ADUR

Aduro Clean Technologies Inc

Aduro Needs to Make Money to be a real company. What's their plan?

What's Their Growth Strategy?Aduro has a really cool method of converting waste plastics, heavy crude/bitumen and renewable oils into more valuable resources.

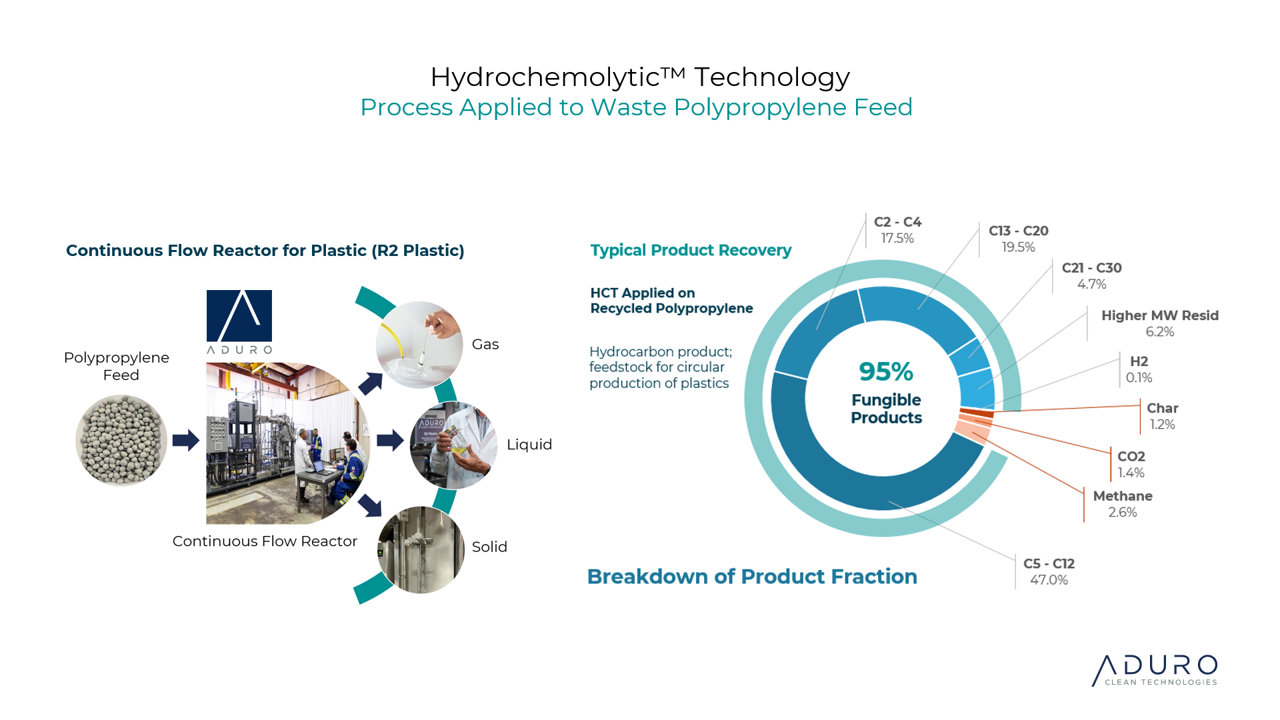

Their innovative method (called HCT- which stands for Hydrochemolytic Technology) is subcritical water-based unlike the traditional high-temperature pyrolysis currently being used in upcycling.

They've identified that their technology's total addressable market is over $250B. https://investors.adurocleantech.com/overview/default.aspx#:~:text=

But! The company has almost no revenue. They are still finding a commercial application to their technology. So the key to the company will lie in their ability to do just that.

Let's look at what they're working on:

## Ongoing Pilot Programs

Pilot Plant: Aduro has built a Next Generation Process (NGP) pilot plant in Ontario, in a partnership with modular plant engineering firm Zeton. The pilot plant is designed for a throughput on the order of 5-10 tons per day of plastic.

Commissioning began in September 2025 (on schedule), according to their most recent quarterly report. Initial feed and reactor tests are underway, and we should have initial pilot data on yields, operating parameters, and equipment performance. This will hopefully de-risk scale up to the next stage.

Notably, Aduro even filed a new patent for a process design improvement to be integrated into the pilot, underscoring ongoing R&D progress

Customer Engagement Program (CEP): Additionally, Aduro is running a paid program to involve potential commercial customers early. Under CEP, interested companies pay Aduro to test their feedstocks in Aduro's reactors. Six major companies (all multi-billion dollar firms) are currently in the evaluation phase.

