BRK.A

Berkshire Hathaway Inc

I valued Berkshire at $970B - ultra-conservatively

Perform Discount Earnings AnalysisThis has taken me a few days to work on, but honestly (and this speaks to the benefit of Flank), writing my thoughts out in the post is really what allowed me to work through it. I stalled a ton trying to just do it via my DCF model.

Writing out your thinking is tremendously underrated in security analysis in my opinion.

Let's value Berkshire using the grove method I've laid out in my prior steps, and just how Buffett told us to do it in 2018

The Groves are:

Non-insurance wholly owned businesses

Public Stock portfolio (Berk owns 5-10% of public stocks)

Shared-control businesses (private businesses not wholly owned by Berkshire)

T-bills

Insurance Float

Grove 1:

I'll start with #1. Here's specifically what Buffett said to do:

So we won't need to account for the taxes, because he said right there that they won't sell their wholly owned businesses.

Grove 1 consists of 51 non-insurance operating businesses (!!). I'll be looking at the biggest ones ("redwoods" as Buffett calls them)

(OP's note: I was stuck trying to determine owner's earnings for BNSF for like....3 days. I fell into my old habit of trying to be penny precise in my valuations... that is not a smart move.)

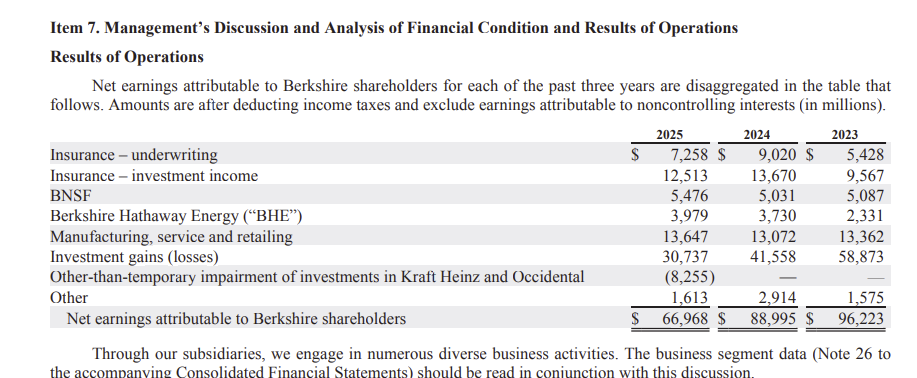

Instead of determining Owner's Earnings, Berkshire gives us a very close approximation (in my opinion) - "Net earnings attributable to Berkshire shareholders"

Alright! That's something we can discount the future earnings.

Grove 1 consists of BNSF, BHE, and Manufacturing, Service and retailing (MSE)... this prevents me from having to count the 'sticks' of Berkshire and instead focus on the redwoods

I assumed a 2% growth rate for BNSF - based on expected GDP growth in the US (conservative, and below their 3-year CAGR of 2.49%)

I assumed a 6% growth rate for BHE. The 3-year CAGR is 19.51%, but those numbers include pre-tax Wildfire loss accruals.

(I had to look up what a pre-tax Wildfire loss accrual was. An accrual means a company records an expense when it becomes likely and estimable, even if the cash hasn’t been paid yet. So Berkshire is saying, “We expect to owe this much money because of wildfires, so we are recognizing the loss now.”)

I assumed a 1% growth rate for MSE... which is certainly conservative, but it has also only grown at a .71% CAGR for the past 3-years (I expect it to perform better in the future)

