ASML

ASML Holding NV

Understand The Income Statement

Understand The Income StatementASML – Value Investor Income Statement Analysis (2014–2024)

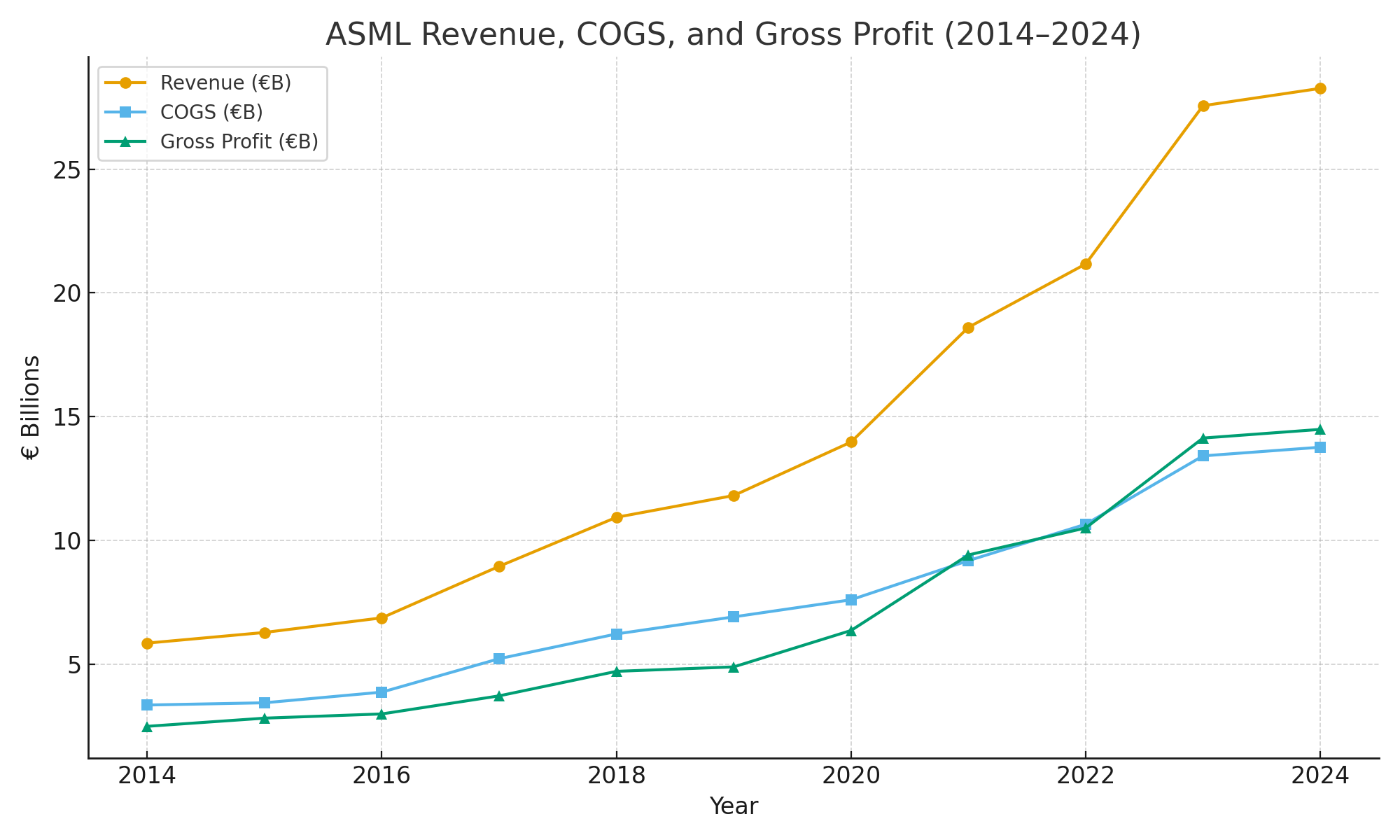

1. Revenue:

2014: €5.9B → 2024: €28.3B (CAGR ~19%).

Inflection points:

2017–2019: EUV ramp (TSMC, Samsung, Intel first adopters).

2020–2021: AI/data center buildout.

2023–2024: slowdown from memory downturn & China export bans.

Installed base services grew to €6.5B (~23% of total, recurring).

Value lens: Fisher → sustainable growth anchored in technological innovation and necessity.

2. Cost of Goods Sold (COGS)

2014: €3.4B → 2024: €13.8B (CAGR ~15%).

Slower growth than revenue → margin expansion.

