General

New Howard Marks Memo!

Howard Marks released a new memo titled "Is it a Bubble"

He starts the memo by talking about how certain aspects of bubbles repeat from bubble to bubble:

Marks then dissects the question, "Is there a bubble in AI", which he says requires two interrelated questions in that single question:

So the key two questions are:

the behavior of companies within the industry,

and the other in how investors are behaving with regard to the industry

Marks' says he's not qualified to answer the first question, since he's not in tech.

So he turns to the financial question. Which he brilliantly answers by saying that, "Market bubbles aren’t caused directly by technological or financial developments. Rather, they result from the application of excessive optimism to those developments" e.g. irrational exuberance.

And when those expectations change is when you see the bubble pop.

He cites some historical examples:

Marks then tells us how to operate during these times (love these paragraphs)

The two different types of bubbles

Marks goes into two different types of bubbles, which I thought was very interesting.

Mean-reverting bubbles

Inflection Bubbles

Mean reverting bubbles occur from financial fads (South Sea Company, portfolio insurance, sub prime mortgage)... they are bubbles that stirred the imaginations based on the promise of returns without risk.

In Mean-reverting bubles, there's no dream of revolutionizing. No one thought sub-prime mortages would advance human progress. These type of fad bubbles rise and fall.

Then we have inflection bubbles (railroads in 1860s, electricity in the 1920s, internet in 2000s) After an inflection-driven bubble, the world changes.

Investors decide that the future will be meaningfully different from the past and change accordingly.

We've seen this with Meta saying "we don't care if we burn a couple tens of billions of dollars -- there's greater risk in being left behind".

