OPEN

Opendoor Technologies Inc

Opendoor is skyrocketing... why?

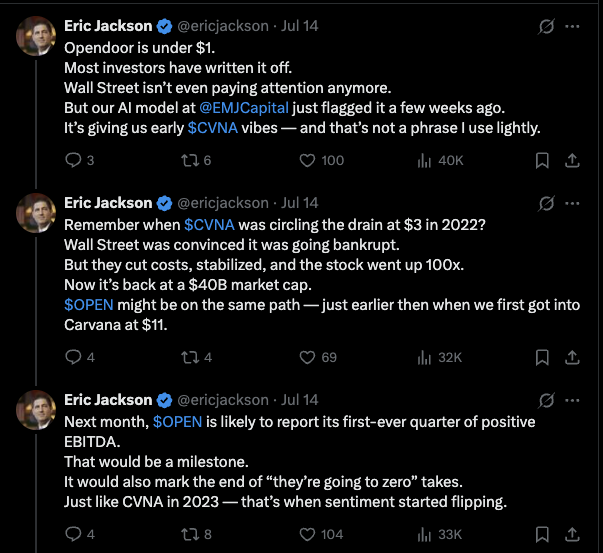

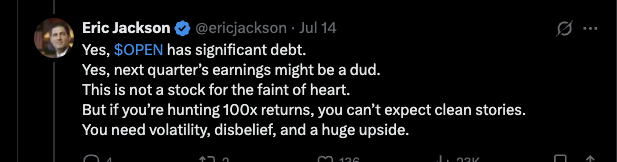

It all started with an X post...

From EMJCapital's founder Eric Jackson. You can find his original post here where he lays out his thesis

I'm going to shoot some holes in it.

First, he believes that Opendoor is feels similar to Carvana's stock in 2023... alright?

His reason for this... they'll likely be EBITDA positive next quarter.

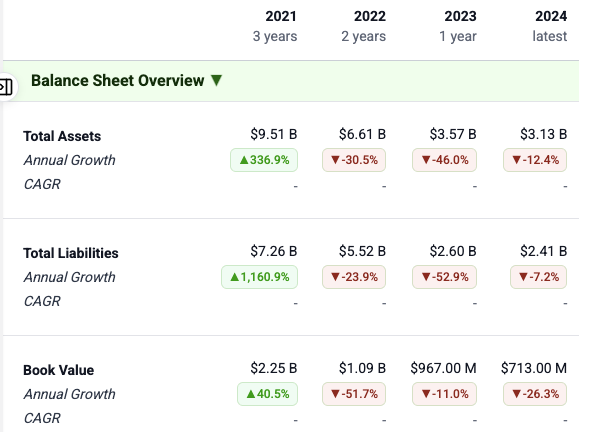

EBITDA means literally nothing for this business. Their business model is to almost immediately buy houses and eventually resell them for profit.

That means they have a very heavy balance sheet. Depreciation is a very real expense here.

So, the fact they will be EBITDA positive in the next quarter means less than nothing to me. Let's talk when they have positive net income.

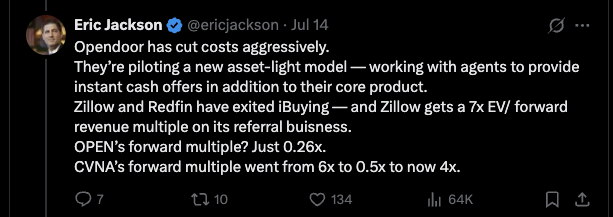

Cost Cutting

Eric claims that $open is cutting costs agressively and forming a new asset light business model-- working with agents to provide instant cash offers.. that's a good move. Credit given here.

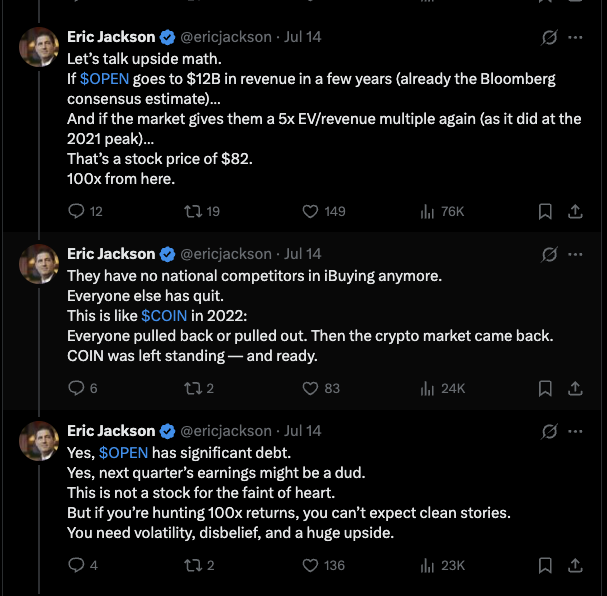

And then finally he talks valuation...

He believes that $open can reach $12B in revenue, and then with historic valuations, it'd have a share price of $82. This is lofty, and not exactly how I like to value businesses, but it works.

His saving grace to me is that he mentions how risky this buy is. I respect that, but then if you look on his X profile, he is constantly pumping the stock. It's ok to pump, but as we often see in these cases, the dump is where you should be in trouble.

I'm not going anywhere near this stock in the meantime though. I don't think their business model works, and it hasn't been able to prove itself out over it's 10+ years in operation.

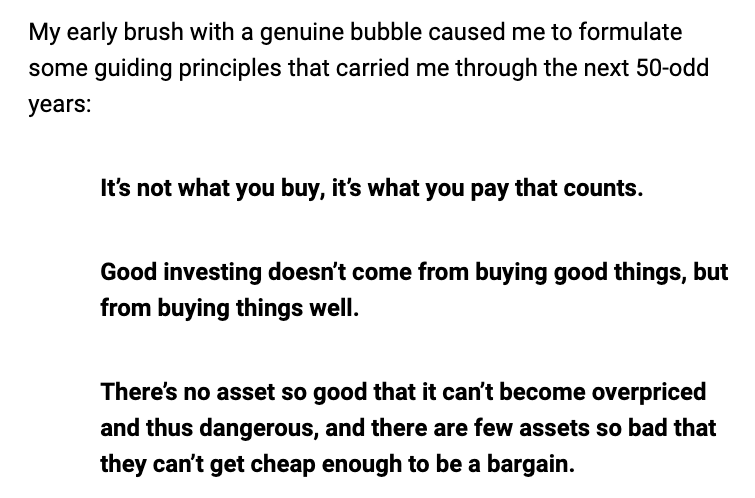

But, remembering the eternal words of Howard Marks:

When the stock was trading for less than $1, Eric certainly saw $open as the latter half of the last point. Now, if you're buying out of FOMO, there's a high chance you'll learn the former half of the last point.