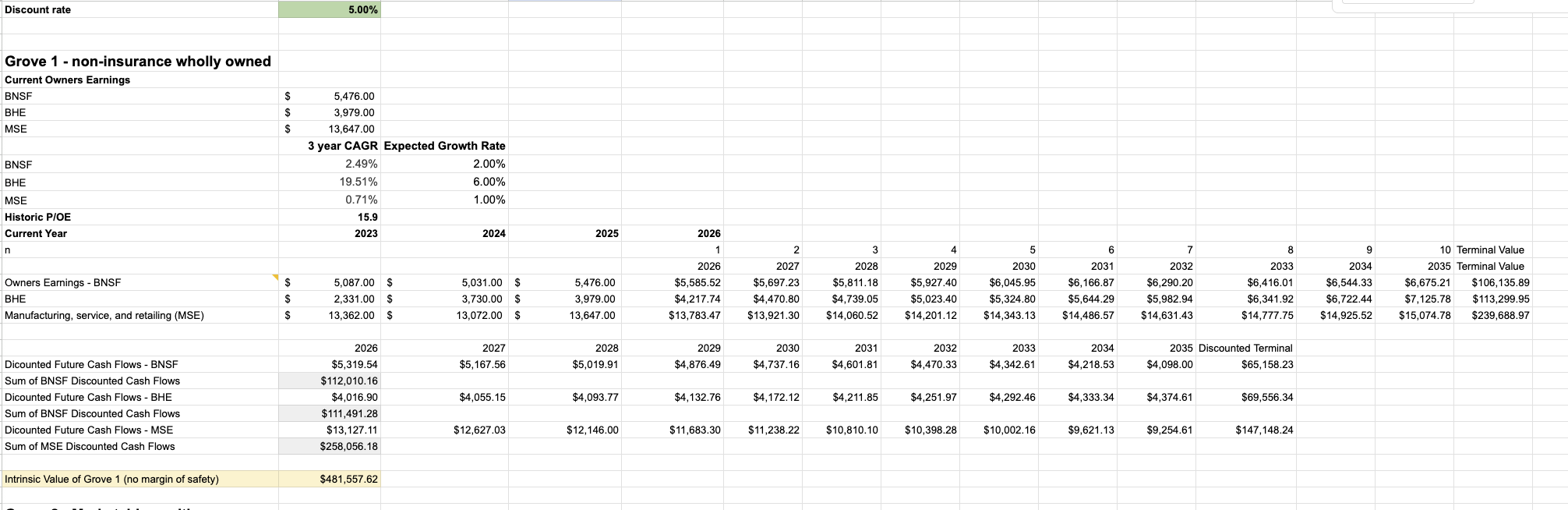

Here's the output of my model:

That puts a pre-margin of safety valuation on Grove 1 at $481B.

I'm liking what I'm seeing so far!

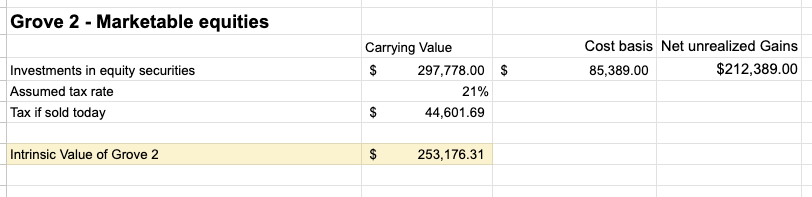

Grove 2:

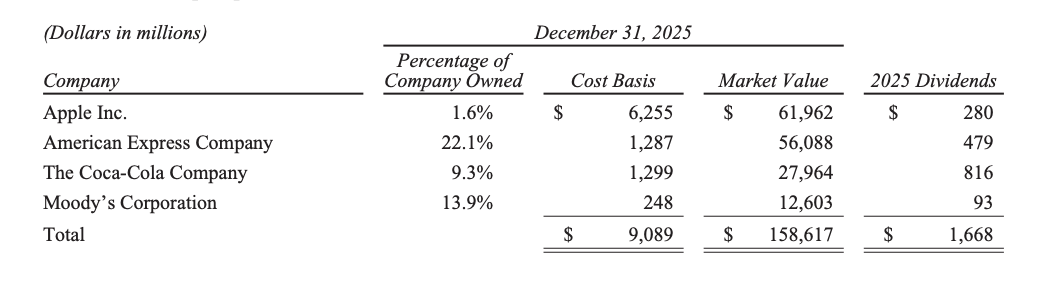

Grove 2 is Berkshire's marketable securities... e.g. their stock portfolio.

Surprisingly, their top 5 holdings account for 65% of their entire portfolio (Buffett is not afraid of concentration)

I didn't account for any growth of these stocks - which is ultra-conservative. Instead, just like Buffett recommends, I took the fair value and subtracted the taxes they would need to pay if they sold

Here's the output of my model:

This values Grove 2 at $253B.

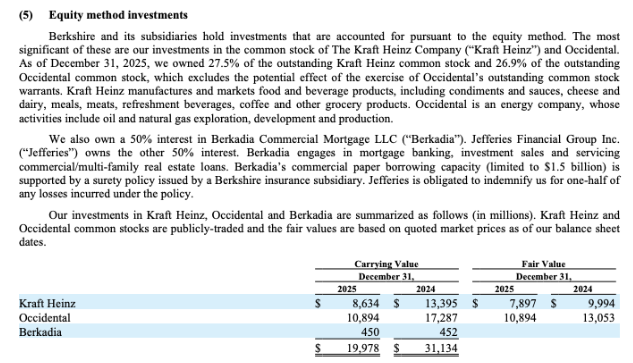

Grove 3:

Grove 3 is Berkshire's equity method investments (which is when they own a considerable amount of a private stock)

This consists of 3 businesses today: Kraft Heinz, Occidental Petroleum, and Berkadia.