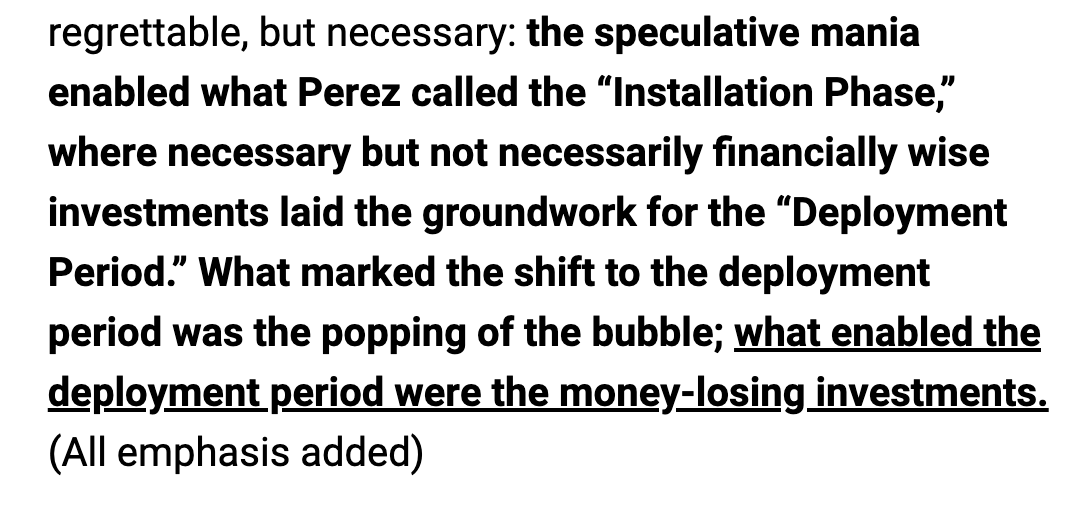

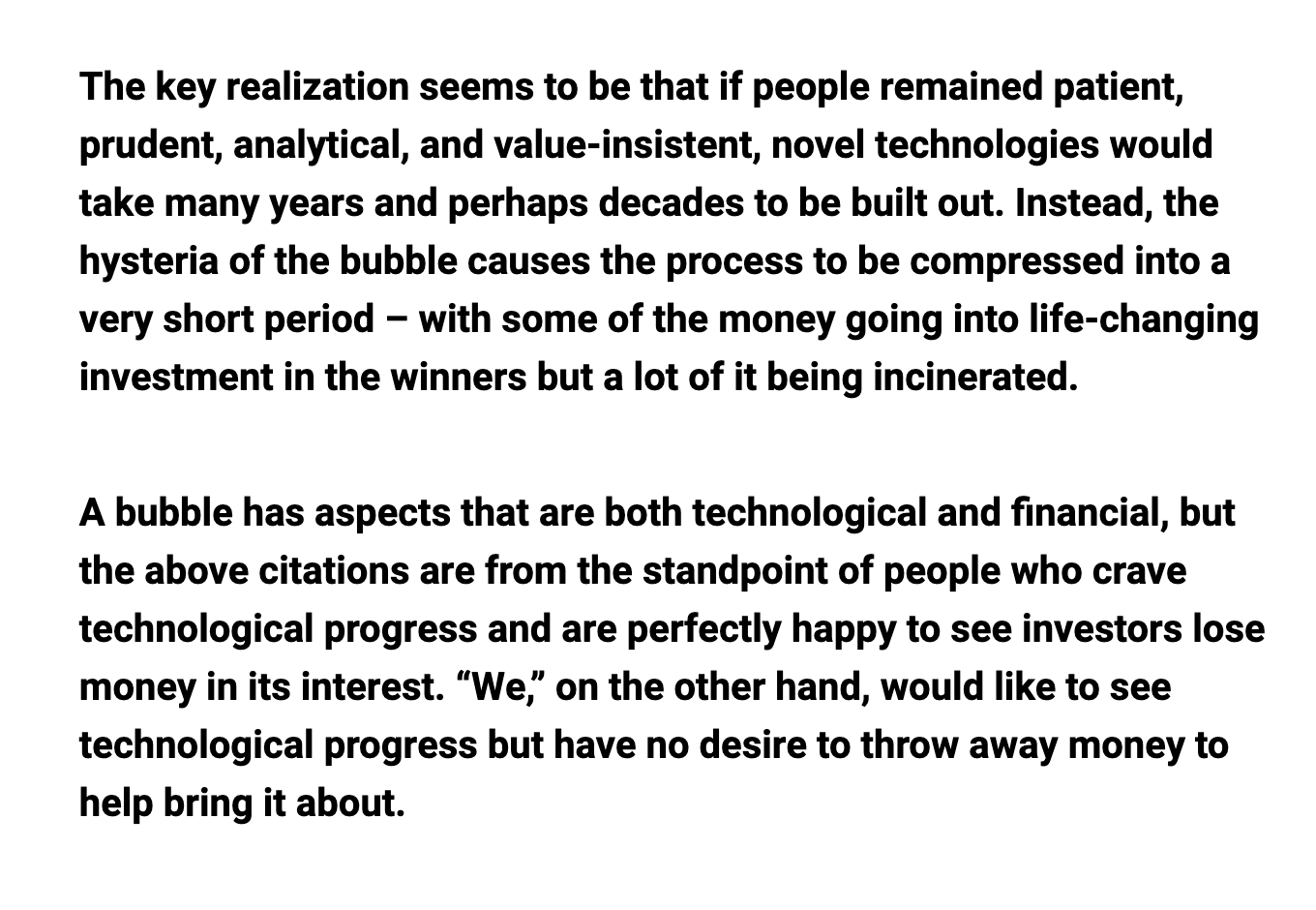

Fascinatingly, in this article, Marks is saying that this speculative mania lays the groundwork for the innovation to be funded:

The key is to not be one of the investors whose wealth is destroyed in the process of bringing on progress.

...but the fact that people do jump in is a good thing for humanity...

