General

Why the P/E Ratio Is the Most Misunderstood Metric in Investing

Most new investors hear about the P/E ratio within their first week of research. Price divided by earnings. Sounds simple, right?

It is. But even experienced investors get it wrong.

In fact, P/E ratio might be the most misunderstood metric in all of investing—and misunderstanding it has cost countless investors big opportunities.

## What the P/E Ratio Really Is

At its core, the P/E ratio tells you:

How much you’re paying for $1 of a company’s earnings.

If a stock trades at a P/E of 20, it means you’re paying $20 for every $1 the company earned in the past year.

High number = “expensive.”

Low number = “cheap.”

Seems straightforward. But here’s the catch…

## The Trap: P/E Is a Static Snapshot

Dogmatic value investors miss the point. Some will say, if it’s over 20, value purists walk away. If it’s under 10, they call it a bargain.

But the E in that formula—earnings—is backward-looking (unless it's FWD P/E).

P/E is almost always based on the trailing 12 months of earnings. It tells you where a business has been, not where it’s going.

If earnings are growing faster than the market expects, today’s “expensive” stock could actually be tomorrow’s steal.

A Real Example of mine

When I first started buying Amazon back in 2012-14, its P/E ratio floated between 200-1,000.

To a strict value investor, that’s insanity.

To me, it was a bet on the future.

I saw how they were investing in huge distribution centers, I saw how Prime memberships were becoming an IQ test to the consumer. I saw they had first mover advantage in the Cloud. I read Bezo's annual report letters and knew his vision.

Yes, the P/E looked absurd. But it completely ignored what Amazon was building.

If I had judged Amazon on its P/E alone, I would’ve missed a great investment that has made me tens of thousands of dollars (almost $100K now). In my journey as an investor, I missed out on Netflix and Nvidia due to high PE ratios.

## Why P/E Misleads Investors

It punishes reinvestment. Companies like Amazon poured money into growth—distribution centers, cloud, infrastructure—which made their earnings look weak in the short run.

It ignores growth potential. Nvidia trades at ~58× earnings today. That looks steep—unless you believe in decades of AI-driven demand.

It fuels dogma. Many investors refuse to touch anything above 20× earnings, shutting themselves off from innovative businesses.

## The Lesson

P/E is useful—but only as a starting point.

It can tell you how the market is currently valuing past earnings, but it says almost nothing about:

A company’s growth trajectory

Competitive advantages

Industry tailwinds

Future cash flows

That’s why some of the world’s best investors (including Buffett himself) have bought stocks with sky-high P/Es when they believed future earnings would justify the price.

## Takeaway for Flankers

Don’t let a single number stop you from doing real research.

Look beyond the ratio.

Study the business model, growth drivers, and economics.

Ask: What do I know about this company’s future that the market doesn’t yet see?

That’s the difference between being scared off by a “high P/E” and spotting the next Tesla.

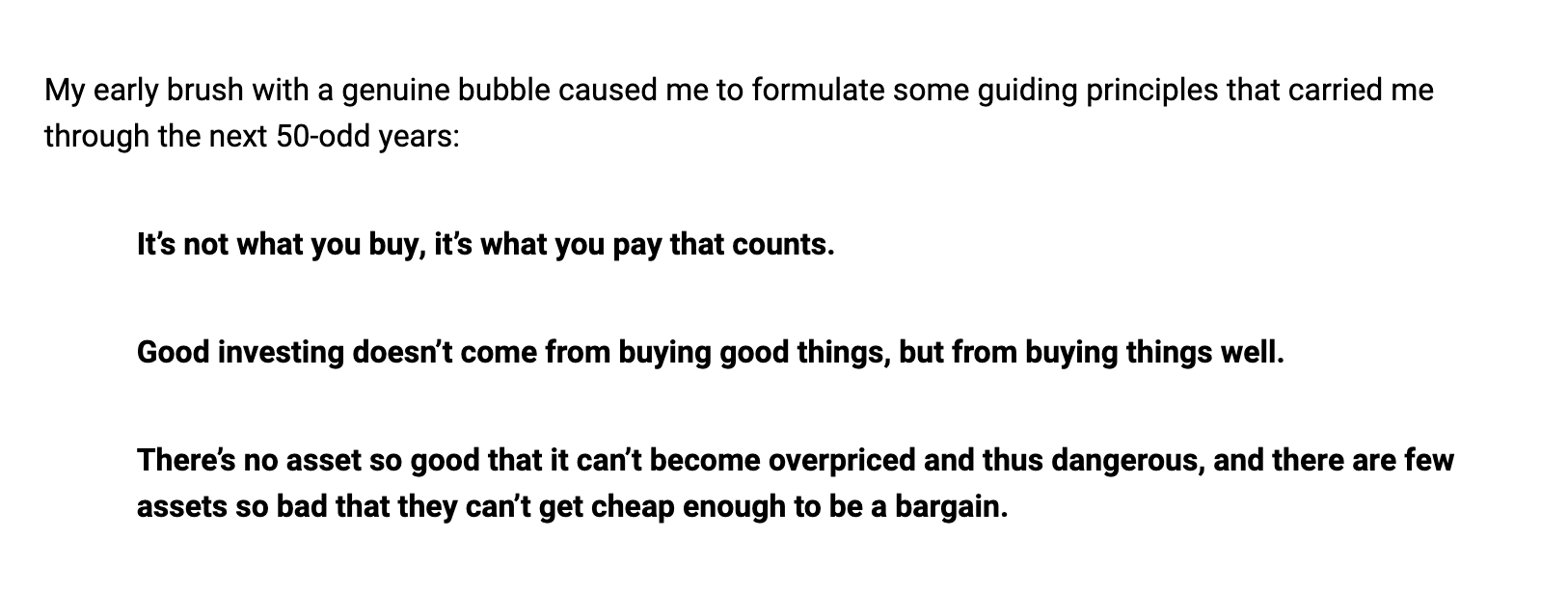

I'll close with one of my favorite excerpts from legendary investor Howard Mark's Memos:

Valuations matter. You should absolutely be wary of an extremely high PE ratio, but don't look at it in a vacuum

We made a video on this whole subject. If you prefer a more conversational format, you can check it out here.