Drivers: EUV initially expensive but supplier integration (Zeiss, Trumpf, Cymer) improved efficiency.

Value lens: Buffett → scalable cost base proves moat strength.

3. Gross Profit

2014: €2.5B → 2024: €14.5B (CAGR ~24%).

Service & upgrade contracts carry >55% gross margins.

EUV shifted from loss-making to profit driver after 2018.

Value lens: Munger’s “Lollapalooza” → monopoly + pricing power + scale → exponential compounding.

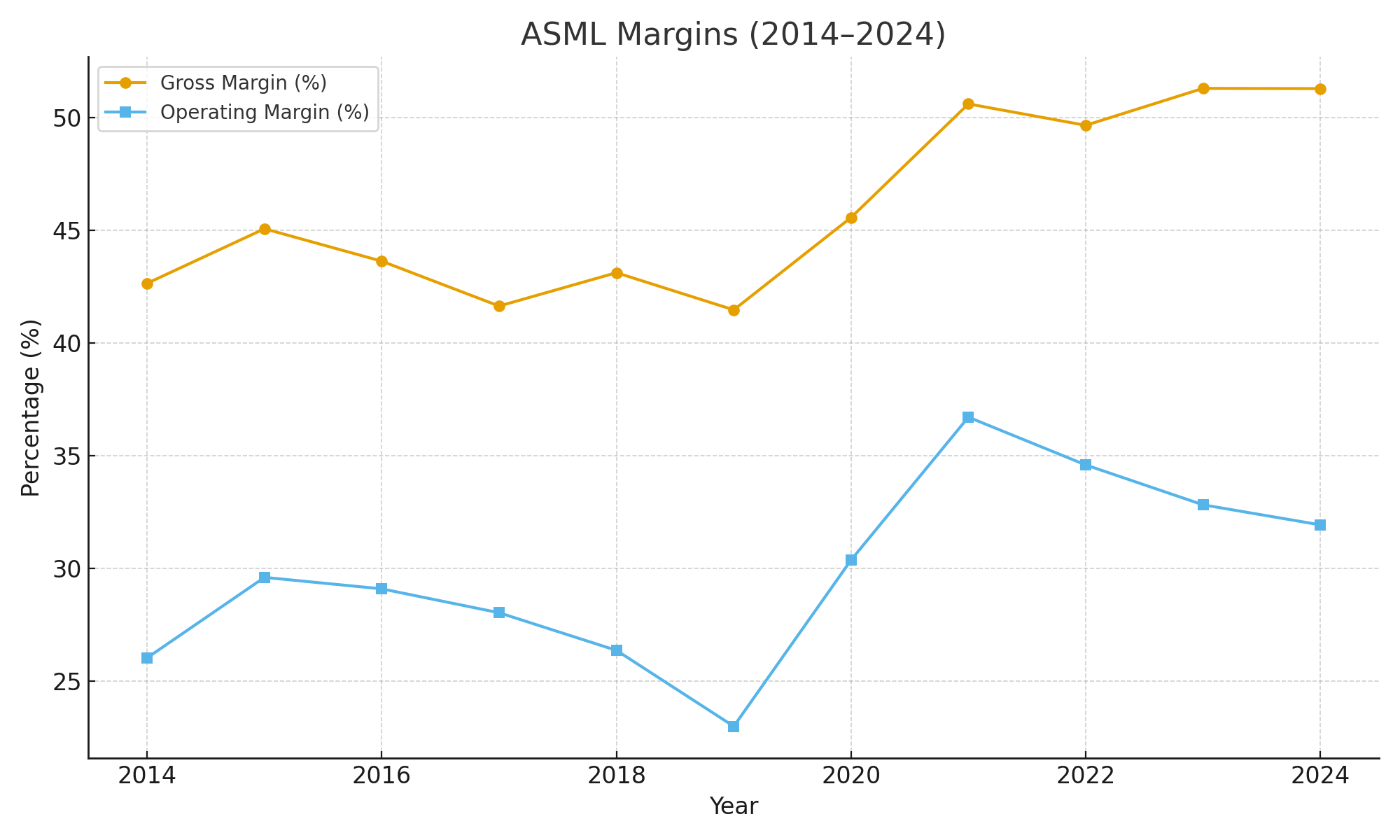

4. Gross Profit Margin

2014–2018: 41–45%.

Post-2020: stable at 50–52%.

Lift driven by EUV maturity & high-margin services.

Value lens: Margin step-up = evidence of durable moat (Buffett: “economics that endure”).

