BRK.A

Berkshire Hathaway Inc

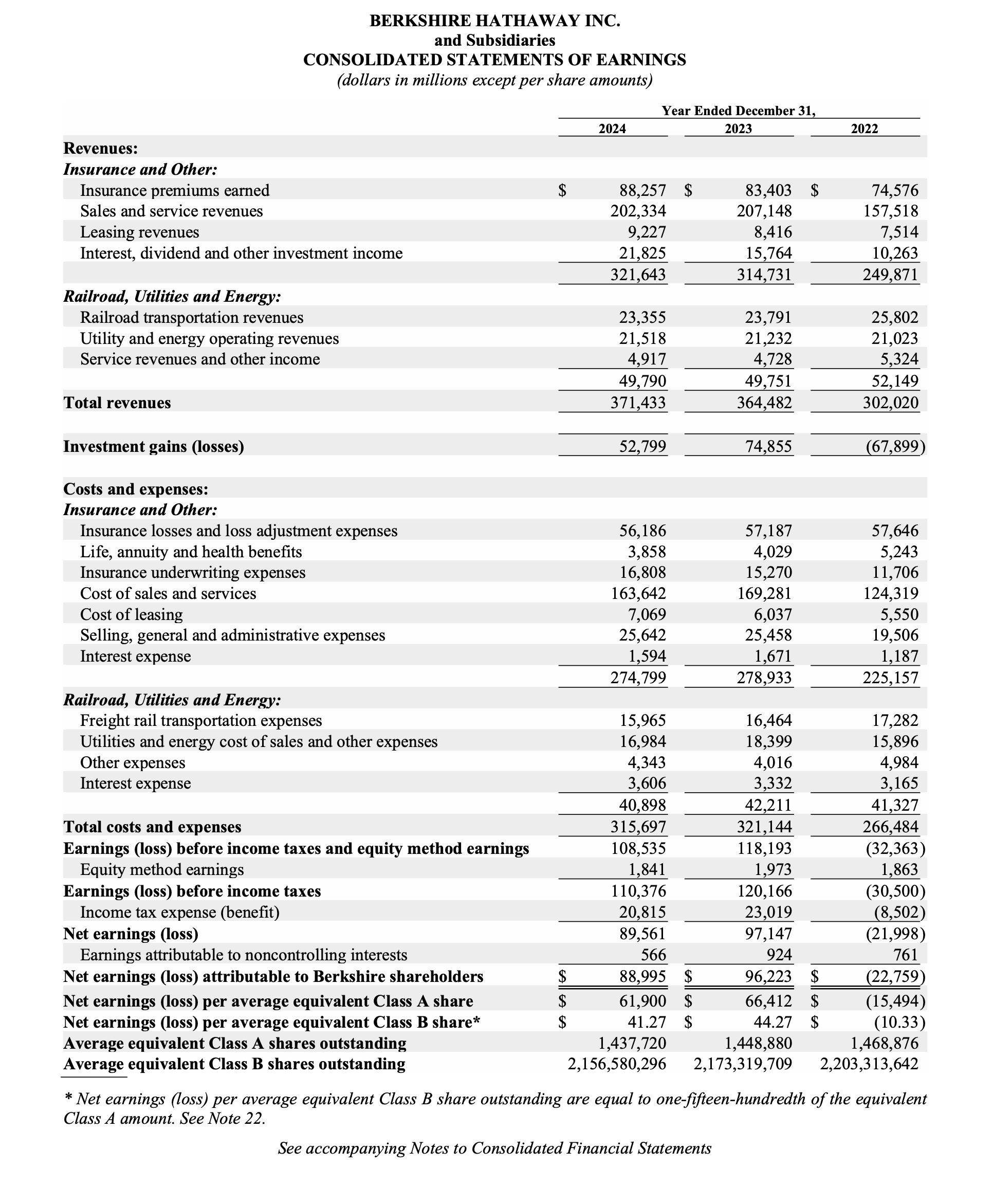

Berkshire's Income Statements is Sterling

Understand The Income Statement(Berkshire's 2025 report will be coming out at the end of this month - this is 2024... still a very useful exercise given how hard Berkshire is to value)

People see Berkshire’s 2024 GAAP net income ($89B) and immediately reach for a P/E.

That’s not how Buffett told us to value Berkshire.

In the 2018 chairman’s letter he basically says: Berkshire is a forest made up of five “groves.” Four are “asset‑laden” groves you can value directly, and the 5th (insurance) finances the others via float. The whole is worth more than the sum because capital can move freely across the groves.

Here’s what this income statement says when you read it that way:

1) The GAAP headline is dominated by the “equities grove.”

Investment gains (losses) were +$52.8B in 2024, +$74.9B in 2023, and –$67.9B in 2022. That’s mark‑to‑market noise...massive swings that tell you more about markets than operating progress... but also HOLY COW! Those are big numbers.

2) The operating forest actually got stronger in 2024.

Back out investment gains and Berkshire earned about $55.7B pre‑tax from the rest of the enterprise in 2024 vs $43.3B in 2023 (**+29%**). Operating improvement… even though GAAP net income went down YoY (because investment gains were smaller).

3) The insurance “float grove” did its job.

Premiums earned were $88.3B and underwriting profit was roughly $11.4B (≈ 87% combined ratio). That’s the engine that can fund the other groves cheaply over time.

4) The cash/T‑bill grove is now a real earnings contributor.

“Interest, dividend and other investment income” was $21.8B (up from $15.8B). In a higher-rate world, Berkshire’s liquidity is no longer just “dry powder” it’s meaningful income.

So the valuation framing (Buffett-style) is:

value the four asset‑laden groves (controlled operating businesses + marketable equities + shared-control holdings + cash/fixed income)

subtract deferred taxes embedded in unrealized equity gains

...and remember the fifth grove (insurance/float) is the structural advantage that helps the first four compound—making Berkshire “the whole > the sum.”

Sentiment: Very Bullish