I assumed a 0% growth rate on these businesses, because they are not performing well.

This values Grove 3 at $15B, which is a bit conservative, but that's alright with me.

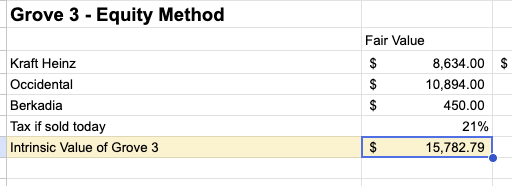

Grove 4:

T-bills! This one is pretty easy. I won't assume any growth, so I'm not even accounting for the coupon that the T-bills will yield.

But even more importantly, this is Berkshire's "blackpowder". This is the capital Berkshire can deploy to buy almost any business it wishes to. When they deploy that capital, it will grow. I'm not accounting for any of that (intentionally - I am being ultraconservative in this valuation)

This values Grove 4 at $390B

Grove 5:

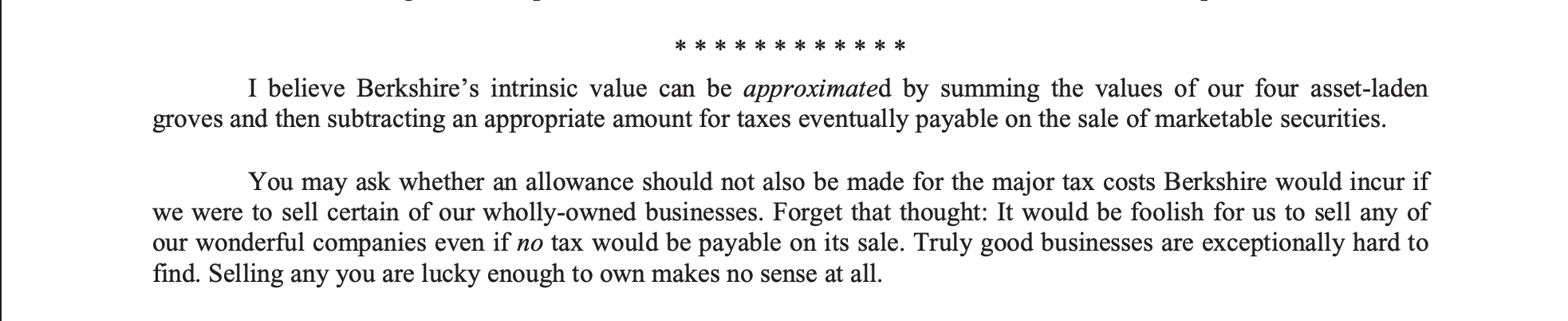

Remember, when Buffett showed us how to value Berkshire, he said, "I believe Berkshire’s intrinsic value can be approximated by summing the values of our four asset-laden groves and then subtracting an appropriate amount for taxes eventually payable on the sale of marketable securities."

Grove 5 is not one of the 4 asset laden groves.

The economic value of Grove 5 is mainly the funding advantage that lets Berkshire own more of Groves 1–4 without normal financing costs. Buffett explains it further in the 2018 letter:

This whole screenshot is worth understanding. It's huge and it's how Berkshire is getting free money.

Here are a couple highlights, just so I'm really being explicit in my explanation of how vital Grove 5 is to Berkshire.