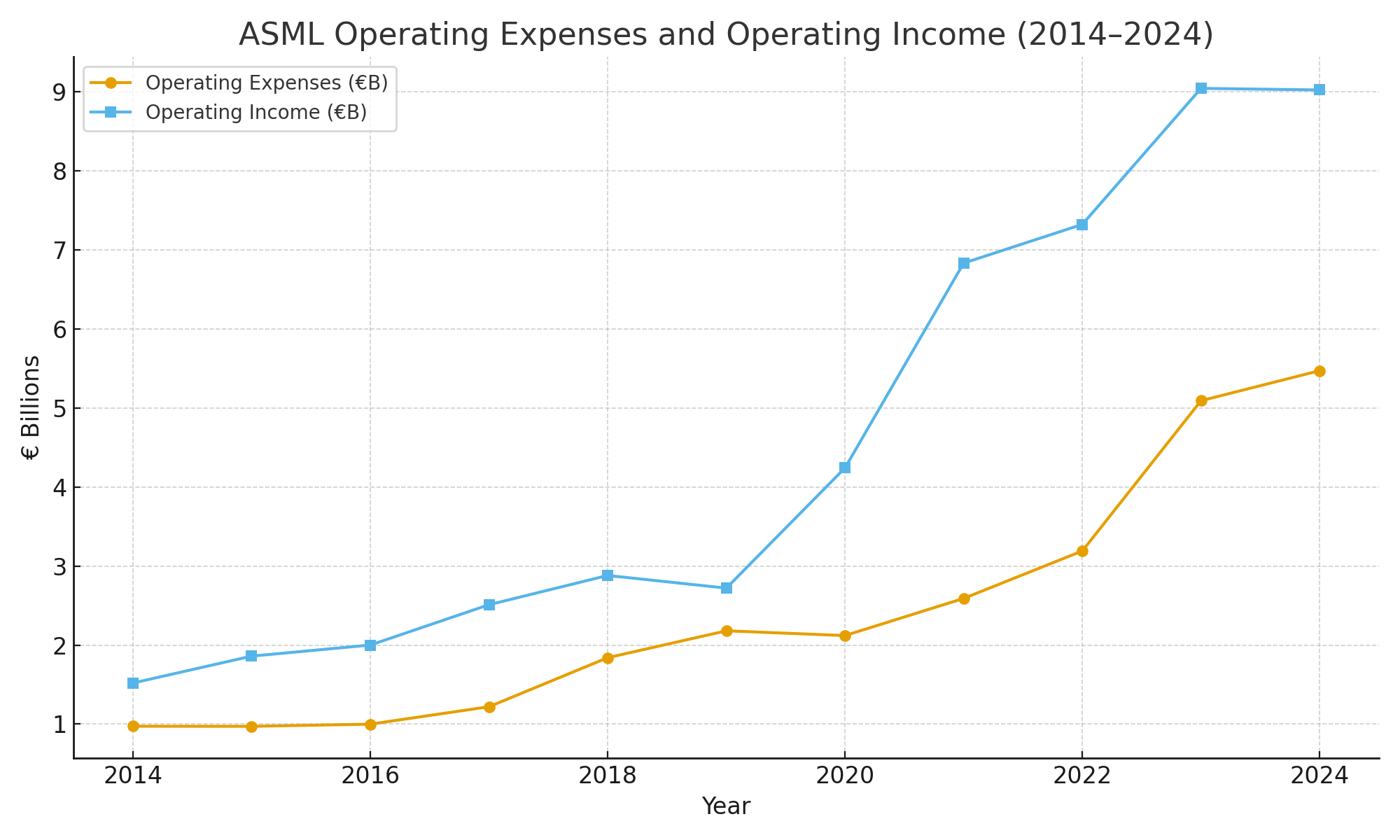

5. Operating Expenses

2014: €1.0B → 2024: €5.5B (CAGR ~20%).

R&D ~€4.3B (15% of sales), SG&A ~€1.1B (4–5%).

Focus: High-NA EUV, holistic lithography, computational & AI-enabled design tools.

Value lens: Fisher → high, consistent R&D is moat-building, not wasteful.

6. Operating Income

2014: €1.5B → 2024: €9.0B (CAGR ~19%).

Dip in 2019 from EUV ramp, then strong acceleration post-2020.

Value lens: Greenblatt’s Magic Formula → high ROC with growth → top-tier compounder.

7. Operating Margin

2014–2016: 26–29%.

2019: fell to 23% (EUV ramp costs).

