GO

Grocery Outlet Holding Corp

This discount grocer uses independent buying to cut prices 70%

Grocery Outlet plays in the "extreme value" retail. They have 533 stores throughout the US.

From their annual report:

So they use flexible by buying name-brand consumables "opportunistically" through a centralized purchasing team to acquire product at significant discount.

They created a franchise model where independent operators. They share 50% of store-level gross profits with $GO.

So, in essence, their business model relies on their "WOW!" deals to create a treasure hunt shopping experience. Pretty innovative.

Purchasing is mentioned a ton in the annual report. This makes sense, but isn't the first thing I'd think about as a newbie to this space

Note: this is part of my on-going research as I'm looking to buy equity in a local bodega in the town I live

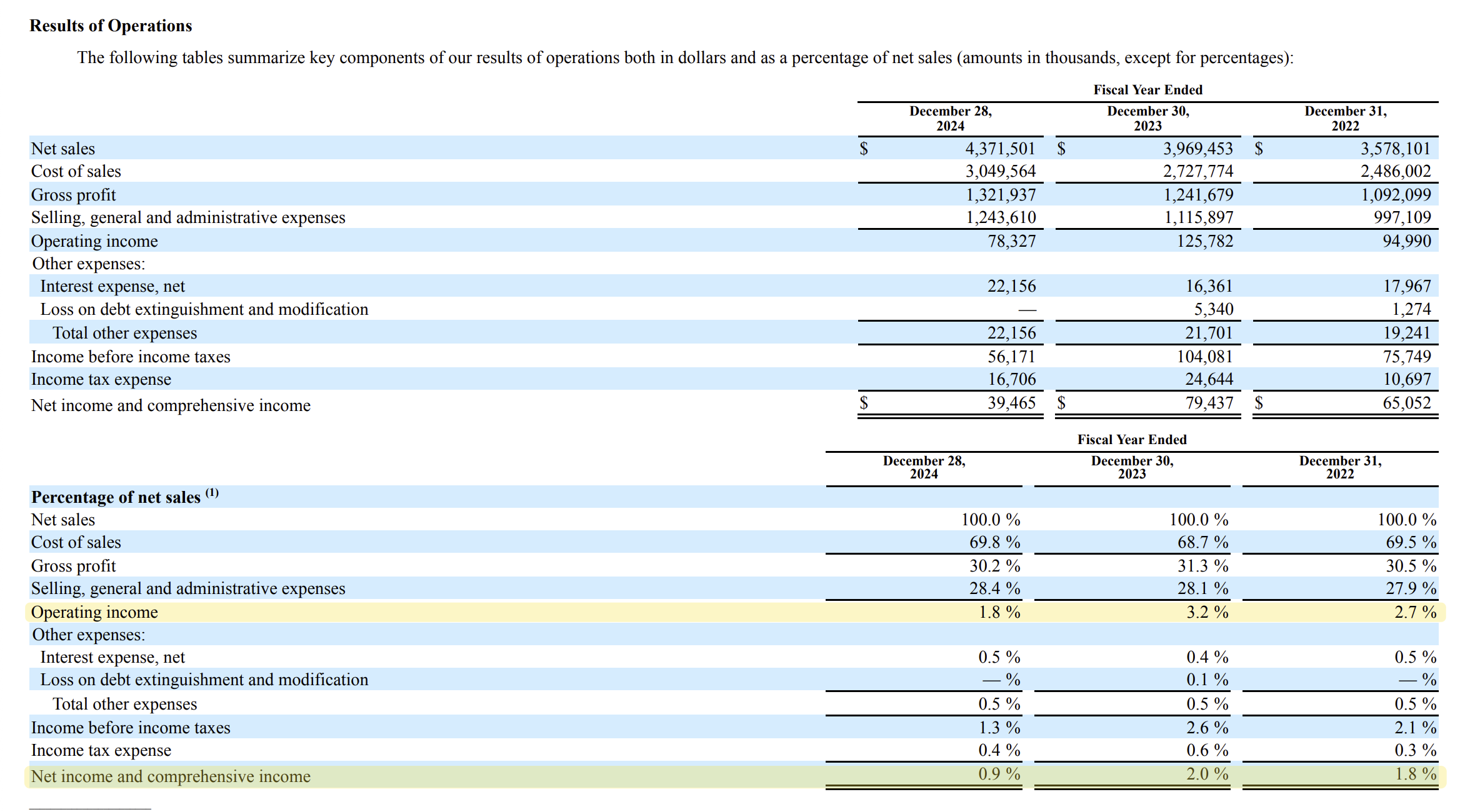

Revenue growth: very steady, compounding at 9.5% 5-year, 8.5% 1-year. Mostly due to adding new stores (opened 67 in 2024 alone). Minor growth due to "comparable store" growth of 2.7% in 2024, driven by a 4.2% increase in the number of transactions partially offset by a 1.4% decrease in average transaction size.

(good for me to note how they grew revenue, same store sales will be a KPI for our Bodega... but that may only be a one-trick pony once it is optimized).

Gross profit sits around 30%.

Operating and Net income are RAZOR thin at 1.8% and .9% of sales (damn). This is a steep decrease from 2023, due to new store openings.

They acquired "United Grocery Outlet" in 2024, which is why they added so many stores in 2024.

My key takeaways:

Purchasing matters immensely

Expect a 30-35% gross margin

Need to understand 'deli/coffee/bodega' margins over just groceries

Inventory turns are hyper important for retailers

Inventory turnover = COGS/Avg Inventory

10-14x is good

Rent as % of sales should be <6%

Seasonality: expect 2-3x higher sales during peak season

Labor as % of sales 18-22% of sales