General

The Perils of AI Megadeals

We've all seen this chart

Michael Burry even tweeted it, right after shorting Nvidia and Palantir.

I wanted to dive into this story more after reading a wonderful article from Randall Forsyth in Barron's last week.

We are experiencing a historic boom in Artificial Intelligence. That's beyond debate.

AI promises to be as profoundly transformative to our society as any boom in the past 200 years: railroads, electricity, the internet boom.

But what also followed those previous capital expenditure booms was a bust, as a new report from BCA Research shows

In that report BCA draws 5 lessons following Capex Booms. Specific booms covered include: The railway booms of the 19th century; the electrification boom of the 1920s; the internet boom of the late 1990s; and various oil booms. I'll talk about the first three, check out the report for the oil boom.

Let's take a look.

But first, if you need a reminder on what Capex is... it's Capital Expenditures

Basically, Capex are funds companies allocate to acquire, upgrade, and maintain essential physical assets (like a data center for AI or a new gigafactory for Tesla)

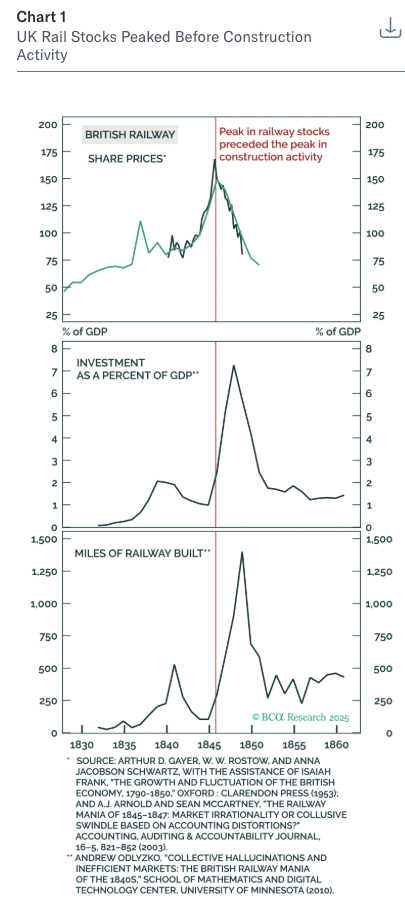

Railway Boom in UK/US - 19th Century

The first railways used steam to carry coal. That changed in 1830 when the introduction of the Liberpool and Manchester Railway showed passenger travel could also be highly profitable.

This led to the ocnstruction of new railway lines all across the UK. Railway stocks surged, doubling between 1843-1845.

And then the y crashed mid-1845. By 1847, Railway construction exceeded 7% of British GDP (!).

By the end of that decade, the rail index had fallen 65% (Chart 1)

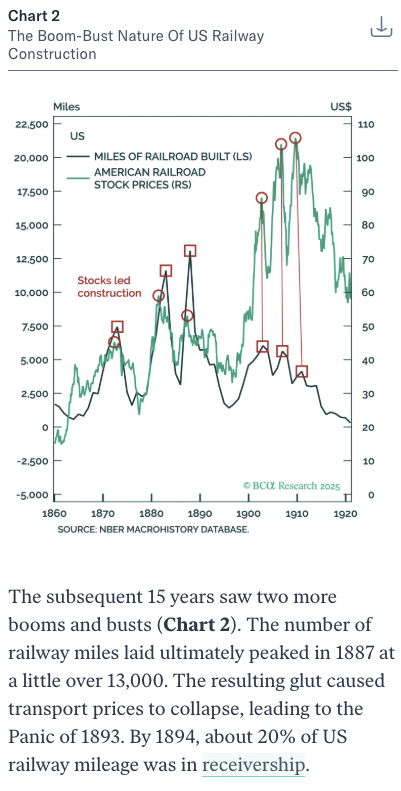

In the US, the story is similiar. Railway construction exploded after the Civil War + Railway stocks rose in value through the 1860s, peaking around 1872.

The subsequent decline in railway stocks culminated in the Panic of 1873 where the market would be closed for ten days in September that year!