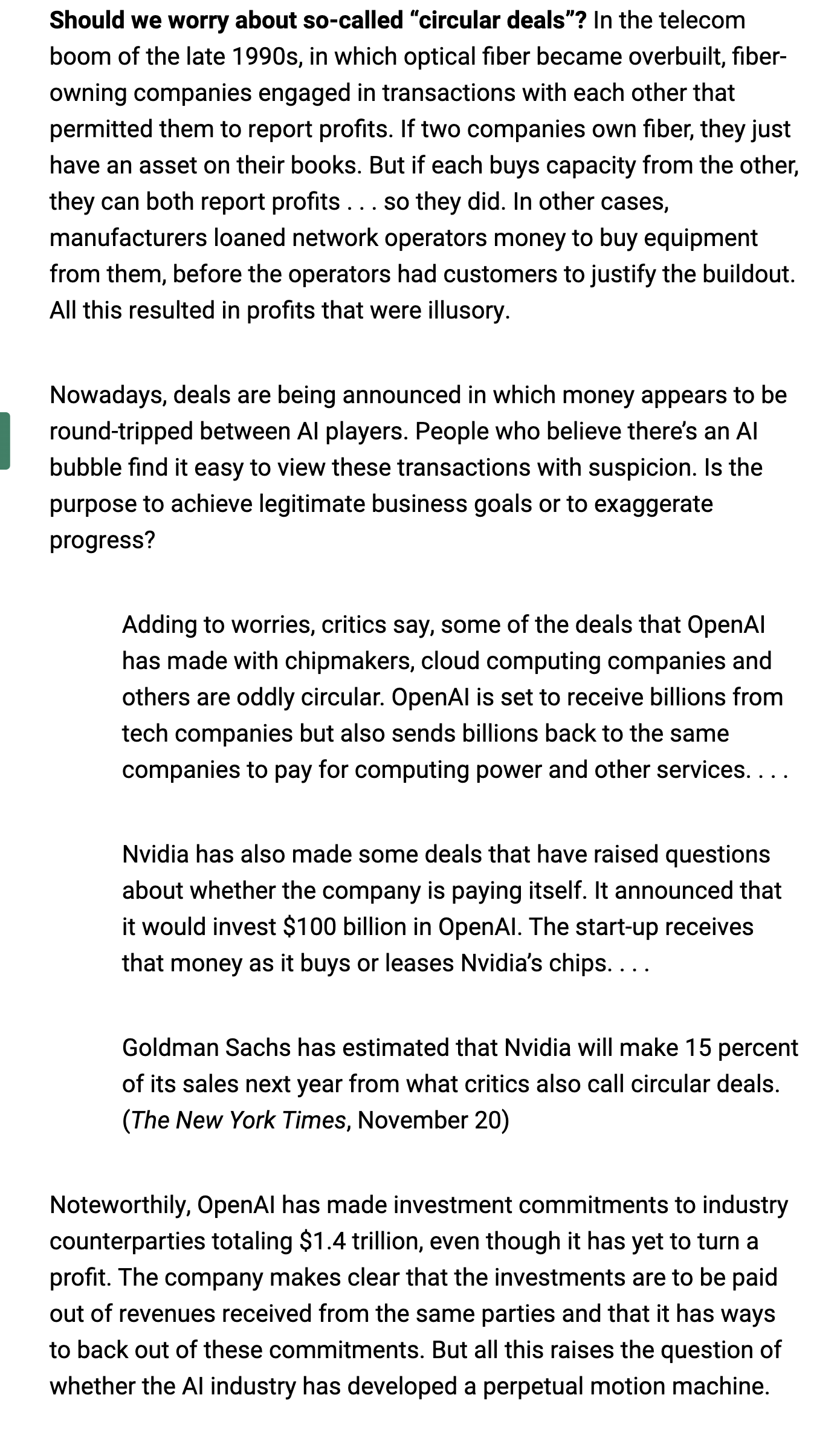

Marks then goes into the risks around Circular financing.

He also covers the insanity of some of the AI seed deals that are being financed (Mira Murati's thinking machines at $2B seed round)

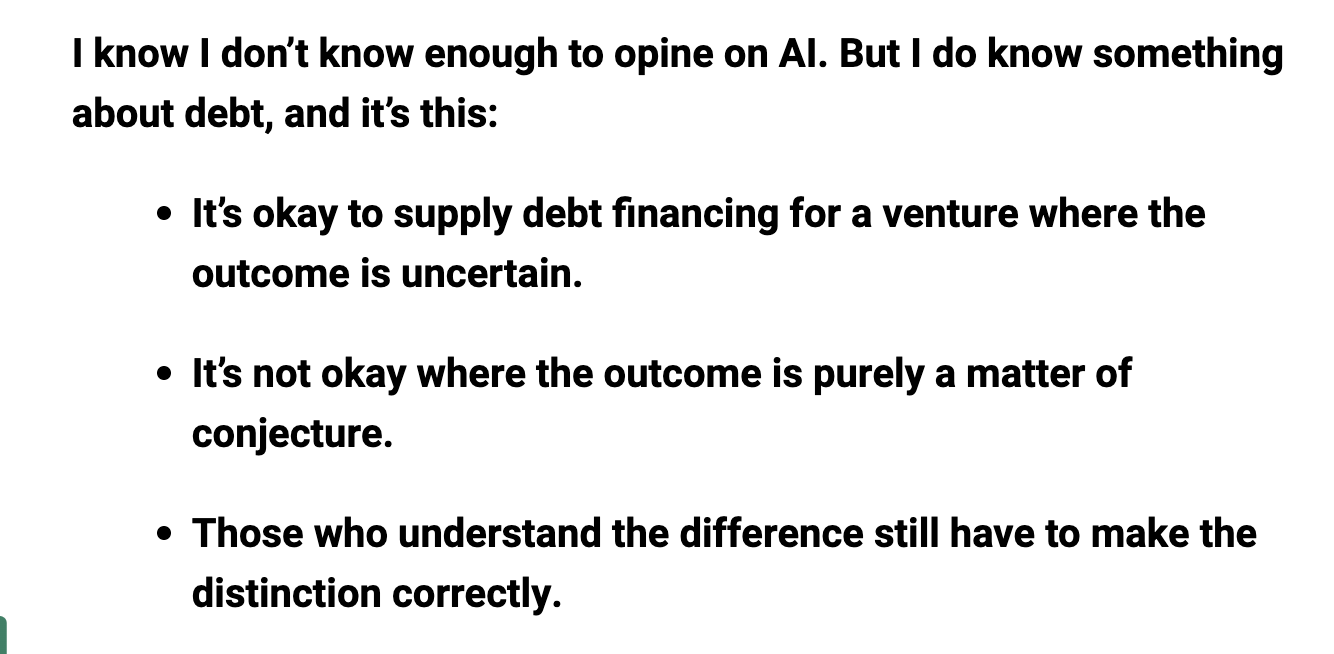

The back half of the memo talks about the risks of how much debt is starting to be used to fund AI capital investment-- which I've covered in the past. I completely agree.

He writes, "The “right” way to play this dynamic is through equity, not debt."