BRK.A

Berkshire Hathaway Inc

Berkshire's Competitive Analysis

Do They Have A Competitive Advantage?This was a hard one to write, I've thought about it for a few days now. The grove analysis doesn't really make sense here (competing against T-bills?)

So... who, really, does Berkshire compete against? They're certainly not a monopoly, but head-to-head, there is no other company on Earth like Berkshire.

So, I thought it would be best to compare two different arenas that Berkshire competes in:

Operating arenas (insurance, rail, energy, industrial/consumer businesses)

Capital-and-deal arena (the holding company). Berkshire competes as a buyer/owner of businesses and a provider of permanent capital. This is competition against Private Equity, strategic buys, and other large pools of capital.

This second arena is where Berskhire's most distinctive competitive advantage shows up. No one is better financed than Berkshire. And... for decades past, who wouldn't want to get "Warren Buffett is an investor in my company". Not sure Greg Abel will have the same premium.

Let's get into the Operating Businesses:

Insurance

For personal auto (think GEICO).. Berkshire is the number 3 player.

Here's a breakdown according to NAIC:

State Farm (18.87% share)

Progressive (16.72%)

Berkshire Hathaway group (11.63%)

Allstate (10.19%)

USAA (6.16%)

Top 5 = ~63.6% combined share.

The current competitive story has been that Progressive has been executing better in pricing/segmentation and data/telematics, while GEICO has been rebuilding profitability and systems—often at the expense of growth. Here's a good Barron's article that talks about the tech problems GEICO is facing.

Bottom line for personal auto: Berkshire is a top‑3 scale player in a concentrated market, but advantage is contested and not automatic. I believe their underwriting discipline will shine through.

Commercial Insurance

In commercial lines, major competitors include Travelers, Chubb, Liberty Mutual, AIG, plus specialty carriers like W.R. Berkley, CNA, Hartford, Markel, etc.

Berkshire's the number 4 largest insurance company for Commercial (#1 is Travelers, #2 Chubb, #3 Liberty)

In many commercial/specialty lines, the “competition” is less about advertising and more about:

distribution relationships,

underwriting talent,

speed/authority to quote,

and (crucially) willingness/ability to write large or unusual risks... which Berkshire's more than capable of doing.

Berkshire's edge? The sheer scale of their capital base. Buyers care about claims-paying ability and capacity. Berkshire boasts a statutory surplus of ~$310B.

Reinsurance

Reinsurance is insurance for insurance companies (confusing I know).

The global reinsurance competitor set is the familiar top cohort: Swiss Re, Munich Re, Hannover Re, Lloyd’s, SCOR, etc.

S&P Global Ratings’ ranking of the world’s largest reinsurers (reported by Insurance Journal) places Berkshire Hathaway Insurance Group #4 globally, behind Swiss Re, Munich Re and Hannover Re (with Lloyd’s #5)

Reinsurance is a business where “competitive advantage” is heavily influenced by:

capital strength (to take peak exposures),

reputation/relationship reliability,

and the ability to be a steady market across cycles.

Berkshire is, in my opinion, top dawg here. No question.

Let's talk Railroads and energy now.

