NOK

Nokia Oyj

Is this a sheep in wolfs clothing or does Nokia have some fight left in it?

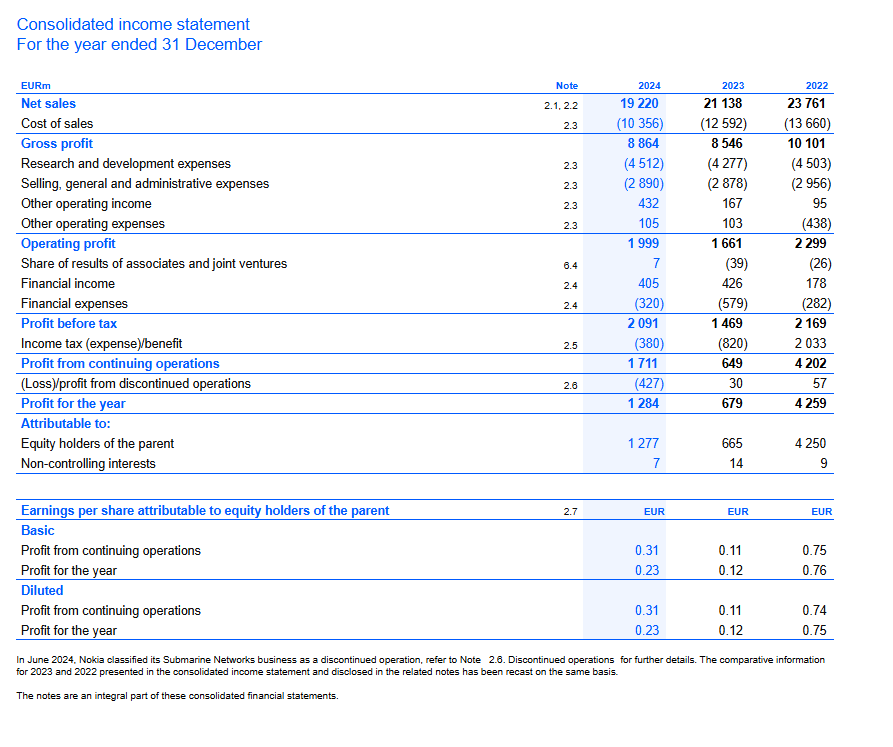

Understand The Income StatementSo, Nokia Oyj is not a US firm but it is listed on the US stock exchange so to get these documents you need to look at the form 20-K.

