DIS

Walt Disney Co

After a lost decade, Disney is back

For Disney shareholders (like myself, I bought in 2023 after the return of Iger), the last few years-- nee decade have been painful.

The stock trades today around a market cap of $208B—the same level it hit back in August 2015, when subscriber losses at ESPN sent shockwaves through the entire media industry.

ESPN, then Disney’s profit engine, was exposed as vulnerable. The stock fell 9% in a single day, dragging down Discovery, Time Warner, Viacom, Comcast, and CBS. If ESPN could be disrupted, the whole television economy could.

But Disney, in true form, is transforming again. ESPN has shrunk enough that it no longer dictates the company’s fate. A full ESPN streaming service is set to launch, the core streaming business is finally profitable, and theme parks are producing record profits. Movies remain mixed—some flops, some dependable winners—but the brand pipeline is alive with Avengers, Toy Story, Avatar, and Fantastic Four sequels.

As Morgan Stanley’s Benjamin Swinburne put it: “It was a media company that owned theme parks. Now it’s a theme park company that owns media assets.” But we can't ignore their incredible IP- that has embedded itself into every generation that walks the earth today.

The Numbers That Matter

Stock Performance: Over the past decade, Disney has returned just 10% (dividends included), compared with 253% for the S&P 500 and nearly 955% for Netflix. But in the past year alone, Disney stock has surged 38%, outpacing the S&P 500 by 19 points.

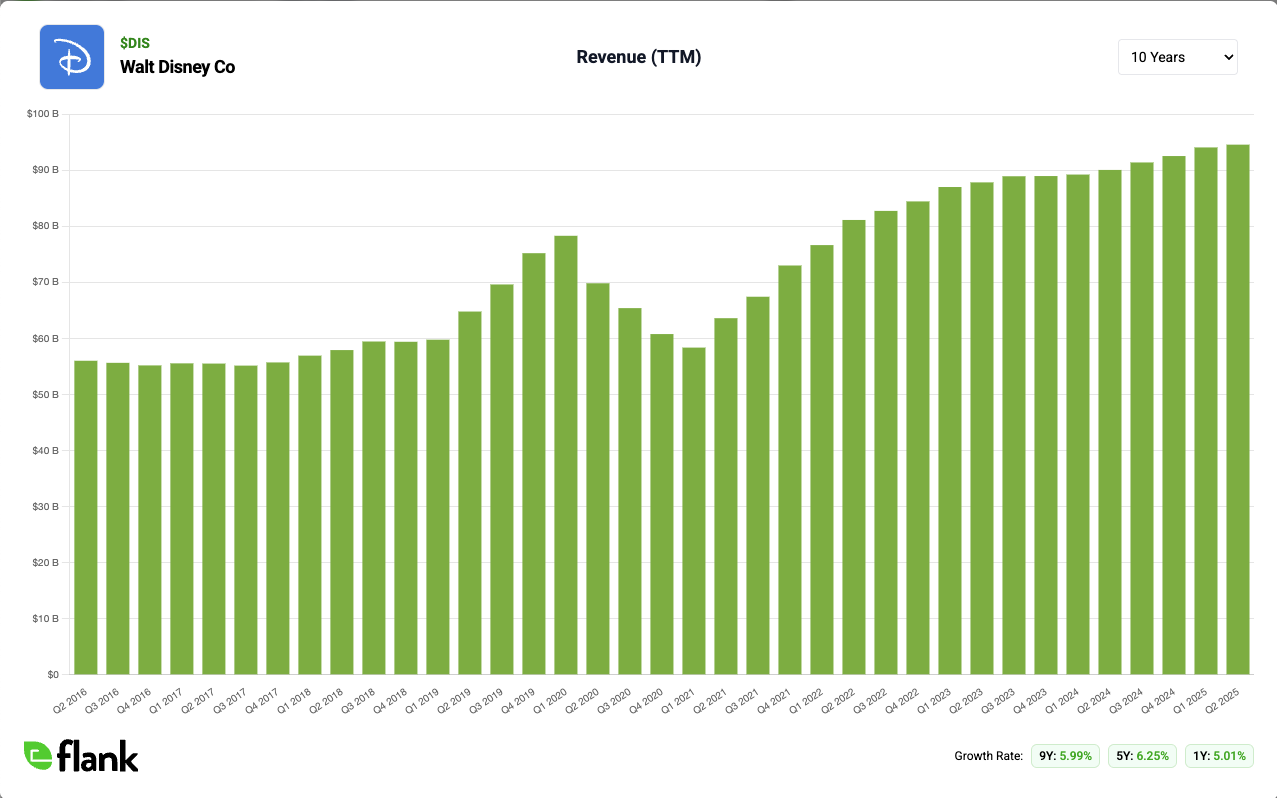

Revenue: Revenue has been growing at a slow rate - averaging 6% growth over the past 10 years.

Valuation: At ~18 ttm earnings, the stock isn’t cheap, but renewed growth could justify the multiple.