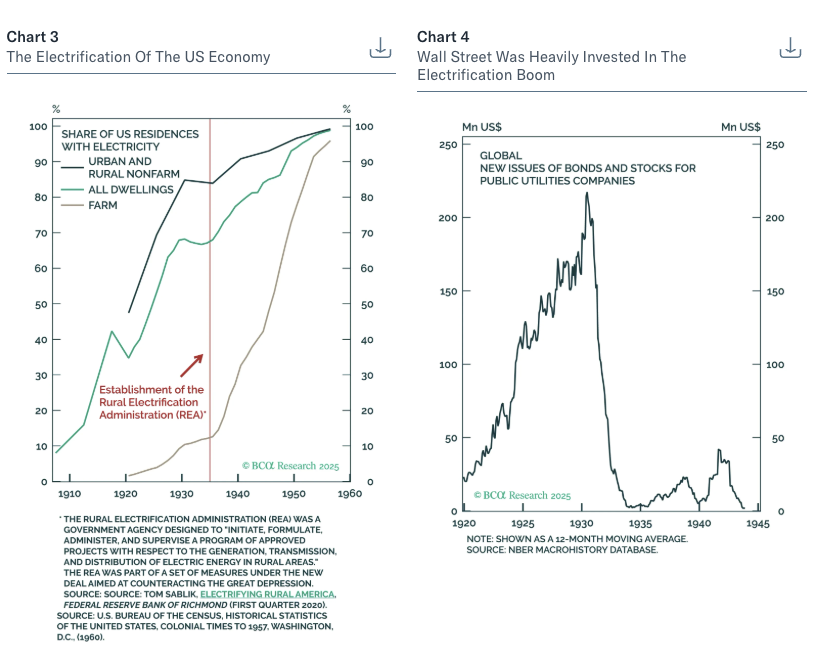

The Electrification Boom of the 1920s

Electified US households were 8% of all homes in 1907. This rose to 35% of homes in 1920 and 68% by 1930.

Wall St invested heavily in electrification. Stocks and bonds of utility companies were often marketed as appropriate for “widows and orphans.” This turned out to be far from the truth. Holding companies ended up controlling over 80% of US electricity generation by 1929.

Most of these companies were consolidated under pyramidal capital structures, which made them highly vulnerable.

This all unraveled in the 1929 stock market crash. US electric utility construction outlays peaked in 1930 at $919M before plunging to $129M by 1933.

The Late-1990s Internet Boom

Like most booms, the internet one was based on real innovation – the internet raised productivity and changed the way people lived and worked.

However, as often occurs during booms, investment spending got ahead of itself, setting the stage for a bust.

Tech-related capital spending rose from 2.9% of GDP in 1992 to a peak of 4.5% in 2000. For context, KKR reports that AI-related capex is ~5% of US GDP in 2025, and JPM reports this CAPEX contributed 1.1% to GDP growth this year.

The surge in spending put pressure on corporate balance sheets. Corporate debt rose while free cash flow deteriorated. Free cash flow among telecom companies peaked in late 1997 and then fell for two straight years before plunging in 2000

The Article then gives us 5 lessons, I'm going to simply list them here...

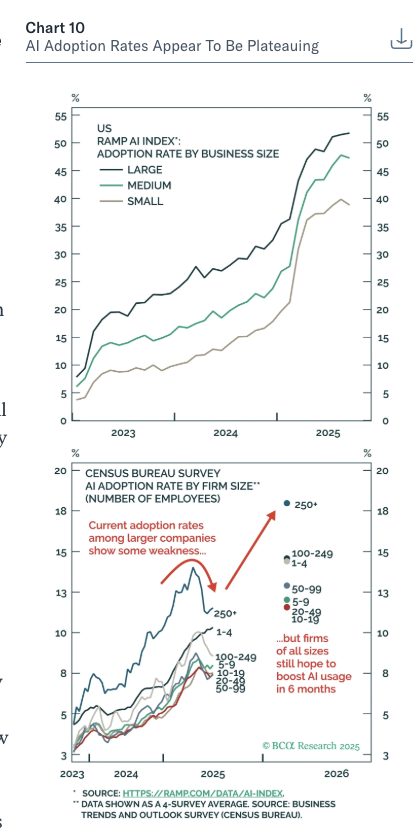

Lesson #1: Investors failed to appreciate the S-shaped nature of technological adoption

Actual adoption rates of AI are slowing (Chart 10). I've talked about Amara's Law plenty, this S-shaped adoption curve is just another way of saying that.

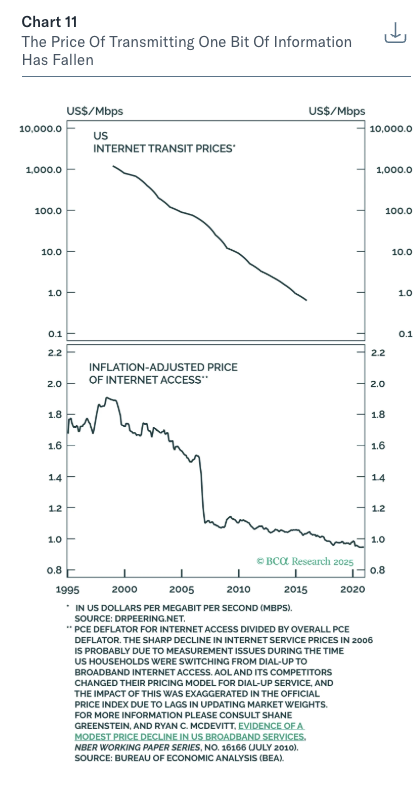

Lesson #2: Revenue forecasts underestimated the degree to which prices would fall

Slowing adoption is one reason why Capex booms, but another just as big reason is price deflation.