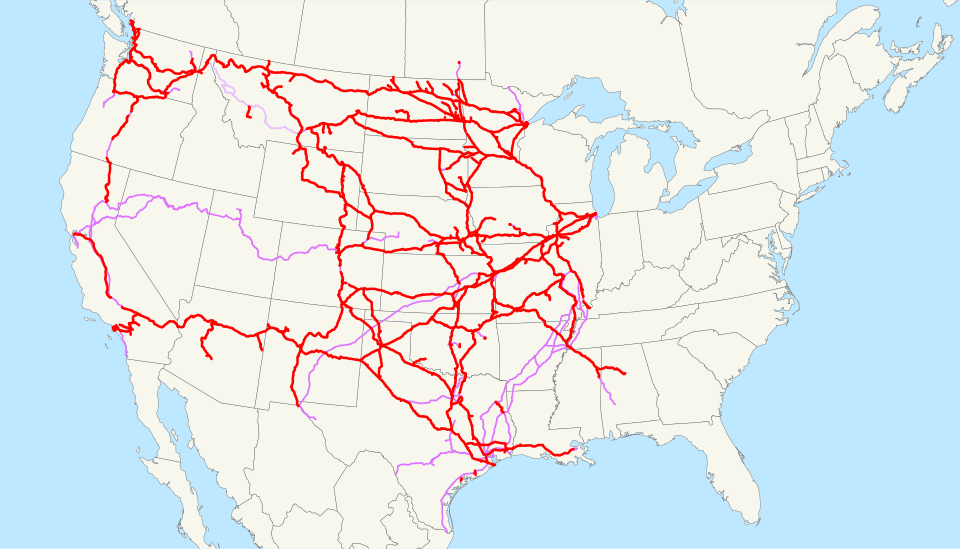

BNSF

BNSF is one of 6 Class I railroads in the US.

The competitor set in North America is small: BNSF, Union Pacific, CSX, Norfolk Southern, Canadian National, Canadian Pacific Kansas City, Kansas City Southern (now combined into CPKC).

Their railway network is impressive. To me, this seems like an impenetrable moat (but we're not on that step yet)

The relevant question is less “does rail have competition?” and more “does BNSF execute as well as Union Pacific and the other Class I’s?” Berkshire ownership helps with patience and capital consistency, but it doesn’t guarantee operating superiority.

Berkshire Hathaway Energy

BHE is a utility/energy holding company with major subsidiaries including PacifiCorp, MidAmerican Energy, NV Energy, Northern Powergrid, and other energy businesses.

In regulated utility service territories, direct head‑to‑head competition for customers is limited (you typically don’t “switch” wires providers). The competitive pressure is more:

regulatory outcomes (allowed returns),

reliability performance,

cost control,

and capital allocation decisions versus other utilities and infrastructure owners.

Does Berkshire have an edge? Parent backing can matter here: utilities are capital-intensive, and being owned by Berkshire can support large investment programs through cycles (again: not a guarantee of better returns, but a real difference vs smaller standalone utilities that must constantly manage equity/debt issuance timing).

So yeah, they have an edge in my opinion.

Let's talk the other subsidiaries

Clayton Homes

Clayton Homes does manufactured housing. The Manufactured Housing Institute’s Q4 2024 market share report shows (Year-to-date 2024):

Clayton Homes: 48.43% share

Skyline Champion: 21.79%

Cavco: 14.88%

So they are the dominant player by a lot in this segment. This could be disrupted by a new market entrant, but again, manufactured housing is a capitally intensive business. It'd be very hard to go toe-to-toe with Berkshire on capital.

Forest River (RVs)

RVDA data for U.S. retail registrations (2022) shows market share leaders by category:

Travel trailers: THOR (41%), Forest River (33.8%), Grand Design (7.6%)

Fifth wheels: THOR (43%), Forest River (29.6%), Grand Design (18.5%)

…and similar patterns across motorhome categories.

Forest River is competing as the #2 scale player in key RV segments (behind Thor, ahead of others), which often confers purchasing scale, dealer influence, and breadth of product lineup.

But RVs are cyclical, and scale doesn’t remove cyclicality. This is a small business for Berkshire, so I'm not too worried about this one.

Precision Castparts (aerospace components)

The competitive set is specialized aerospace/industrial component suppliers—most notably Howmet Aerospace and other forged/cast/fastener suppliers. (This is not a “10,000 competitors” industry.)

Aviation Week coverage highlights the strategic importance and concentrated nature of advanced castings/engine components (where a handful of suppliers matter).

PCC’s competition is not about mass marketing; it’s about qualification, long-term programs, and manufacturing excellence. Berkshire's ownership helps with the long and capex-heavy cycles.

Lubrizol (specialty additives)

A typical competitor set in lubricant additives includes Afton Chemical, Infineum, Chevron Oronite and others (industry reports commonly group these as key players).

