KO

Coca-Cola Co

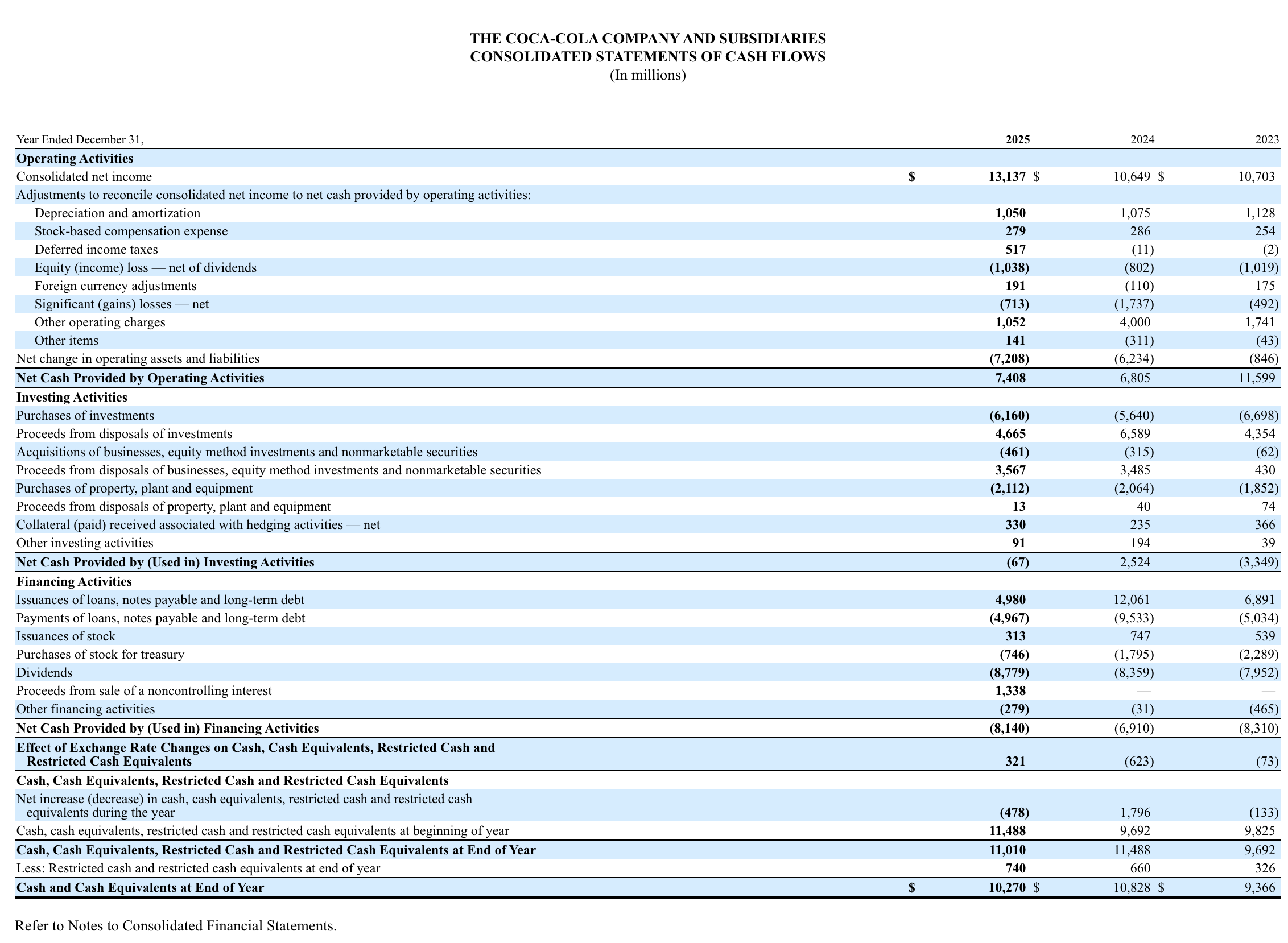

Coke's Cash Flow Statement

Understand The Cash Flow StatementCoke's Cash Flow statement tells a pretty interesting story.

Let's tell the good, the bad and the ugly by green, yellow, and red flags I noticed