The article goes into how internet traffic grew an average of 67% a year from 1998-2015, but the price of transmitting one bit fell just as quickly (chart 11)I think this is the biggest risk. And we saw it earlier in the year with Deepseek. If we get more efficient and AI-queries, then capex spending while plummet.

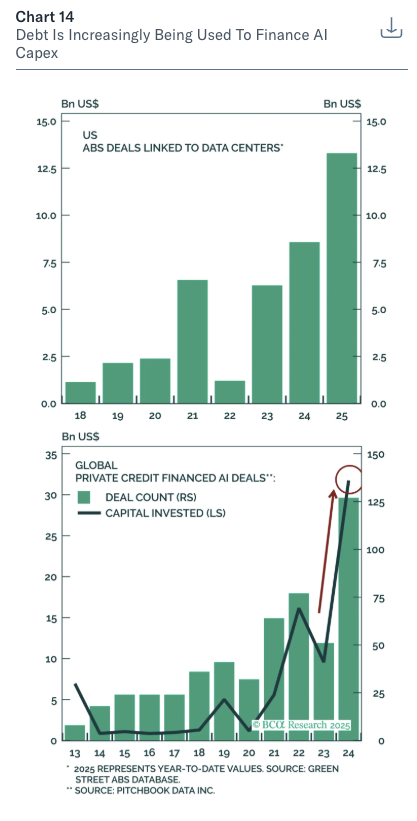

Lesson #3: Debt became an increasingly important source of financing

Until recently, companies weren't using debt to fund their capex spending for AI.

This has started to change (Chart 14)

In October, Meta announced a $27B data center financing deal (to be housed in an off-balance sheet SPV!!) and Oracle tapped the bond market for $18B.

Increased wariness about monster hyperscaler borrowings has sent the cost of insuring their debt against default soaring

Credit default swaps more than doubled for Oracle since September, after it issued $18 billion in public bonds and took out a $38 billion private loan. CoreWeave’s CDS gapped higher this past week, mirroring the slide of the data-center company’s stock.Lesson #4: Asset prices peaked before investment declined

Straight from the article, since they covered it wonderfully:

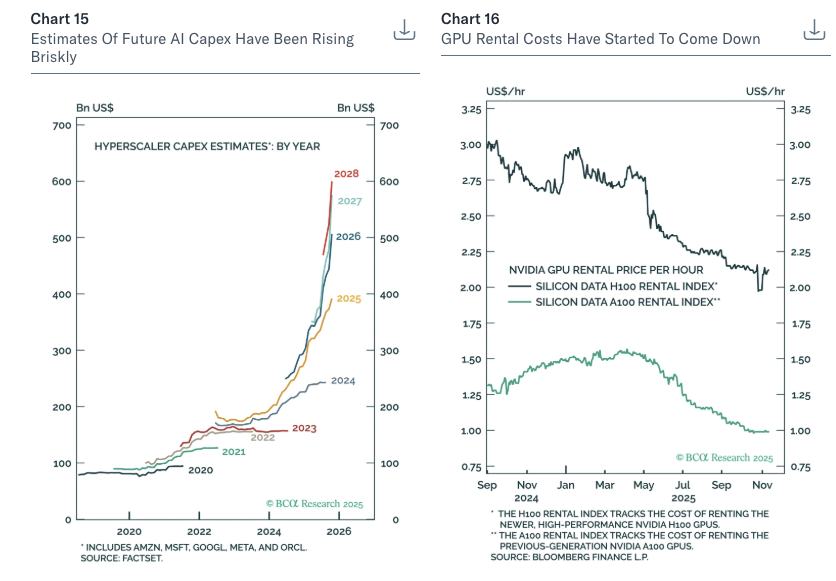

"During past capex booms, equity prices have typically peaked before investment declined. And even when investment fell off its highs, it usually did so at levels that continued to add to excess capacity.This suggests that investors should not wait for evidence that AI capex has rolled over. By the time that evidence is apparent, AI stocks will have fallen considerably.

Instead, investors should monitor four things. The first is revisions to analyst capex estimates. Estimates of future capex will likely start falling before actual capex declines. They have been rising briskly, but if they were to flatten out, that would be a worrying signal (Chart 15).

The second is GPU rental costs. After staying resilient through May of this year, they have started to come down (Chart 16). "

Lesson #5: The capex busts weighed on the economy which, in turn, further hurt asset prices

Basically what they are saying here is that when the capex busts, market sentiment will swap.

All in all, I'm taking this as shifting my risks to be more defensive, just like Howard Marks advised (INVESTCON 4)