DUOL

Duolingo Inc

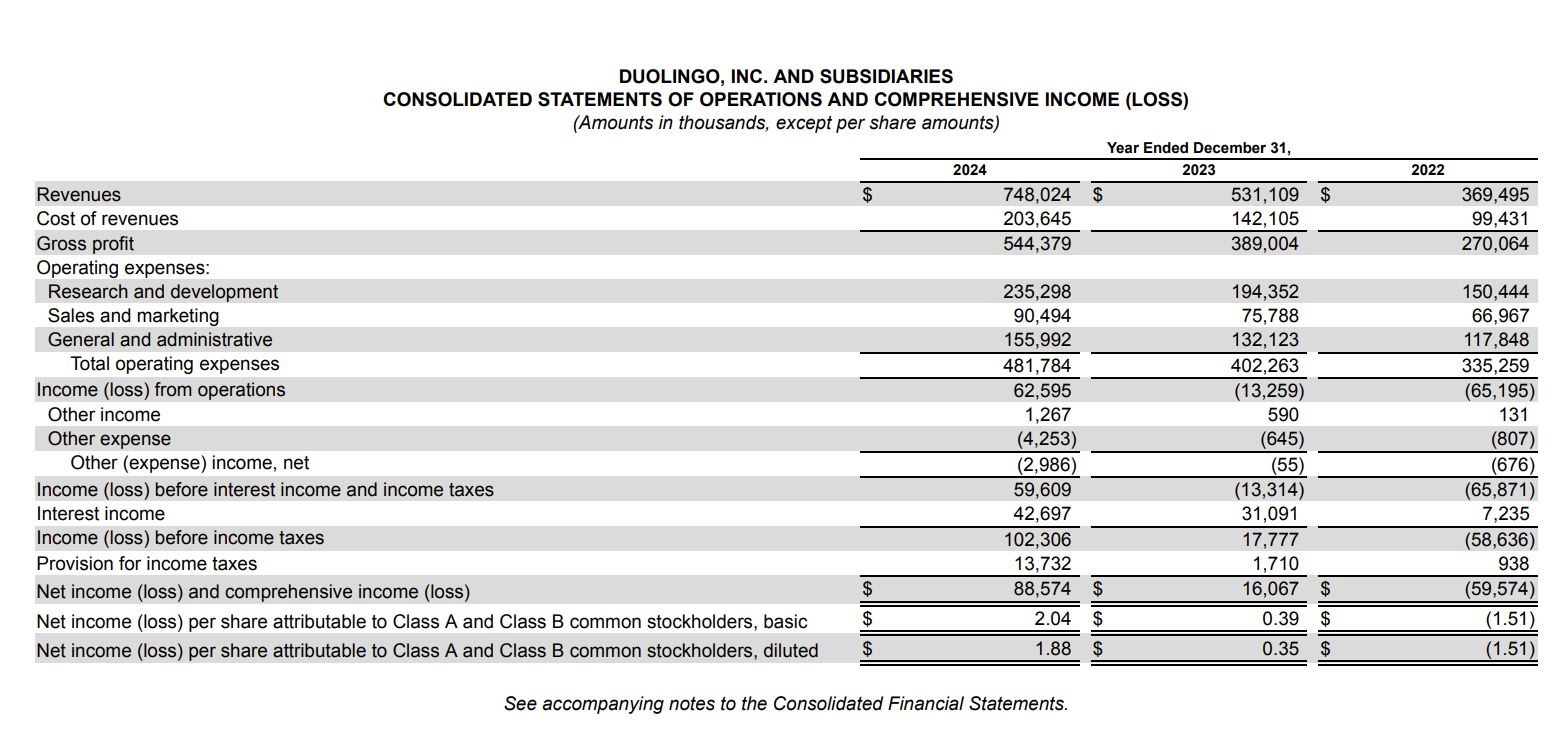

Duolingo's Income Statement

Understand The Income StatementFrom the 2024 annual report...