🟢 Green Flags

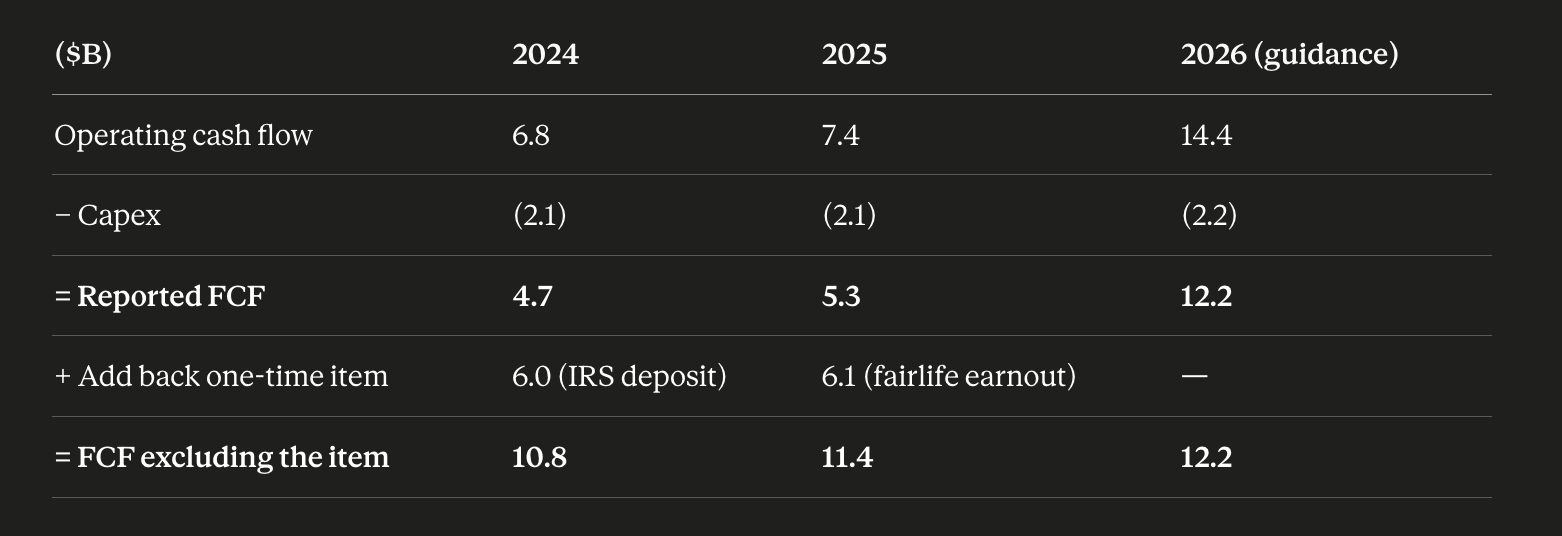

The underlying cash engine grew straight through two ugly reported years.

Strip the one-time items and FCF went ~$9.8B → $10.8B → $11.4B, guided to ~$12.2B in 2026. The business never actually stumbled on cash generation; the statement just looked like it did. That's the single most important green: the distortions were optical, not operational.

(When Coke bought the rest of fairlife in 2020, it didn't pay a fixed price. It paid ~$980M upfront plus an earnout: a promise to pay the sellers (Select Milk Producers) more, later, based on how fairlife performed over a defined measurement window)

Trivial capital intensity. ~$2.1B capex on $47.9B revenue (~4–5% of sales) is the structural payoff of refranchising. The capex-heavy bottling sits on franchise partners' balance sheets, not Coke's. This is why the company converts net income to free cash flow at such a high rate, and it's durable, not a one-year fluke. This shows how strong Coke's business model is.

🟡 Yellow Flags

Dividend coverage is thin. The $8.8B dividend was not covered by reported FCF in either 2024 or 2025... payout ran above 100% of operating cash flow both years, bridged with cash reserves and financing. On management's adjusted basis it's ~73–75%, near target. Both numbers are true. The reason it's yellow is that there's very little margin for error: normalized FCF (~$11–12B) and the dividend (~$8.8B and growing ~5%/yr) are converging, so the dividend now consumes most of the real free cash flow.

This is the price you pay for being a "Dividend King"

Almost no buyback firepower left in practice. Net repurchases were only ~$0.4B in 2025. Nearly all shareholder return now runs through the dividend, which is the least flexible form - you can pause a buyback in a bad year.. but they won't...cutting a 63-year dividend streak is unthinkable. So the cash flow statement has lost a shock absorber.

Re-franchising will remove revenue in the future. The asset-light move that makes the cash flow statement look good also shrinks the top line.

An example of this is the pending CCBA bottler sale. When Coke sells it's ownership interest it will remove almost 4% revenue in 2026. (CCBA is the largest Coke bottler on the African contient - Coke currently owns 66% of it). This is not necessarily a problem, but it means that you can't read revenue and cash flow trends off the same baseline.

🔴 Red Flags

The risk hiding in a footnote. Coke is fighting the IRS over how it shifted profits to low-tax countries from 2007–2009. It lost in Tax Court and is appealing, with a ruling due in late 2026 or 2027. The catch: the court case is "only" ~$6B, but if Coke loses and the IRS's method gets applied to every year since, Coke's own estimate of the exposure runs to $16–18 billion. Against that, it has reserved just ~$493 million... because it believes it'll win. That's a 30+ multiple between what's at stake and what's set aside, and almost none of it shows up in the actual financials. A loss would cost more than the IRS deposit and the fairlife earnout combined. The statements are priced for a win; the downside lives in the fine print. (I'm not a lawyer, but 3 of the 4 "Big Four" accounting firms have filed briefs supporting Coke's accounting, so I do think they'll win)

Capital allocation judgment is genuinely mixed. The flip side of the fairlife win is the $960M BODYARMOR trademark impairment in Q4 2025... a write-down on a $5.6B 2021 acquisition. It's non-cash (so it doesn't hit the cash flow statement directly), but it's an admission that real cash was overpaid for a brand that underdelivered. One brilliant deal and one clear miss in the same era means the M&A track record shouldn't be assumed to be uniformly good, and acquisitions are where large discretionary cash outflows live.

Conclusion

This is a really good cash flow statement, and it makes sense why it's a Buffett-owned company.

I'm not too worried about the IRS lawsuit, and hopefully the new CEO doesn't make the same poor capital allocation decisions like Body Armor, but instead focuses on accretive acquisitions such as Fairlife

Sentiment: Slightly Bullish