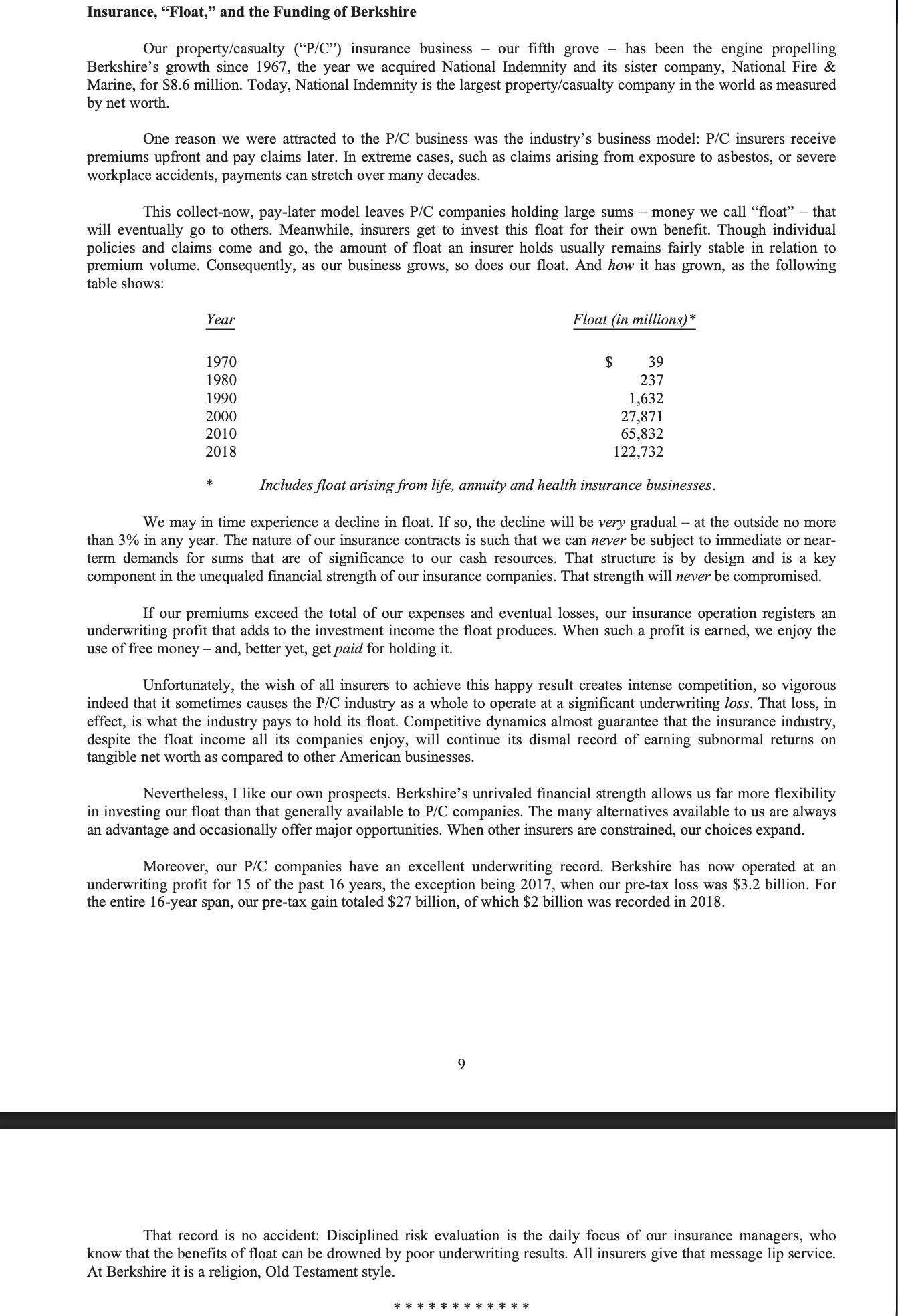

"Our property/casualty (“P/C”) insurance business – our fifth grove – has been the engine propelling Berkshire’s growth since 1967"

"This collect-now, pay-later model leaves P/C companies holding large sums – money we call “float” – that will eventually go to others. Meanwhile, insurers get to invest this float for their own benefit"

"We may in time experience a decline in float. If so, the decline will be very gradual – at the outside no more than 3% in any year."

"Berkshire’s unrivaled financial strength allows us far more flexibility in investing our float than that generally available to P/C companies. The many alternatives available to us are always an advantage and occasionally offer major opportunities. When other insurers are constrained, our choices expand."

"That record is no accident: Disciplined risk evaluation is the daily focus of our insurance managers, who know that the benefits of float can be drowned by poor underwriting results. All insurers give that message lip service. At Berkshire it is a religion, Old Testament style"

The big thing to leave out of Grove 5 is insurance investment income. Berkshire reported $12.5 billion of after-tax insurance investment income in 2025, but it also shows that the insurance businesses held $294.1 billion of equity securities, $212.6 billion of cash/cash equivalents/U.S. Treasury Bills, and $17.466 billion of fixed maturity securities at year-end.

Those assets overlap heavily with what I already counted in Grove 2 and Grove 4, so capitalizing insurance investment income again would double count. That overlap point is my inference from Berkshire’s presentation, but I think it is the right way to keep the grove model clean

OMG I'm finally done. This was by far the hardest valuation I've ever done.

Here it is! I value Berkshire at $1.1T with no MoS. With a 15% margin of safety, I value is at $970B, although I do believe this is too conservative - I was very conservative in my growth rates + this completely ignores Grove 5's power.

I want to sit and "let the dough rise" a bit, but I could see myself making a large investment in Berkshire soon.

Fun fact, 5 days ago, Greg Abel appeared on CNBC and told investors that they would be reinitiating their Buyback program,

which has been suspended since 2024. Berkshire famously only buys back its own stock when the CEO thinks shares are undervalued - so I'm very happy to see that my analysis is lining up with managements.

Sentiment: bullish