This is closer to an oligopoly/“few big R&D players” structure than a fragmented commodity market, which can support durable competitive positions so long as the company stays ahead technically and commercially.

NetJets (fractional aviation)

NetJets competes primarily with other fractional ownership operators like Flexjet (and, depending on the customer, premium charter operators). Industry commentary often frames NetJets as the category leader in fractional.

In a trust/safety/service-heavy category, being the dominant operator can matter. Berkshire ownership can also be a credibility/continuity advantage for high-end customers.

Distribution + Travel Centers

McLane (distribution)

In convenience distribution, a core competitor is Core‑Mark (now within Performance Food Group). CSP’s distribution coverage explicitly discusses investments and competitive focus at McLane and Core‑Mark.

Berkshire’s advantage is less “McLane is unbeatable” and more: McLane can make long-run investments (automation, systems, capacity) without financing constraints typical of smaller distributors.

Pilot Travel Centers (truck stops)

Pilot Travel Centers (Pilot Company) holds a significant competitive advantage as the largest operator of travel centers in North America, acting as a critical, high-volume, and modernized "energy and experience provider" for both professional fleets and passenger vehicles. Owned by Berkshire Hathaway, Pilot leverages a network of over 870 locations in 44 states and six Canadian provinces... this beats the second place (Love's) at 644 locations.

This is a network/real-estate/logistics adjacency business: fuel supply, loyalty programs, fleet relationships, amenities, and increasingly EV charging / alternative fuels infrastructure.

Berkshire’s edge here is primarily balance-sheet-backed ability to invest through transition periods (fuel mix changes, EV infra buildout), while competing with other large, well-funded operators (Love’s; bp/TA). And, their history of operating excellence.

