General

The Hunt for the Next Berkshire

We're all tired of Berkshire valuation posts. I'd love to hear how people value these other conglomerates.

Barron's recently wrote an article covering the 'mini-Berkshire's popping up'

Here's a quick rundown of the top players:

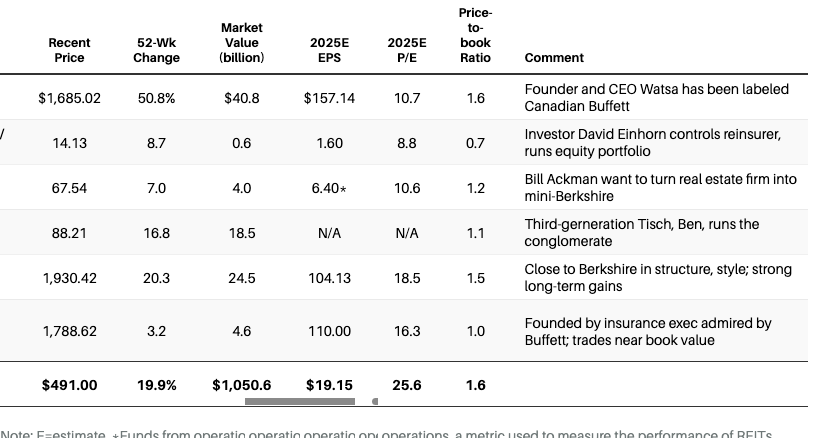

Fairfax Financial

Led by Prem Watsa, often called Canada’s Buffett, Fairfax boasts a 19.2% annual growth since its IPO in 1985.

With extensive insurance holdings and diverse investments (container ships, European banking), Fairfax aims for 15% annual growth in book value (similar to Buffett's stated goal at Berkshire, however due to the 'Law of Big Numbers', Berkshire has only grown TBV by 10% CAGR over the last 10 years).

“You can’t go back and invest in Berkshire in 1992, but Fairfax looks and smells like Berkshire of 30 years ago,” says investor Charlie Frischer, who runs a Seattle family office that holds the stock.

Analysts see Fairfax as reminiscent of Berkshire’s early days, trading at 1.6 times book value—still attractive to investors.

Markel Group

Markel explicitly models itself after Berkshire, even holding an annual brunch post-Berkshire’s famous meeting.

CEO Tom Gayner leads insurance, a ventures unit, and an investment portfolio, which holds a lot of Berkshire itself. Since they went public in 1986, Markel has compounded at 15%, compared against 11.7% for the SP500.

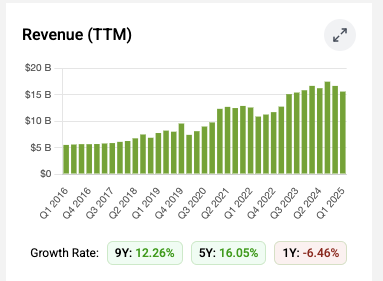

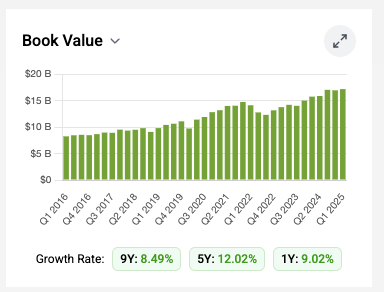

Revenue has grown relatively flatly for a conglomerate. 10/5/1 CAGR are 12%/16%/-6%. But this is a company where I'd focus more on the balance sheet. Book Value's 10/5/1 CAGR are 8%/12%/9%

Despite recent mixed insurance results, Markel remains undervalued compared to its intrinsic value (estimated 35% higher than current stock price). They've also attracted activists investor Jana Partners, they are pushing for improved insurance results and divesting the venture arm of Markel.

Loews

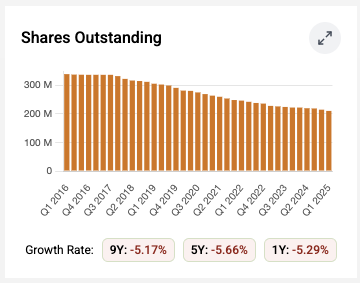

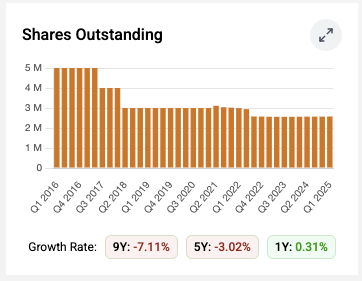

Run by Ben Tisch, Loews emphasizes reducing share count while growing intrinsic value—straight from Buffett's playbook. Tisch explained to shareholders that his only job as CEO is to "Grow intrinsic value per share by growing the numerator, shrinking the denominator"

It has core holdings in CNA Financial (insurance), Boardwalk Pipelines, and Loews Hotels, alongside robust cash reserves. You also get exposure to the new Epic Universal attraction in Orlando-- Loews owns 50% of it.

Despite strong fundamentals, Loews remains overlooked by Wall Street, offering a potential bargain at current valuations.