2021: peaked at 37% (AI supercycle).

2024: ~32%.

Value lens: Munger → temporary margin pain was moat investment, not structural weakness.

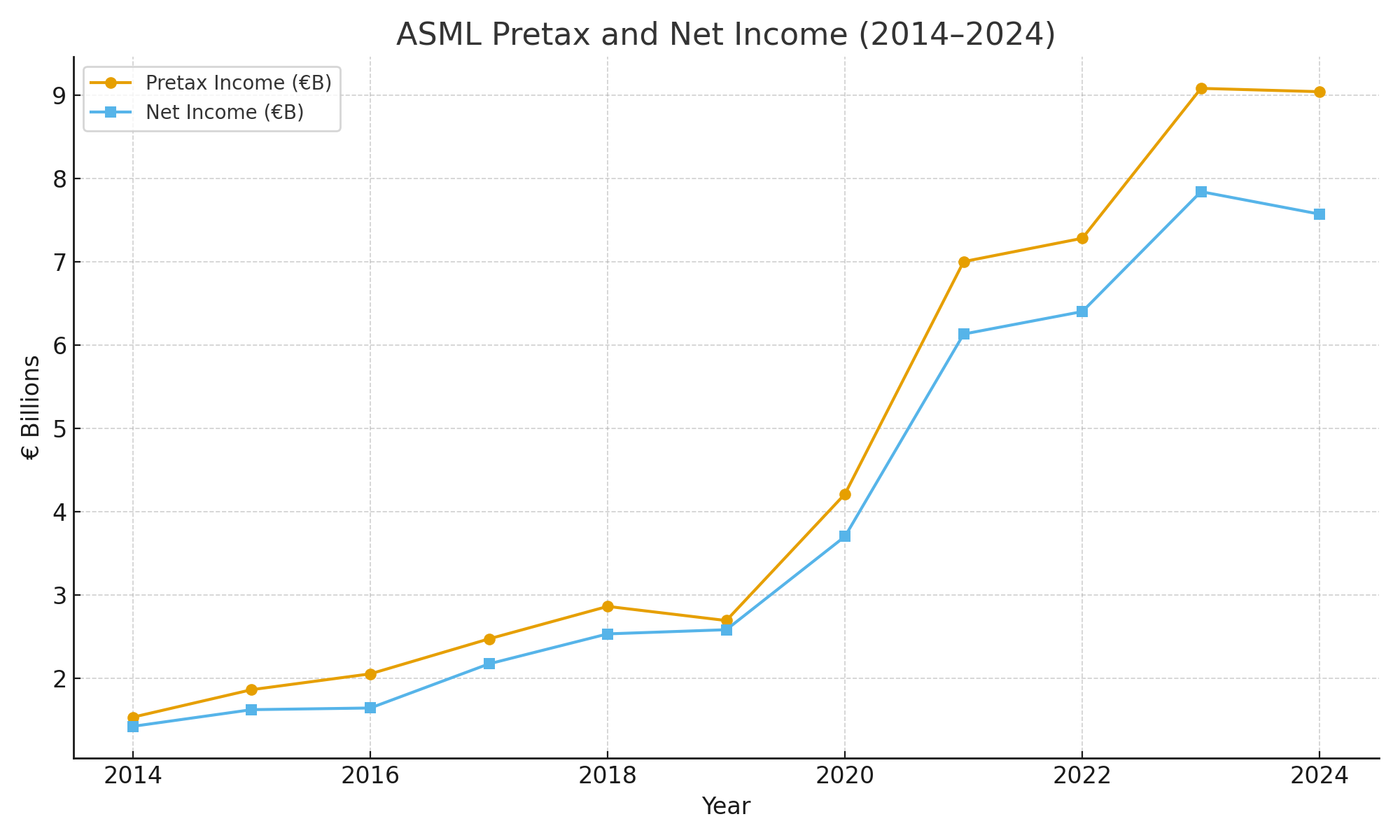

8. Total Other Income

Small (~€0.3–0.4B).

Net interest + small equity stakes.

Value lens: Buffett → true earnings come from operations, not financial tricks.

9. Pretax Income

2014: €1.5B → 2024: €9.0B (CAGR ~18%).

Clean alignment with operating income (no distortions).

Value lens: Buffett → pretax income is the cleanest check of business quality.

