DUOL

Duolingo Inc

Was I wrong about Duolingo?

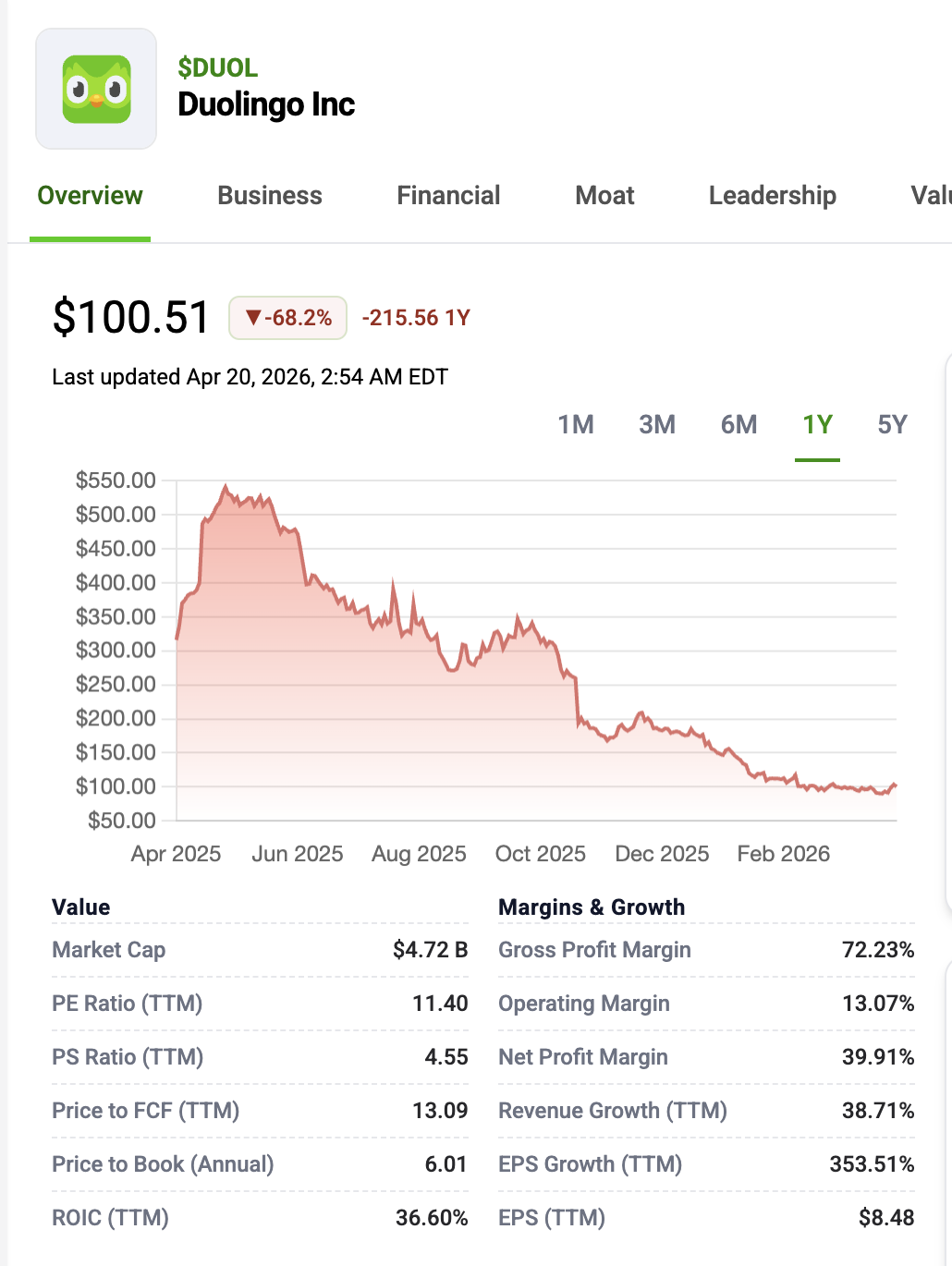

Duolingo has had a rough year. It's current market cap is $4.72B, down from $7.75B when I bought back in November.

