DUOL

Duolingo Inc

Duolingo's steller Balance Sheet

Understand The Balance SheetFrom their 2024 annual report...

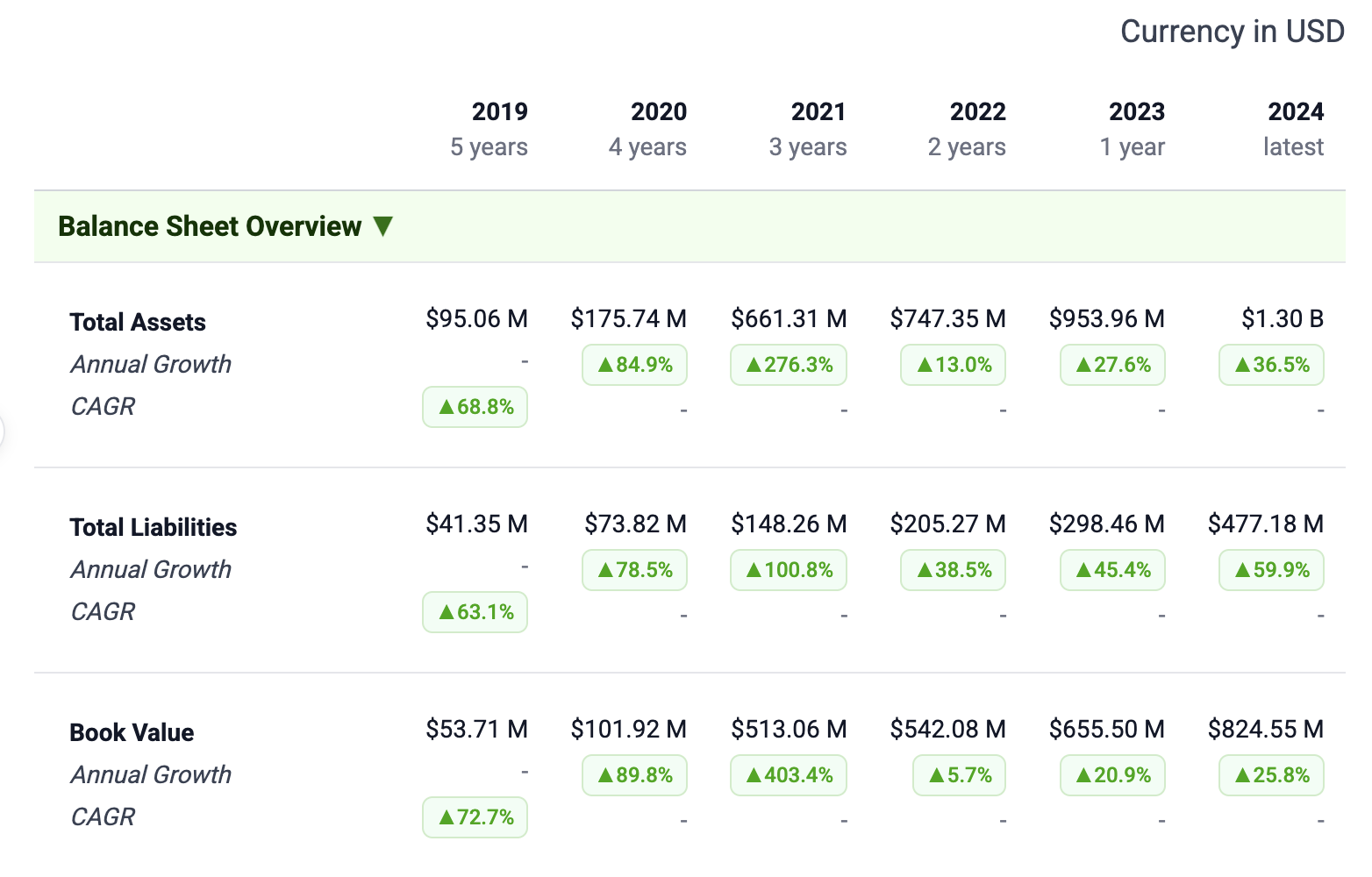

Five year trend has been fantastic. Duolingo has transformed from a pre-IPO startup to a cash-rich, almost debt-free position.

Total Assets swelled from $95M in 2019, to $1.3B in 2024 (68% CAGR).

This growth was fueled by the 2021 IPO proceeds and subsequent cash generation – cash and short-term investments alone were $554M in 2021 and climbed to $879M by 2024

Total Liabilities have also swelled from $41M to $477M over the same period, but at a slightly slower rate (63% CAGR)

Liabilities consist mainly of operating obligations (like deferred revenue and leases), with minimal interest-bearing debt. Shareholders’ equity swung from negative before IPO to $513M in 2021 and continued rising to $825M in as the company raised capital and began retaining earnings.

