BRK.A

Berkshire Hathaway Inc

The many ways Berkshire makes money...

How Do They Make Money?Alright, I'm going to do it.

The market is so risk-on right now, I want to look at the more defensive stocks (be fearful when other's are greedy).

With that, for this month's Flank Challenge, I'm going to complete 100% research on Berkshire Hathaway... and determine what I believe the fair value for it is.

Berkshire, since it is a holding company, has many businesses. Holding Companies are notoriously difficult to value.

Obviously, I've studied this company extensively, and already hold the stock (I've held it for over a decade). But I haven't run it through the Flank methodology. Now's as good as time as ever.

How does Berkshire make Money?

Berkshire Hathaway is a holding company engage is numerous diverse business activities.

The most important of these are insurance, freight rail transportation, and energy generation and distribution activities.

Berkshire has over 392,400 employees around the world. 20% of them are unionized.

Insurance

At its core, Berkshire insures risk across the globe through dozens of subsidiaries, covering everything from auto insurance to complex reinsurance contracts. These businesses span primary insurance (insuring individuals and businesses directly) and reinsurance (insuring other insurance companies). At the end of 2024,

Berkshire’s insurance group employed roughly 41,500 people worldwide.

While insurance is a highly competitive industry with few barriers to entry, Berkshire differentiates itself in three critical ways: financial strength, disciplined underwriting, and long-term thinking.

Berkshire organizes its insurance operations into three main groups:

GEICO, which focuses primarily on auto insurance and competes on cost efficiency and customer service through its direct-to-consumer model.

Berkshire Hathaway Primary Group, a collection of specialized insurers covering commercial, medical, professional, workers’ compensation, and specialty risks.

Berkshire Hathaway Reinsurance Group, which provides large-scale reinsurance for property, casualty, life, and health risks worldwide.

Unlike many insurers that chase growth, Berkshire is willing to walk away from underpriced risk. Management expects to generate underwriting profits over time, meaning the insurance business itself is profitable before considering investments.

But the real magic comes from float.

Insurance premiums are collected upfront, while claims are paid years or even decades later. This creates a massive pool of low-cost capital known as float. By the end of 2024, Berkshire’s float had grown to approximately $171 billion. That money is invested primarily in equities and other long-term assets, historically generating returns far above what most insurers can achieve.

Energy

Berkshire Hathaway Energy (BHE) owns a diversified portfolio of regulated electric utilities, natural gas pipelines, transmission assets, and renewable power projects across the U.S., the U.K., and Canada.

The core of BHE’s business is straightforward: invest capital into essential energy infrastructure and earn regulated returns over long periods of time. Most of its utilities operate as monopolies within defined service territories, giving them exclusive rights to serve customers in exchange for heavy regulation. Rates are typically set on a cost-of-service basis, allowing BHE to recover expenses and earn a reasonable return on invested capital.

From an investor’s perspective, BHE is not a growth rocket. It is a capital-heavy, regulation-bound compounder that converts steady reinvestment into dependable long-term value. This is exactly the kind of business Berkshire favors: essential, boring, and built to last.

Non-Energy Businesses

Beyond insurance, rail, and energy, Berkshire owns a massive collection of “real economy” businesses that quietly generate a lot of cash.

HomeServices of America is a huge U.S. residential real estate brokerage network. It makes money on transaction volume and also captures more of the homebuying chain through mortgage, title, closing, insurance, and relocation services. It is cyclical and competitive, and revenues tend to be strongest when housing activity is high.

The rest is a broad set of operating companies across manufacturing, services, and retail. Manufacturing alone employs roughly 180,000 people, spanning everything from aerospace components (Precision Castparts) and specialty chemicals (Lubrizol) to building products (Clayton Homes, Shaw, Johns Manville, Benjamin Moore, Acme Brick) and consumer brands (Forest River, Fruit of the Loom, Duracell).

On the service and retail side, Berkshire owns businesses like McLane (a high-volume distributor), Pilot Travel Centers, NetJets, FlightSafety, and a range of retail operators. Many of these are capital-light, operationally disciplined, and built around scale, logistics, and brand.

The takeaway: Berkshire is not one business. It’s a portfolio of durable cash generators that benefits from smart capital allocation at the top.

Burlington Northern Santa Fe (BNSF)

BNSF is one of the largest railroad networks in North America and represents Berkshire’s most important non-insurance operating business.

Railroads benefit from high barriers to entry. Once tracks are laid, competitors cannot easily replicate the network. This gives BNSF durable pricing power, especially on long-haul and bulk freight where rail is far more fuel-efficient than trucking. Revenue is generated through a mix of long-term contracts and published freight rates, tying performance closely to overall economic activity..

As you can see, Berkshire does a lot. Holy Cow.

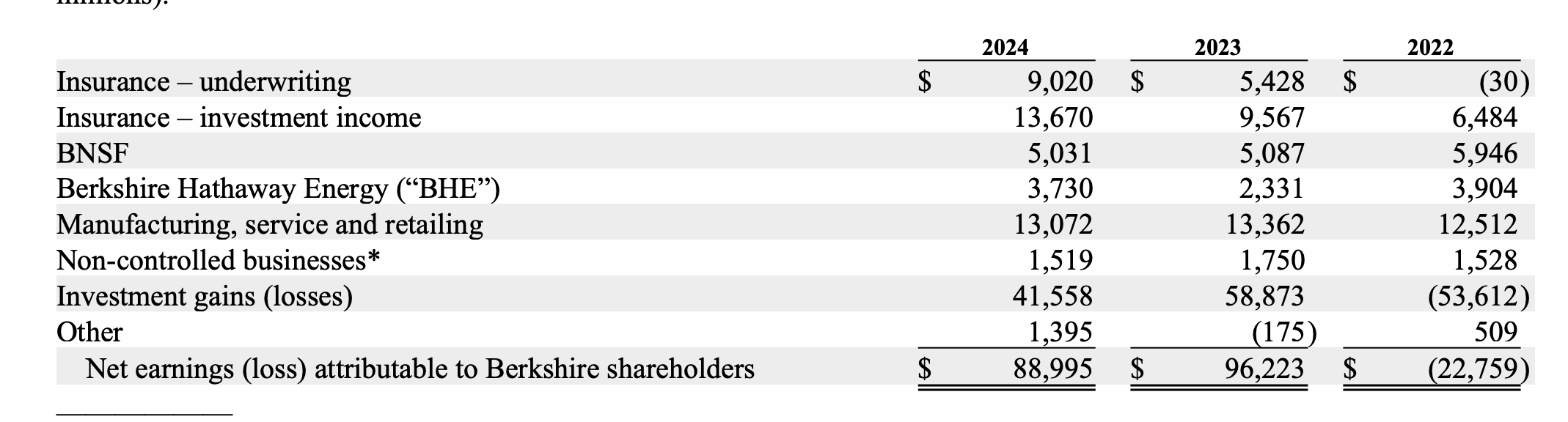

Which ones are the biggest? Which ones are the most profitable? Here's the answer right from the Annual Report.

Sentiment: Very Bullish