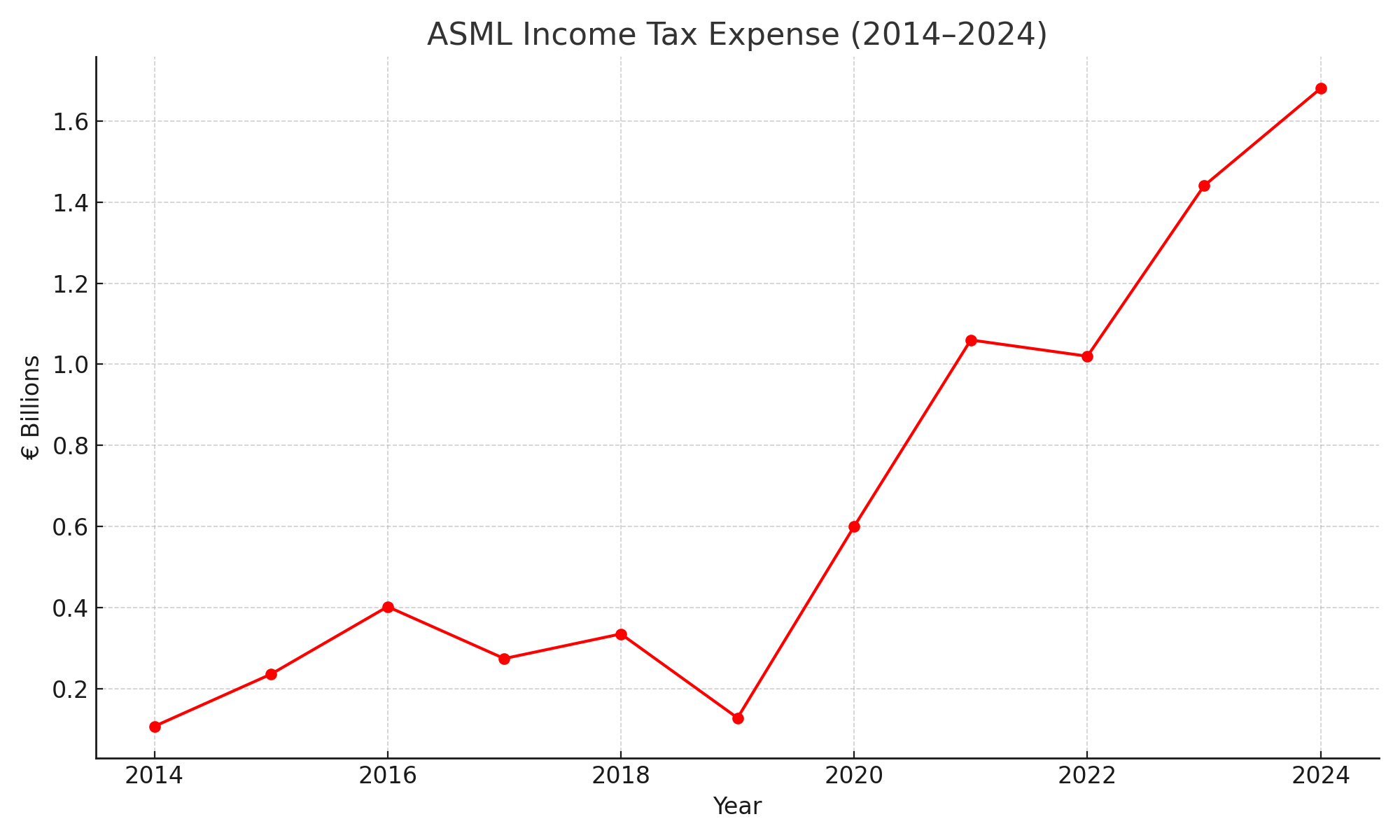

10. Income Tax Expense

2014: €0.1B → 2024: €1.7B.

Effective tax rate ~16–19%, fairly stable.

Netherlands tax incentives & R&D credits help.

Value lens: Klarman → predictable tax = stable compounding, reduces downside risk.

11. Net Income

2014: €1.4B → 2024: €7.6B (CAGR ~18%).

Spike in 2021 from AI/EUV demand, stable at high levels in 2023–24.

Value lens: Lynch → earnings drive stock prices; consistency proves durability.