Green Flags

Strong Liquidity and Cash Reserves

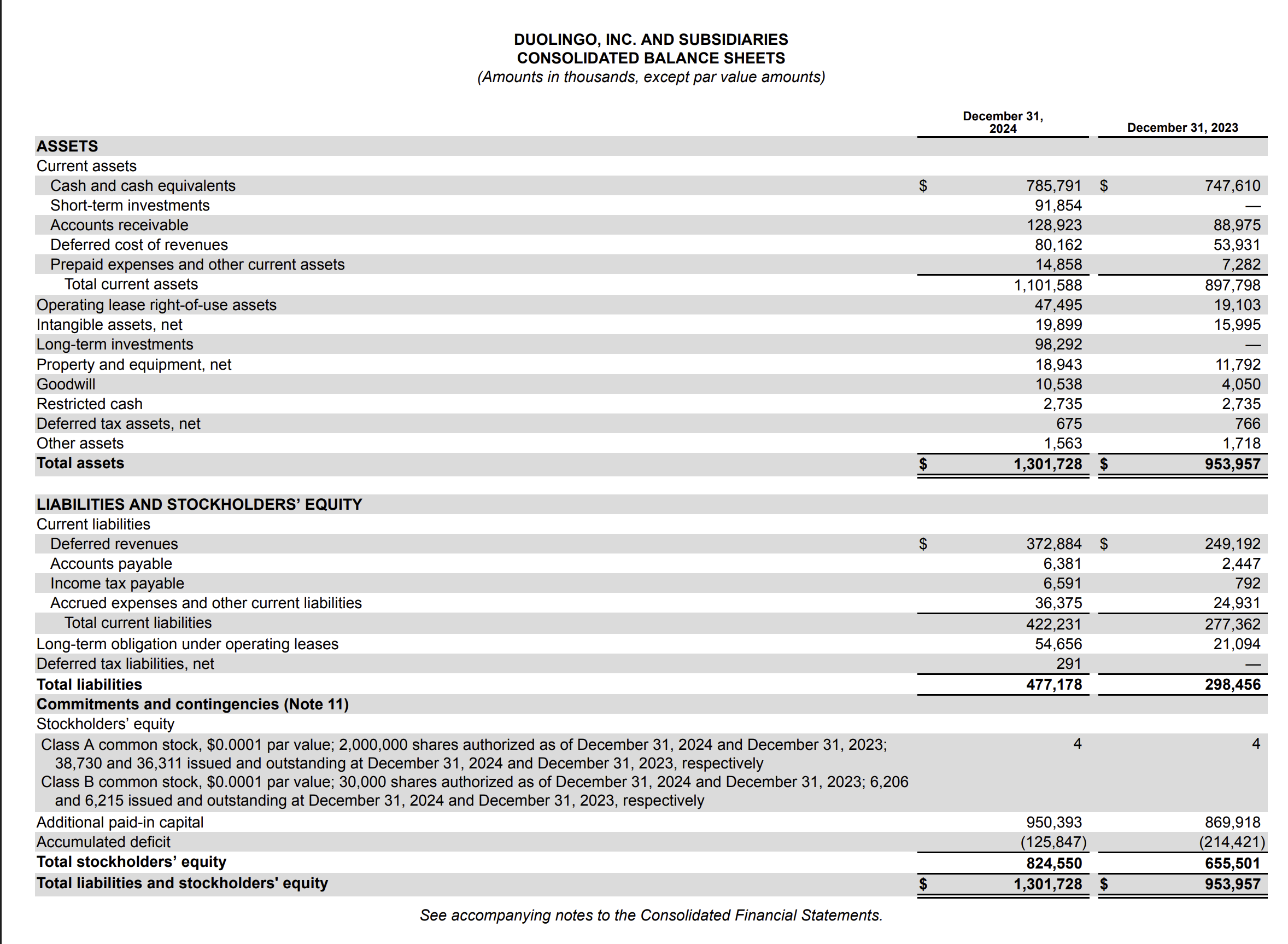

Duolingo maintains a very liquid balance sheet. As of end-2024 it held $786 million in cash and equivalents. This accounts for well over half of total assets.

Current assets ($898M in 2023, $1.10B in 2024) far exceed current liabilities ($277M in 2023, $422M in 2024). This “fortress” liquidity means Duolingo can fund operations and growth internally and weather downturns.

We like to see this as Buffett-style investors. We don't want companies that depend on external financing to survive (*cough* Six Flags)

Virtually No Debt (Low Leverage)

Reported “total debt” was only ~$57 million in 2024, which in Duolingo’s case consists entirely of lease liabilities for offices (a byproduct of accounting rules). There are no bank loans or bond obligations on the books.

Low financial risk and freedom from creditor constraints, allows management to focus on the business rather than interest payments

Deferred Revenue “Float”

A significant portion of liabilities is unearned revenue – $372.9M of current deferred revenue at 2024, up from $157.6M in 2022stockanalysis.com. These are cash payments from customers for subscriptions yet to be earned as revenue.

Duolingo’s growing deferred revenue provides internal financing for operations and is a sign of a healthy, subscription-driven model (customers are paying in advance, reflecting confidence in the service). As long as the user base renews, this float is a positive funding source that boosts cash flow (with zero leverage or dilution).

Asset-Light Business Model

Duolingo’s operations require relatively low capital assets. Property and equipment were only ~$30.9M in 2023 and $66.4M in 2024. This is tiny relative to revenue and cash.

Yellow Flags

Share Dilution (Equity Fundraising)

Duolingo’s share count has increased since the IPO. Total common shares outstanding rose from ~38.3 million in 2021 to ~42.5M in 2023 and ~45M in 2024. This ~17% increase in shares in just three years is primarily due to stock-based compensation and some follow-on share issuances for employee options.

While not unusual for a growing tech firm, dilution means each share claims a slightly smaller portion of the business.

Red Flags

Thin Retained Earnings / Short Operating History

Even after recent profits, Duolingo’s retained earnings as of Dec 2024 were still negative $125.9 million

Essentially, the company has not yet earned back its cumulative losses from earlier years (though this flipped to positive in 2025 after a one-time accounting gain)

Duolingo’s book value growth to date has largely come from raising capital (paid-in capital of $950M+) rather than from organic earnings.

Overall Sentiment: Bullish+