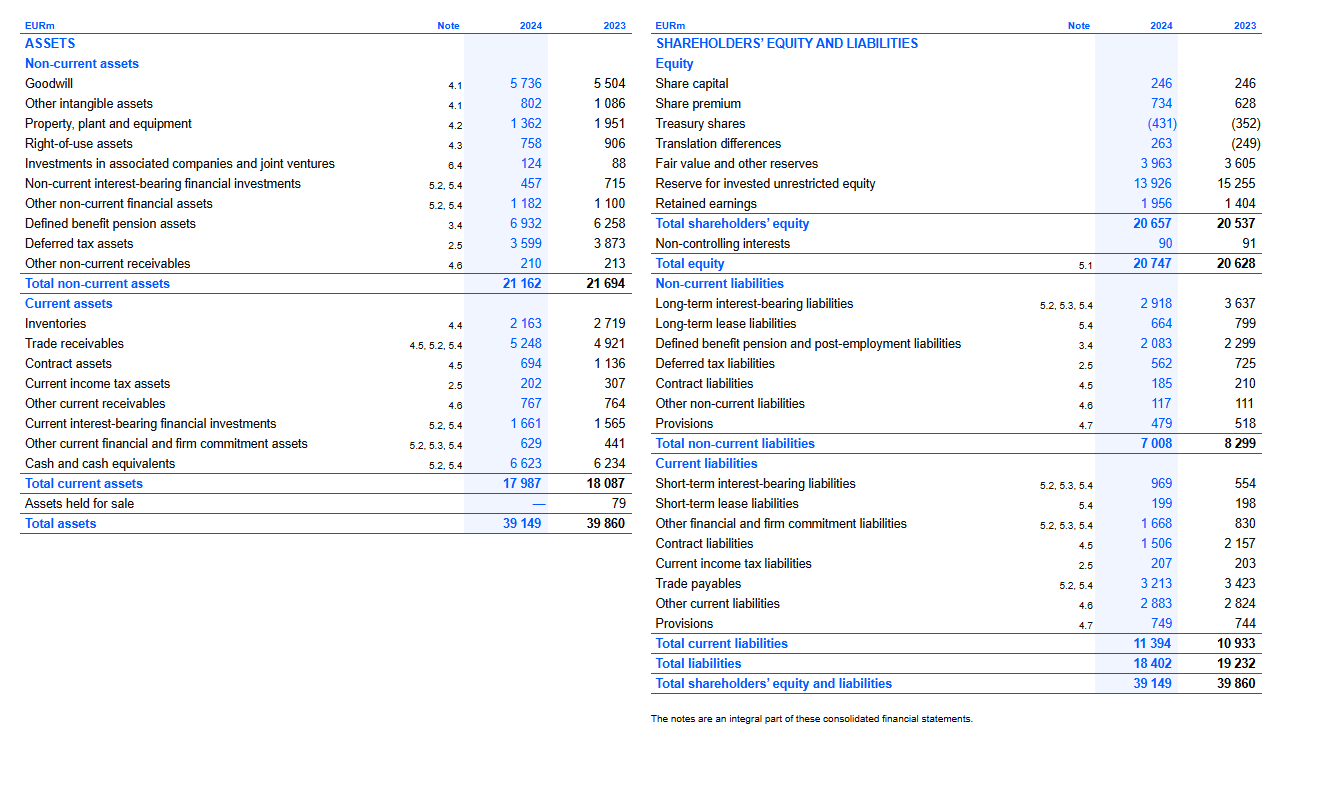

The biggest thing that jumps out at me is there is not a sizable obscure asset called Goodwill jumping out at me.

However, if you look at their asset breakdowns

Boom 5 billion Euros in good will. How is Nokia defining good will?

Accounting policies

Intangible assets acquired separately are measured on

initial recognition at cost. Internally generated intangibles,

except for development costs that may be capitalized, are

expensed as incurred. Development costs are capitalized

only if Nokia has the technical feasibility to complete the

asset; has an ability and intention to use or sell the asset;

can demonstrate that the asset will generate future

economic benefits; has resources available to complete

the asset; and has the ability to measure reliably the

expenditure during development.

The useful life of Nokia’s intangible assets, other than

goodwill, is finite. Following initial recognition, finite

intangible assets are carried at cost less accumulated

amortization and accumulated impairment losses. Intangible

assets are amortized over their useful lives, generally three

years to ten years, using the straight-line method, which is

considered to best reflect the pattern in which the asset’s

future economic benefits are expected to be consumed.

Depending on the nature of the intangible asset, the

amortization charges for continuing operations are included

in cost of sales, research and development expenses or

selling, general and administrative expenses.

Goodwill is allocated to the cash-generating units or groups

of cash-generating units that are expected to benefit from

the synergies of the related business combination and that

reflect the lowest level at which goodwill is monitored for

internal management purposes. A cash-generating unit, as

determined for the purposes of Nokia’s goodwill impairment

testing, is the smallest group of assets generating cash

inflows that are largely independent of the cash inflows

from other assets or groups of assets. The carrying value

of a cash-generating unit includes its share of relevant

corporate assets allocated to it on a reasonable and

consistent basis. When the composition of one or more

groups of cash-generating units to which goodwill has been

allocated is changed, the goodwill is reallocated based on

the relative fair value of the affected groups of cash-

generating units.

Nokia tests the carrying value of goodwill for impairment

annually. In addition, Nokia assesses the recoverability of the

carrying value of goodwill and intangible assets if events

or changes in circumstances indicate that the carrying value

may be impaired. Factors that Nokia considers when it

reviews indications of impairment include, but are not

limited to, underperformance of the asset relative to its

historical or projected future results, significant changes

in the manner of using the asset or the strategy for the

overall business, and significant negative industry or

economic trends.

Nokia conducts its impairment testing by determining the

recoverable amount for an asset, a cash-generating unit or

groups of cash-generating units. The recoverable amount

of an asset, a cash-generating unit or groups of cash-

generating units is the higher of its fair value less costs of

disposal and its value-in-use. The recoverable amount is

compared to the asset’s, cash-generating unit’s or groups

of cash-generating units’ carrying value. If the recoverable

amount for the asset, cash-generating unit or groups of

cash-generating units is less than its carrying value, the

asset is considered impaired and is written down to its

recoverable amount. Impairment losses are presented

in cost of sales, research and development expenses or

selling, general and administrative expenses, except for

impairment losses on goodwill, which are presented in

other operating expenses

So, lets summarize that

Synergies: The expected cost savings or revenue boosts created by integrating the new company into Nokia's existing Network Infrastructure or Mobile Networks.

Assembled Workforce: The value of having a pre-existing team of highly skilled engineers and researchers (e.g., from the Alcatel-Lucent acquisition or the recent Infinera deal).

Future Technology & R&D: The potential for future innovations that are not yet patented or documented as specific "intangible assets" at the time of purchase.

Market Position: The strategic "foothold" or brand reputation gained in a specific geography or technical niche.

Interesting stuff so far Nokia does not have the software arm Broadcom does.