NVDA

NVIDIA Corp

How Do They Make Money?

How Do They Make Money?NVIDIA: How the AI Infrastructure Titan Makes Money

NVIDIA has evolved far beyond being just a chip manufacturer. They sell the entire package:

the brains (GPUs, CPUs, full AI systems),

the nervous system (networking fabric),

the software glue (CUDA, AI tools).

This creates a closed ecosystem with enormous lock-in, almost like a toll booth for the whole AI industry.

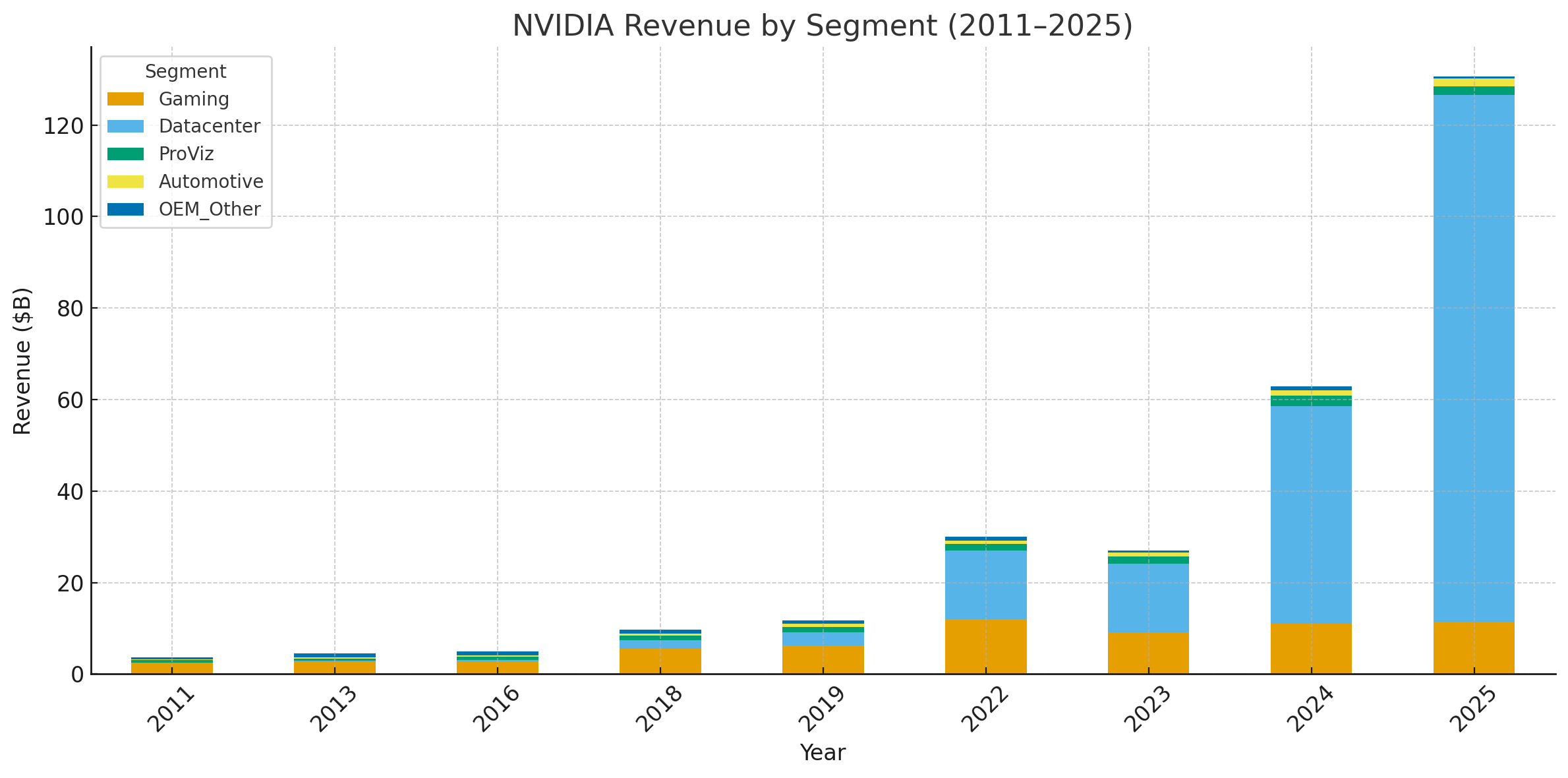

Pillar 1: The AI Compute Engine (Data Center)

Products: High-margin GPUs (H100, B100/GB200), CPUs (Grace), complete supercomputers (DGX SuperPODs costing $10M+ each).

Networking: InfiniBand, Ethernet, NVLink (via Mellanox). Enables thousands of GPUs to act as a single “AI brain.”

Customers: Hyperscalers (AWS, Azure, Google Cloud), AI labs (OpenAI), tech giants (Meta).

Financials (FY2025): $115.2B revenue (+142% YoY), 88% of total business, 73% operating margin.

Growth: From $340M (2015) to >$115B (2025).

(some visuals from an earlier post)

Pillar 2: The Software Moat (CUDA & Ecosystem)

CUDA: Proprietary programming model and platform for NVIDIA GPUs.

Lock-in: 4.7M developers, 15+ years of ecosystem building. Virtually all major AI frameworks (TensorFlow, PyTorch) run on CUDA.

Economic effect: Competitors might build faster chips but cannot replicate the ecosystem. Switching costs are prohibitive.

Monetization: Indirect (driving GPU demand) + direct (subscriptions like NVIDIA AI Enterprise with ~100% margins).

Pillar 3: Gaming & Professional Visualization (Cash Cow)

Gaming: GeForce RTX GPUs, DLSS technology.

Professional Visualization: High-end workstation GPUs (Quadro/RTX), Omniverse software for digital twins.

Financials (FY2025): $13.3B (~10.4% of sales).

History: In 2018, Gaming was the core (57% of sales). Today, Data Center is the dominant engine.

Pillar 4: Automotive (Long-Term Bet)

Products: DRIVE platform (Orin & Thor SoCs, software stack).

Strategic stickiness: Auto design cycles last 5–7 years. Winning a contract locks in long-term, high-margin revenue.

Financials (FY2025): $1.7B (~1.3% of sales, +55% YoY).

Pillar 5: Optionality (OEM, Jetson & Robotics)

Products: Jetson AI modules for robotics/drones, custom chips (e.g., Tegra for Nintendo Switch).

Financials (FY2025): $0.4B (~0.3%).

Strategic purpose: Plant seeds for future billion-dollar markets—just like Tegra laid the foundation for Automotive.

Big picture:

NVIDIA is no longer “just” a hardware vendor. It has become the core infrastructure of the global AI economy, with CUDA as its moat and Data Center as its rocket engine. Gaming/ProViz remains the stable cash generator, Automotive is the long bet, and Jetson/OEM is an option factory for tomorrow’s breakthroughs.