FUN

Six Flags Entertainment Corp

What do all these Activists see in Six Flags?

With Six Flags stock down 45% in 2025, it makes sense that activists have smelled blood in the water.

But I want to know: what is their thesis?

Let's take a look!

Jana Partners (9% stake)

I've talked about this in a recent post, but in October 2025, activist hedge fund JANA disclosed a ~9% position in Six Flags, teaming up with NFL star Travis Kelce and two industry veterans (former Gap CEO Glenn Murphy and tech executive Dave Habiger) as an investor.

JANA’s Scott Ostfeld outlined their thesis at a 13D Monitor conference: Six Flags has significant untapped potential in its brand and assets, but needs to improve marketing, modernize the customer experience, and upgrade technology to boost attendance.

The JANA/Kelce group is prepared to push for leadership changes (the CEO Richard Zimmerman is already set to step down by year-end) and even consider strategic options – JANA’s agenda explicitly includes “exploring a potential sale” of the company if that would unlock value.

Six Flags responded diplomatically that it “appreciates the perspectives of shareholders” while it works to increase attendance and profitability.

As of now, JANA has not launched a proxy fight, but potential board nominations are looming – Kelce, Murphy, and Habiger have been mentioned as possible director candidates if needed.

JANA’s involvement comes amid an ongoing board shake-up: the Executive Chairman (Selim Bassoul) and lead independent director will exit the board at year-end 2025, opening slots for new voice.

Sachem Head Capital (≈10% stake)

Another activist investor, Sachem Head, quietly built a nearly 10% position in Six Flags during 2025 and reached a cooperation agreement with the company.

In October 2025, Six Flags agreed to appoint Jonathan Brudnick, a partner at Sachem Head, to the board, expanding the board to 13 members (then dropping to 11 after retirements)

Jonathan Brudnick said in a press release, "We invested in Six Flags because we strongly believe in the potential of the business and that numerous pathways exist to addressing the Company’s current undervaluation. I look forward to working with my fellow directors to continue the important work underway to ensure Six Flags builds on its legacy as the premier amusement park company in North America."

Land & Buildings (2% stake)

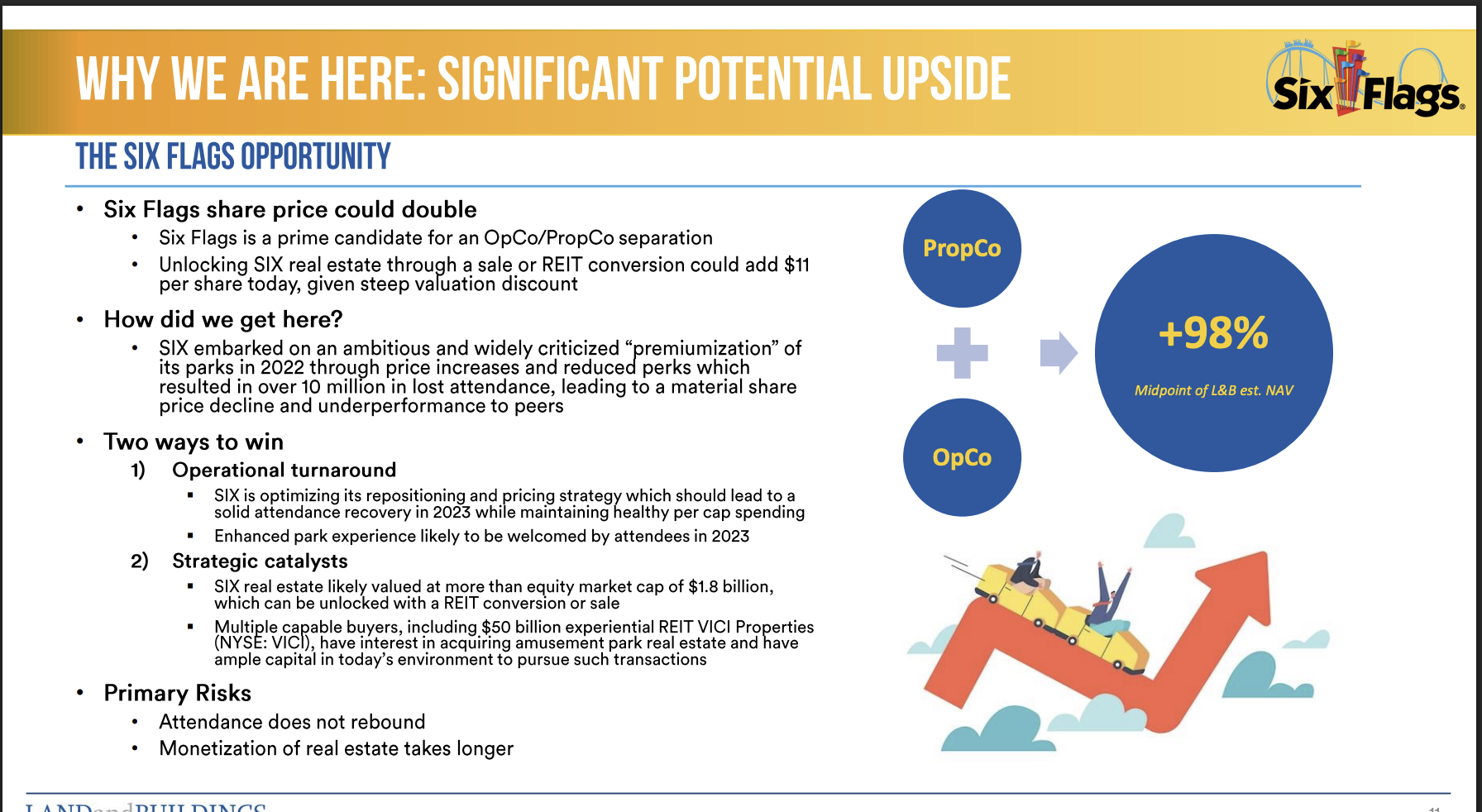

Real-estate focused activist Land & Buildings Investment Management (run by Jonathan Litt) has been agitating since late 2022 for Six Flags to monetize its substantial real estate holdings. L&B argues that Six Flags’ 10,000+ acres of park real estate is undervalued by the market and could be worth up to $6 billion if separated.

Here is their original thesis from 2022

In that thesis, Land & Buildings urged the company to execute an OpCo/PropCo split – essentially spin off the land into a REIT or do sale-leaseback deals – to unlock value for shareholders.

So, they propose:

1. Spin off or sell the PropCo

Move the land and physical parks into a new, separate entity (the PropCo).

That PropCo could be structured as a REIT (Real Estate Investment Trust), which would own the land and lease it back to the operating entity.

The PropCo would collect rent from the OpCo.

2. Keep the theme-park operations in the OpCo

The OpCo would continue running the Six Flags brand, staff, rides, and ticketing.

It would become an “asset-light” operator — like Marriott or Hilton in hospitality — focusing on brand, operations, and customer experience, not owning the underlying real estate.

According to L&B’s analysis, Six Flags’ stock was trading at an extremely low ~7× EBITDA multiple on depressed earnings, while park real estate could command much higher valuations (cap rates ~7–8%) if held by a REIT