One of the six companies is Shell, which selected Aduro for their presitgious GameChanger accelerator program. Through this program, Shell provided non-dilutive funding and technical mentorship for a 12-month, 6-phase project to rigorously test Aduro’s HCT on polyethylene, polypropylene and polystyrene, from bench scale up to a continuous flow reactor and commercial design basis

The true purpose is to seed future deals: if testing yields positive results, clients may enter the next phases – joint development of pilot/demo projects (collaboration) and eventually deployment deals (commercialization).

I really like this program. It'll hopefully scale up design.

Demonstration Plant: As the pilot plant data proves out the technology, Aduro is already planning a demonstration-scale plant to bridge the gap to full commercialization. In March 2025, Aduro signed an MOU with NexGen Polymers (a veteran polymer feedstock supplier) to collaborate on deploying an HCT demonstration unit.

The global site-selection process kicked off in late 2025, focusing on locations in Canada, Europe and Mexico that offer feedstock supply, supportive regulations (e.g. mass balance certifications for product circularity), offtake markets and expansion room

The Demo facility is expected to have a 22 tons/day throughput!

Licensing Business Model: A core tenet of Aduro’s strategy is to scale via partnerships and licensing rather than building many plants on its own (VERY smart).

Management describes a “capex-light” model where Aduro would license out its HCT technology and know-how to industry operators (such as petrochemical companies, waste management firms, or project joint ventures) who would finance, construct, and operate the recycling units.

In return, Aduro would earn licensing fees or royalties – roughly on the order of 20–30% of the revenues those plants generate. This model allows rapid expansion with relatively low capital expenditure by Aduro and inherently high gross margins on the royalty streams. (For instance, if a full-scale plant produces $100 of product revenue, Aduro might earn ~$20–30 via royalty/license, at very high margin since the operating costs are borne by the plant operator.)

The company indicates it may still build and own a few plants in strategic cases (to jump-start adoption or serve as flagship facilities), but even those are expected to have healthy economics (projected 40–50% gross margins on operations).

Overall, the long-term vision is to become an IP provider and technology licensor to global plastics and energy companies, rather than a heavy-asset project developer. This approach is intended to enable fast global scaling once HCT is validated, as multiple projects can be pursued in parallel by partners. However, it also means Aduro’s success hinges on proving the technology and then convincing larger players to adopt it. Fact-check note: As of now, no commercial licenses have been signed – all industry interactions are in testing or MOU stages. The licensing model’s viability will depend on Aduro delivering tangible results in pilot/demo and negotiating favorable deals thereafter.

Okay, so that was a lot. My biggest question is: WHEN can we expect scale up? I can't wait 5 years to see if their technology works

## My yearly expectations

1-Year: By 2026, Aduro is unlikely to have significant revenue yet. The next 12 months will focus on pilot plant operations and building the demonstration plant. The NGP pilot unit (5–10 tpd) should be fully commissioned and running continuous trials in early-to-mid 2026, providing performance data and sample outputs to interested partners. This might generate small revenue if Aduro sells any product from the pilot (e.g. oils produced) or does additional paid test projects. However, pilot-scale output is limited and primarily for testing, not profit.

Base expectation is that revenue will still be <$1M by the end of 2026

2-Year: By 2027, we should start seeing initial commercial traction if Aduro’s plan is on track. Several critical things need to happen in this timeframe for revenue to ramp up:

(a) The 8,000 tpy demonstration plant must be built, commissioned, and operational (ideally by mid/late 2027), and

(b) at least one or two partners move from testing to implementation agreements

The demo plant, once running, could itself generate a modest revenue stream: 8,000 tonnes/year of recycled output – if, say, the product oil sells for $600–$1,000 per tonne (a rough market range), then the demo plants revenue could be $5-8M/year

5-Year: Looking out to 2030, Aduro could be at the inflection point... either scaling up commercial deployments, or struggling with a technology that hasn't been widely adopted.

In the successful scenario, five years would be enough time to go from demo to multiple commercial plants

## Conclusion

From point A (today) to point B (a 100× larger company), Aduro’s journey will be defined by its ability to turn promising tests into profitable projects. Today, the company’s test cases and pilot projects show promise – e.g. converting waste plastics (even tricky ones like dirty turf or mixed polymers) into valuable outputs, attracting interest from industry giants like Shell . The fact-check on these claims is that they are genuine early successes, but on a small scale; no fundamental red flags have emerged so far, yet no commercial validation has happened yet either. The next few years will be critical. If Aduro’s technology truly delivers the advantages it advertises in real-world conditions, the company’s growth could accelerate rapidly through partnerships and licensing.

Sentiment: Neutral