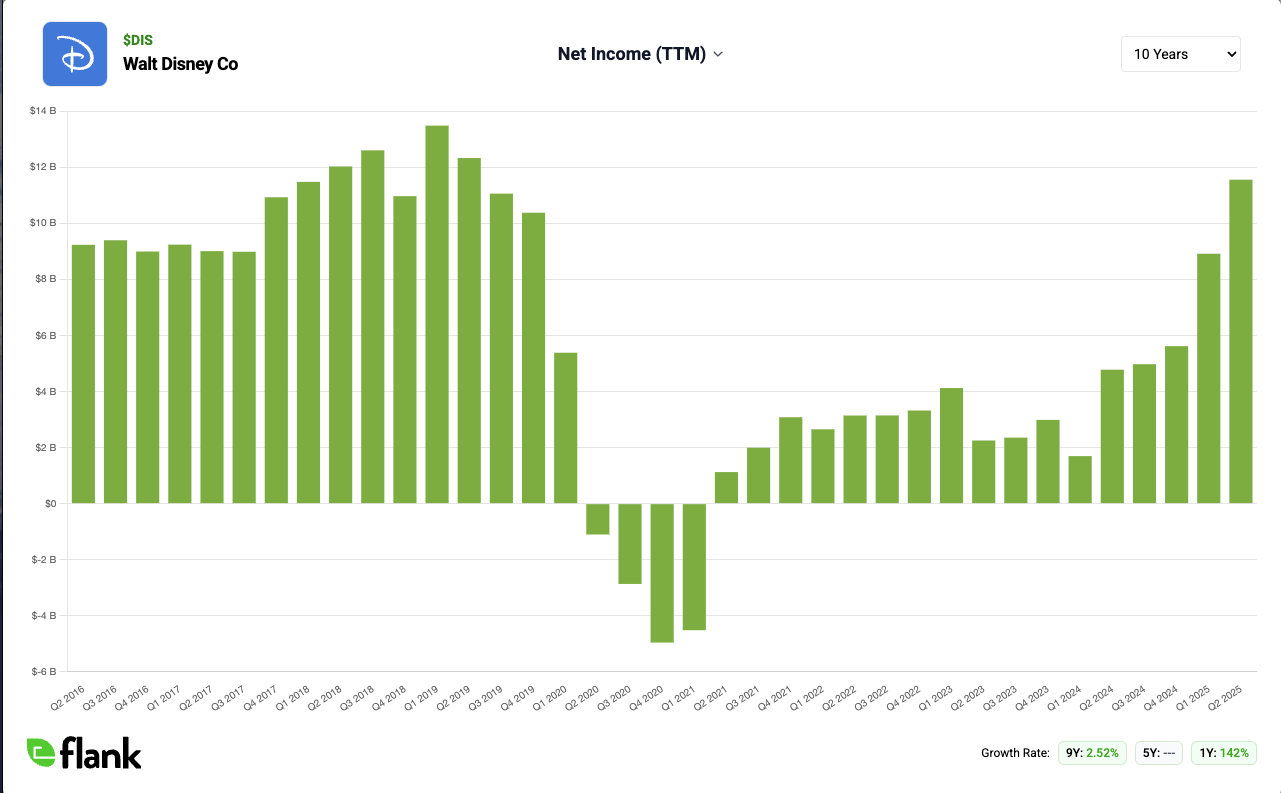

Profits: Operating profit in 2023 hit $15.6 billion, just shy of its all-time high in 2016. Wall Street expects $17.5 billion this year (+12%), with another $5 billion in growth over the next three years. In terms of Net Income, the large investment into Disney+ was dragging down the bottom line, but with the service approaching proftiability, we're seeing Net income spike-- it's up 142% yoy

Cash Cow Shift: ESPN once funded Disney’s empire—including acquisitions of Pixar, Marvel, and Lucasfilm. Today, it’s the parks. Disney’s Experiences division delivered $9.3 billion in profit last year, 59% of companywide operating profit.

Risks and Realities

Streaming: Disney+ is profitable but not dominant. Analysts call it “stuck in the middle”—neither a cash furnace like some rivals, nor a true pay-TV substitute like Netflix. At best, it could generate about 20% of Netflix’s operating profit in a few years.

Movies: A weak release slate and pandemic aftershocks hurt box office results. But 2025 and 2026 could bring the biggest pipeline since pre-Covid.

ESPN: The full streaming launch (expected at $29.99/month) is a double-edged sword. It could speed cable cancellations but also open up direct monetization of tens of millions of cord-cutters.

Competition: YouTube now outruns both Netflix and Disney in total viewing hours, and it’s inching into sports. This is the industry’s existential threat.

The Long-Term Lens

Walt himself used television to finance Disneyland in 1954, proving the genius of leveraging one business to fund another. Bob Iger did the same with ESPN’s profits to build the IP empire. Today, parks and cruises are the cash machine. That cycle of reinvention has been Disney’s DNA for 100 years.

Analysts are bullish—more recommend buying Disney than buying Netflix. But Buffett-style investing asks: is this a durable franchise at a fair price? The answer depends on whether you believe Disney can:

Maintain pricing power in parks.

Turn streaming into a steady, if unspectacular, profit stream.

Rebuild its movie slate to fuel both box office and park tie-ins.

If those hold, double-digit annual returns are possible—even if Disney never catches Netflix.

Final Take

Disney won’t be the fastest horse, but it may be one of the safest in Hollywood. With Iger determined to go out as a “hero CEO” by 2026, the next two years could mark the company’s strongest stretch in over a decade. For long-term investors, Disney looks less like a broken media conglomerate—and more like what it has always been: a survivor with the rare ability to transform.