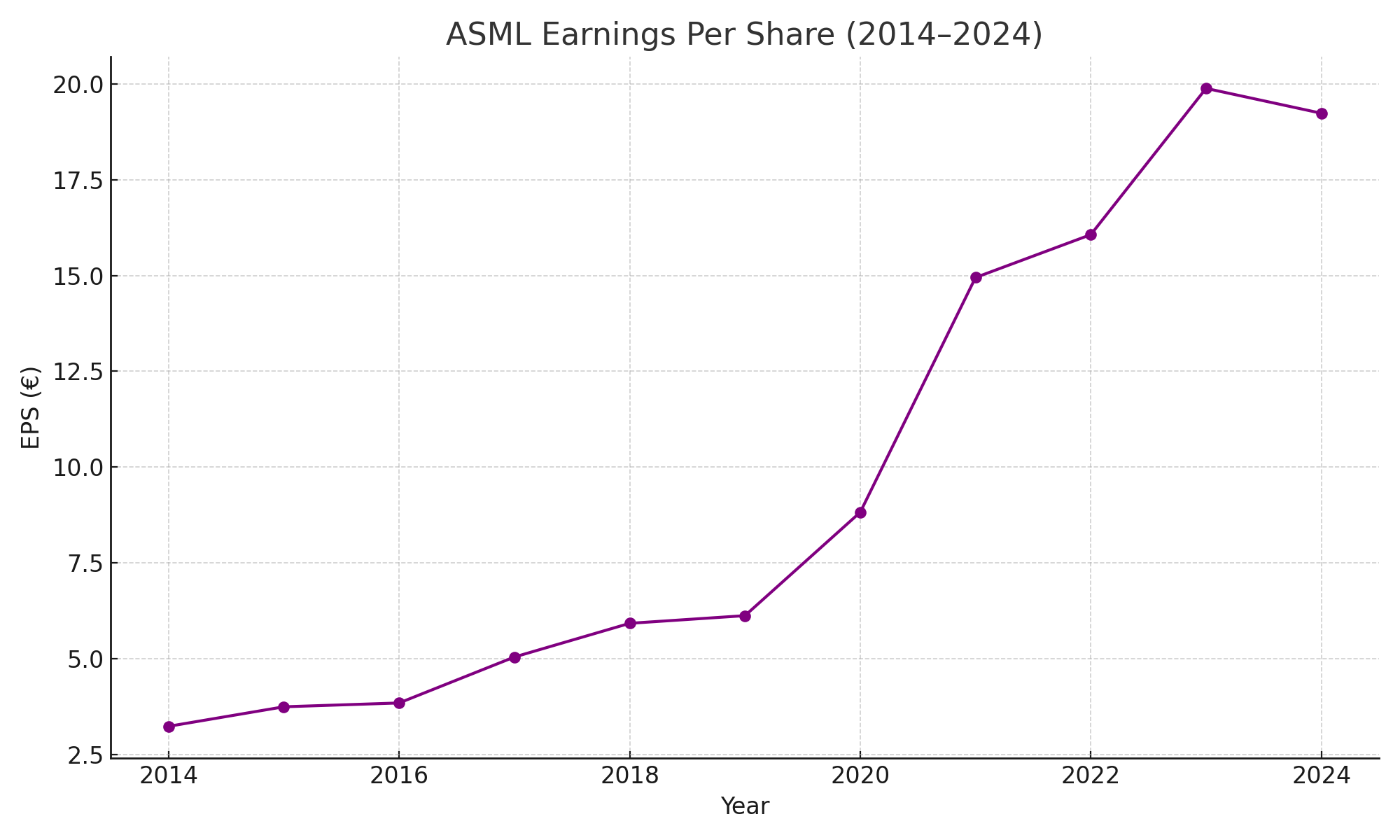

12. Earnings Per Share (EPS)

2014: €3.23 → 2024: €19.24 (CAGR ~21%).

Boosted by share buybacks and strong dividends (€6.40/share in 2024).

Value lens: Buffett → EPS compounding = true “owner’s earnings” growth.

Different people perspectives like I researched/imagine them from books, interviews, personal knowledge and articles:

Buffett/Munger: ASML = wonderful business, monopoly-like economics, recurring revenues.

Fisher: Relentless innovation and customer trust ensure long runway.

Greenblatt: High ROC and profit growth rank ASML at the very top.

Klarman/Marks: Margin of safety thin at P/E ~35–40; best entry is during downturns.

Lynch: Fast grower that is also unusually durable.

Conclusion:

ASML is the ultimate compounding machine: over 15 years of >15% EPS growth, structural margin step-up, and a monopoly-like moat. The only limitation is valuation — expensive at current multiples. Strategy: hold long-term for compounding, and buy aggressively during semiconductor downturns or geopolitical shocks when market offers a discount from my perspective.

Please let me know if I’ve missed or overlooked anything, made a mistake, or if you have any questions or suggestions for improving the analysis!