Key Changes

CFO change: Matt Skaruppa, CFO since early 2020 who took the public company is stepping down and will be replaced by Gillian Munson, and long-time board member (since 2019) and former CFO of Vimeo.

The stock fell 8.4% in a single day when the CFO change was announced. I don't really care about this; Gillian seems just as capable as Matt.

Chess growing better than expected: Duolingo announced 7M DAU's on Chess in under a year. It's now their fastest growing learning subject, with retention slightly better than language courses.

This is good to see, but it's important to note, math and music have not been growing as quickly as expected.

CEO Luis von Anh confirmed my thesis

They are playing the long game, which I love to see. Management is voluntarily leaving $50M+ of 2026 bookings on the table by removing conversion promts and expanding AI-premium to lower subscription tiers - (AI Live Chat with Lily rolled out to Duolingo Super users). I LOVE to see this.

Luis said they are targeting 20% DAU growth per year. They are exceeding this. On the earnings call, Luis called this out explicitly:

“if we’re seeing faster user growth than we’re expecting, and what we are expecting is about 20%, then that means the strategy is working,”

Financial Performance

Forward P/E ~32x

Trailing P/E: 11.5 (inflated due to a $256M tax benefit recognized in 2025 - reality is closers to 25x)

$400M buyback authorized - signals management thinks its undervalued (!!)

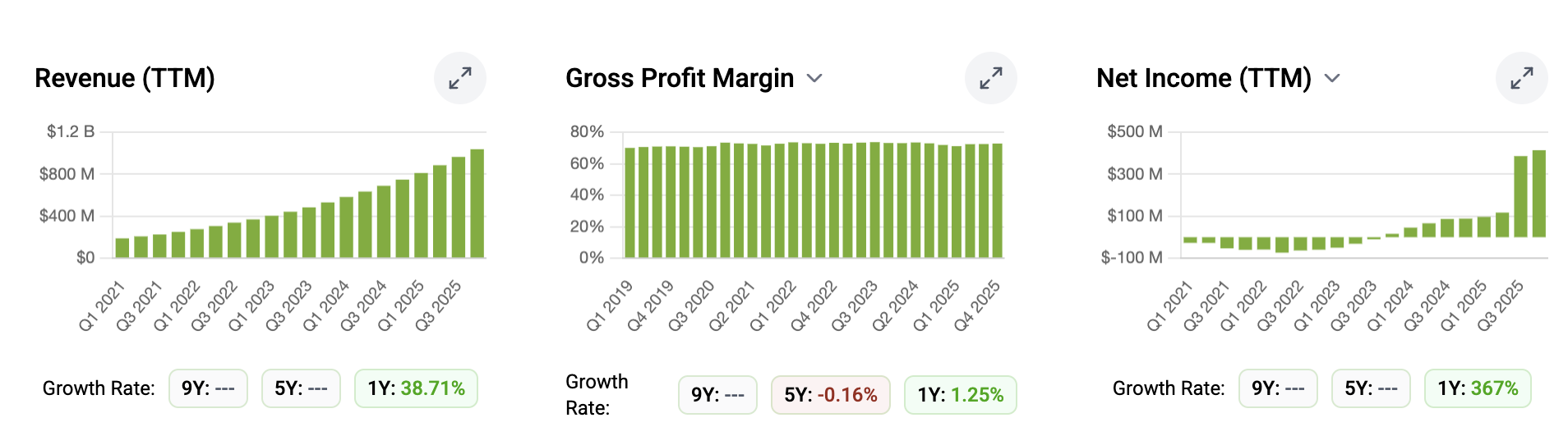

Revenue growth ~38%

Gross profit margin expanded 1.25%

Current Valuation:

I valued Duolingo at $32B last year; after the last two quarters (which is extreme near term in our style of investing), I want to hold my valuation at that level.

I want to think about this more, but I'm strongly considering adding to my position.