Green Flags:

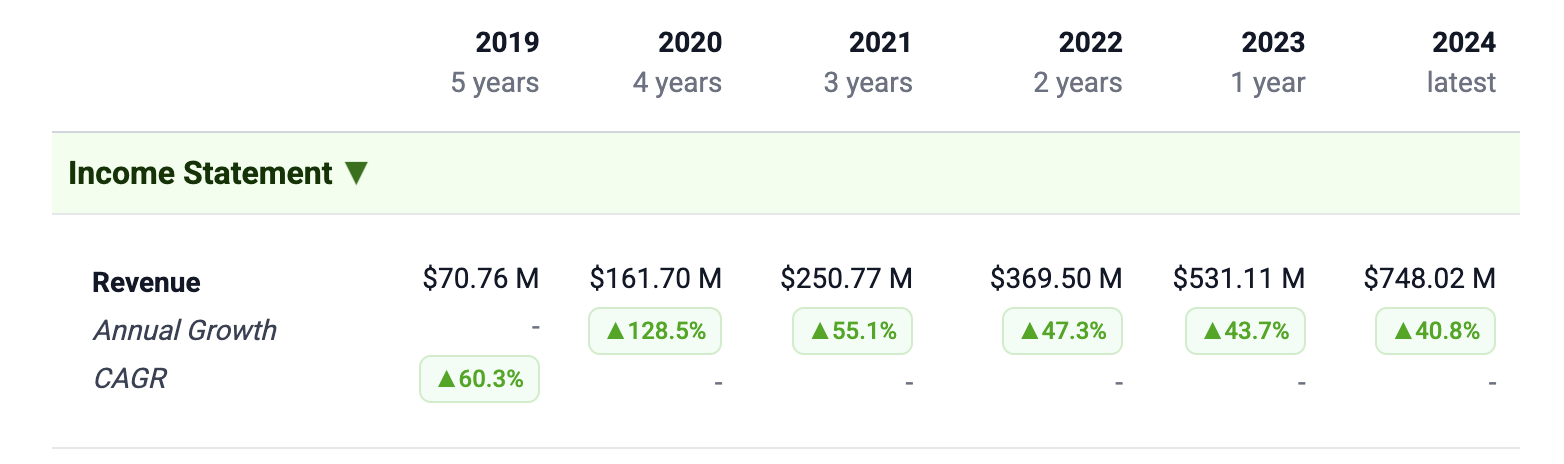

Rapid Revenue Growth... like a crazy amount of growth.

60% 5-year CAGR for revenue growth is insane. Is it sustainable? Probably not, but that's what my research will bear out.

Paid Subscriber growth skyrocketed from 6.6M at the end of 2023 to ~9.5M at the end of 2024 (+43% YoY). And that's recurring. 80%+ of their revenue comes from paid subscribers, so this makes sense.