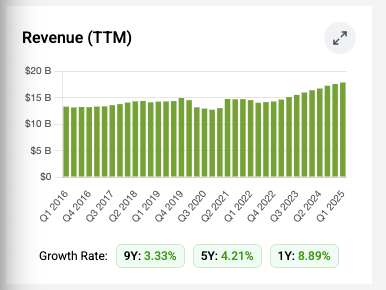

And, yeah, looking at the Shares Outstanding chart is impressive. 10/5/1 CAGR is -5.17%/-5.66%/-5.29%. And Revenue growth is 3.33%/4.21%/8.89%.

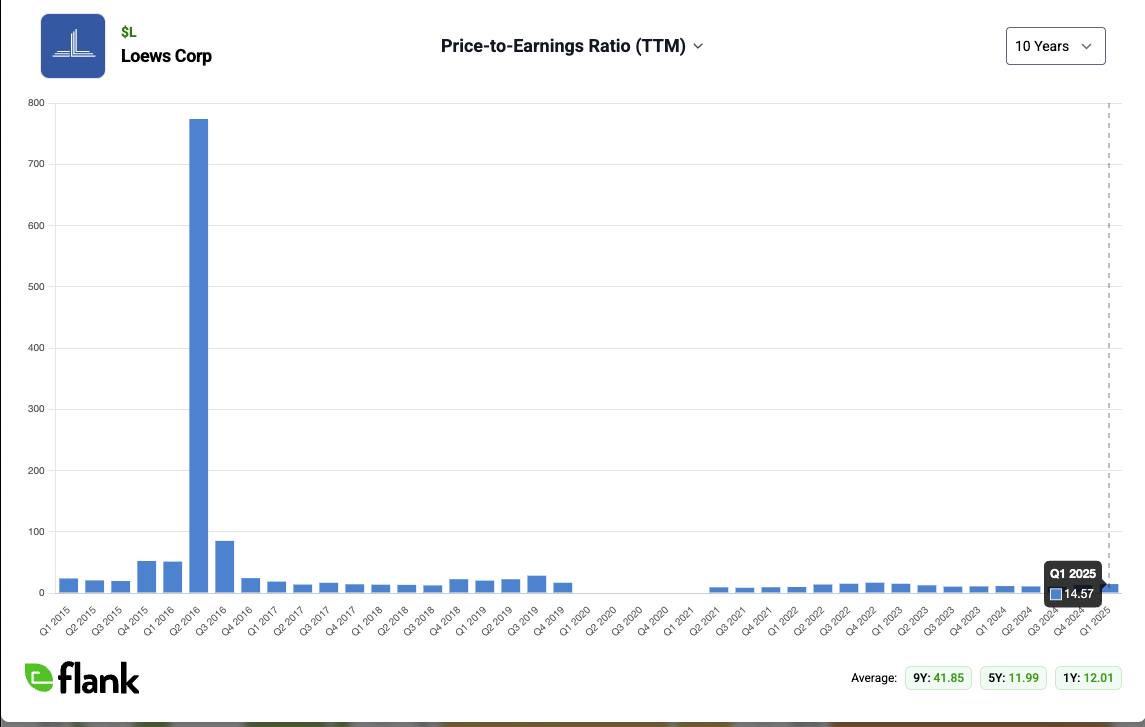

This is probably my favorite on the list. P/E ratio is right around 12

White Mountains Insurance

White Mountains, founded by legendary insurance executive Jack Byrne (who Buffett called the "Babe Ruth of Insurance" and credits him with saving GEICO), steadily grows book value by 10% annually.

With a diversified portfolio including London-based insurer Ark, investment firm Kudu, and insurer Bamboo, it trades just above book value, like literally 1.1 P/BV.

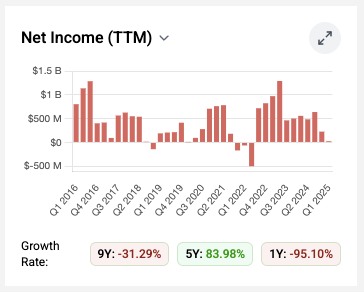

Minimal Wall Street coverage makes it a hidden gem. They do a lot of share buybacks, but Net Income is all over the place. It's 10/5/1 CAGR is -31%/83%/-95%.

Howard Hughes Holdings

Billionaire Bill Ackman recently repositioned Howard Hughes into a Buffett-like structure, merging its real estate assets with potential insurance and growth investments.

Ackman paid a premium to gain control, but shares now trade at a discount. This is a bet on Ackman’s ability to diversify and enhance cash flows, making it a compelling long-term play.

BUT! Unlike the others on the list, Ackman is charging a management fee (and a $15M fee). I think this is the most charlatan of the Berkshire contenders. We made a full video detailing why it's not the next Berkshire (see below)

Greenlight Capital Re

Managed by legendary value investor David Einhorn, Greenlight Capital Re combines reinsurance with Einhorn’s investment strategies.

Greenlight has drastically lagged the SP500 over the past 10 years, mostly due to poor underwriting. But they have a diversified portfolio. The holdings include Gold, life insurer Brighthouse Financial, and coal producer Core Natural Resources.

The stock trades below book value, potentially rewarding investors willing to bet on a turnaround.