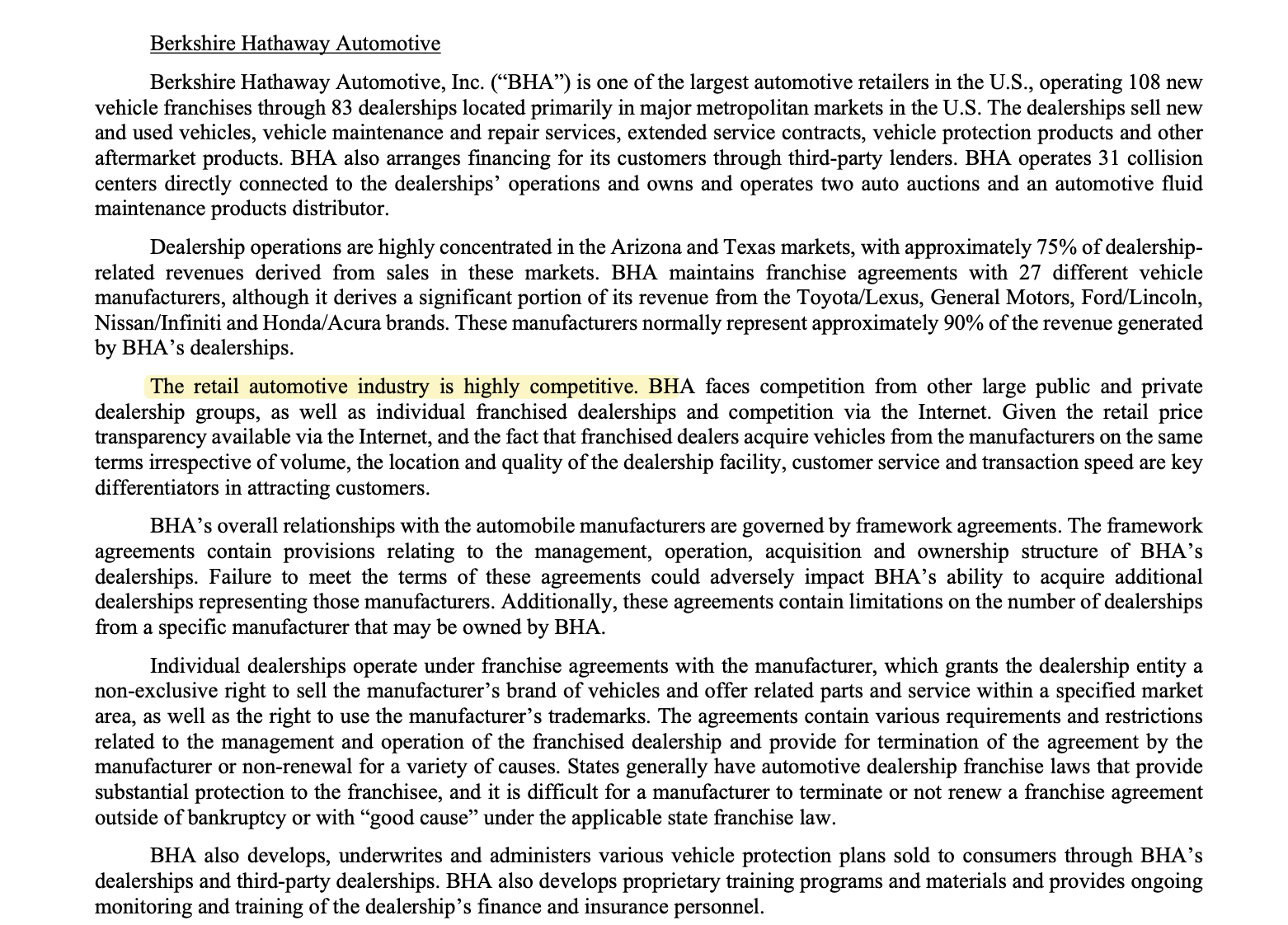

Berkshire Hathaway Automotive

I couldn't write a puff piece about every single business having an amazing competitive advantage. BHA is, in my opinion, the smallest moat.

Warren Buffett created Berkshire Hathaway Automotive in 2014 by acquiring the Van Tuyl Group to enter the highly fragmented, profitable auto dealership industry with a long-term strategy for consolidation and growth. He viewed it as a durable, cash-generative business, leveraging it to expand his portfolio into "planes, trains, and automobiles"

But what does make Berkshire so wonderful is that I DIDN'T NEED TO GET ALL FORENSIC ON THIS. THEY TOLD US ITS THEIR TOUGHEST BUSINESS.

The killer line (from a “competitive advantage” lens) is that franchised dealers acquire vehicles from manufacturers “on the same terms irrespective of volume".

Now, we're finally onto the "Holding Company" part.

If you zoom out, Berkshire’s “competitors” aren’t only Progressive, Union Pacific, or Thor Industries.

Berkshire also competes against:

Private equity (Blackstone, KKR, Apollo, etc.) for buying businesses,

strategic buyers (industry incumbents),

and other permanent capital pools (Brookfield; insurance-holding-company models like Markel/Fairfax, etc.).

Why Berkshire has an edge here

Berkshire’s public filings and shareholder communications repeatedly emphasize the company as a long-term, hands-off owner with significant financial capacity.

This matters competitively because in many acquisitions, the seller is choosing not only a price but an “owner profile.” Berkshire’s owner profile is unusual relative to private equity (which often has finite fund lives) and relative to strategic buyers (which often need synergies and integration).

We all know the bad name that PE is getting in the US (I hate my dentist now that they're part of a PE group). Berkshire does not need to squeeze every dollar out of a business like PE does. This makes them the "buyer of choice"

This “buyer-of-choice” positioning is not a moat you have to believe in blindly; you can observe it in the way Berkshire continues to attract sellers and maintain a very large stable of autonomous subsidiaries.

So does Berkshire have a competitive advantage?

Simply put, YUP. They intentionally built that way over 40 years ago. It's amazing what they've built - if capital allocation was an art, Buffett is Da Vinci.

Sentiment: Very, Very Bullish