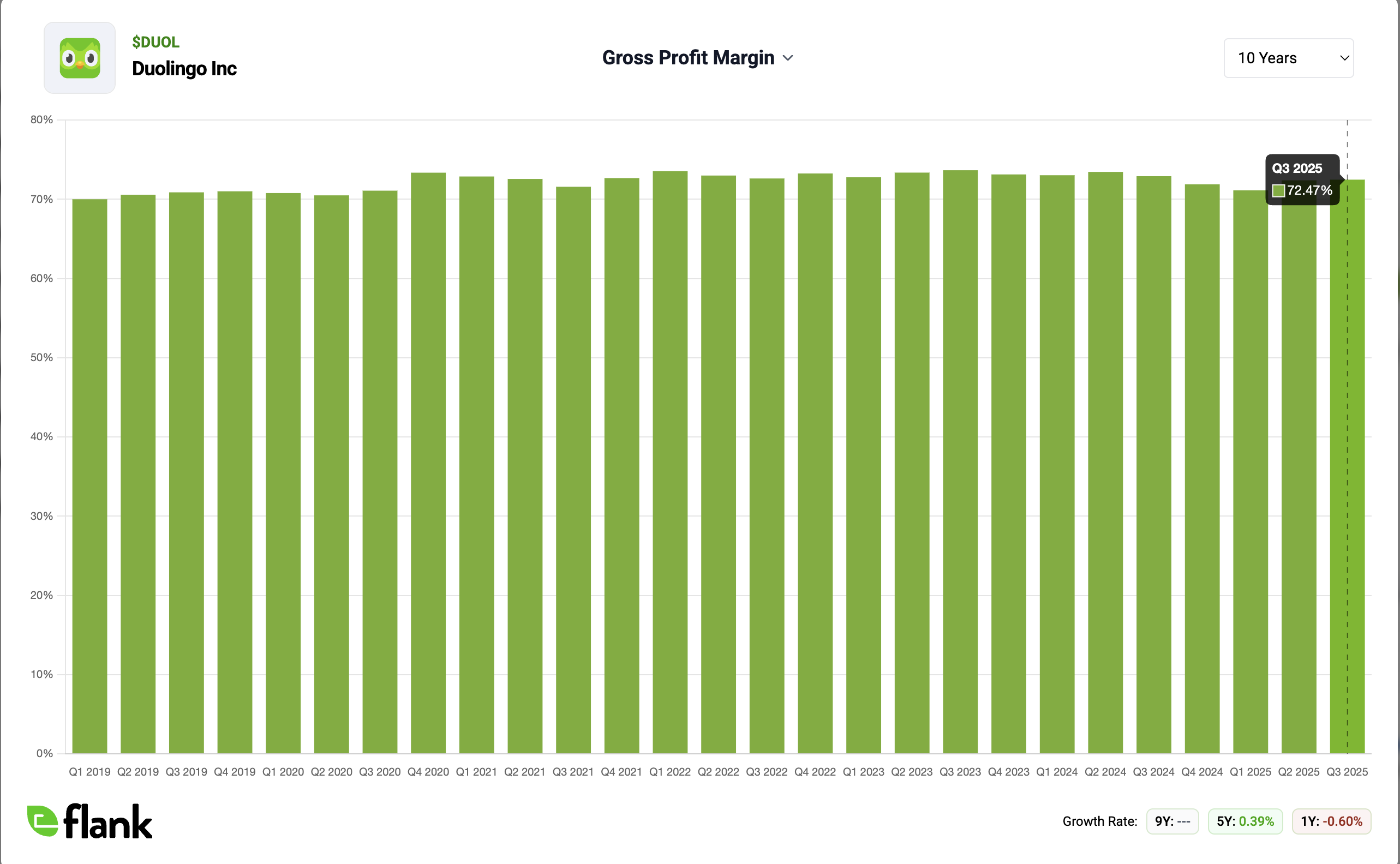

Gross profit margin holding strong at ~73%

Gross profit margin is an indicator of the economics of the core business. A consistently high gross margin signals that the company isn’t competing exclusively on price.

I wasn't sure what they would consider in their "cost of revenues" (which is how Gross profit margin is calculated), so I wanted to take a look.

So, they calculate Cost of Revenues by adding:

third-party payment processing fees

hosting fees

generative AI costs

To a much smaller extent:

customer support costs

wages and stock-based compensation for customer support employees

Nothing too outside of the usual there!

So overall, I am very happy with the economics of the business. This is a quality business model.

Yellow Flags

Growth is slowing (but still very high)...

If you look at the revenue chart above, we have 128% growth in 2020, 55% in 2021, 47% in 2022, 43% in 2023, and 40% in 2024. That's decelerating. I'll need to include that in my valuation.

High Research & Development costs

In 2024, R&D was $235M, on $748M of revenue... meaning 31% of revenue goes to R&D.

That's a little higher than I'd like to see. The big question is: whether R&D costs will need to remain high to keep improving the platform.

I think the answer is most likely yes, given their focus on AI development.

Stock Based Compensation

Stock-based compensation is a significant part of costs: $110.5M in 2024 (vs. $88.6M GAAP net income). This inflated expense depresses reported earnings and dilutes owners, so it’s a cautionary point – true cash profitability is higher, but owners are paying via dilution.

This is normal in a tech startup, but still not great to see... but if it it means early employees will be "owners of the business" and stakeholders, I'm game.

Red Flags

Owner's Earnings is still negative.

Since SBC is so high (~125% of net income), our Owners Earnings are actually negative.

Owners earnings are Buffett’s term for cash profits available to owners.

This is a risk to watch: if Duolingo cannot gradually tame stock compensation relative to revenue, it may indicate difficulty in attracting/retaining talent without heavy equity grants, which could weigh on per-share earnings growth for investors.

Sentiment: Bullish