BRK.A

Berkshire Hathaway Inc

Berkshire's Growth Strategy (by Grove!)

What's Their Growth Strategy?If you check out my Past Growth article, I updated it after further research.

The gist of it is that, to value Berkshire, Buffett recommends breaking Berkshire into 5 "Groves", a play on seeing 'the forest from the trees'.

These 5 groves are:

Non-Insurance Operating Businesses (BNSF, Lubrizol, Netjets, etc)

Equity Investments (Apple, Coca-Cola, AMEX, etc)

Share-Controlled Businesses (Pilot Flying J, Occidental Petroleum, etc).. companies that Berkshire has a significant portion in, but doesn't wholly own

Cash equivalents and US Treasury Bills

Insurance Operations (GEICO, General Re, etc)

So that's how I'll be doing the rest of my analysis!

Non-insurance Operating Businesses

Berkshire subsidiaries generally reinvest a large portion of their earnings to expand and improve their businesses. For example, Berkshire Hathaway Energy has been plowing earnings into expanding its utility infrastructure and renewable power capacity – Buffett noted BHE’s annual earnings grew from just $122 million in 2000 to $3.4 billion in 2020 through continuous reinvestment

For growth expectations: given their large scale, these businesses are unlikely to repeat the explosive growth of past decades, BUT we can expect steady, moderate growth.

I'm going to assign a growth rate of ~5%/yr for this sector. Of course, the wildcard is a massive acquisition given their extreme cash pile.

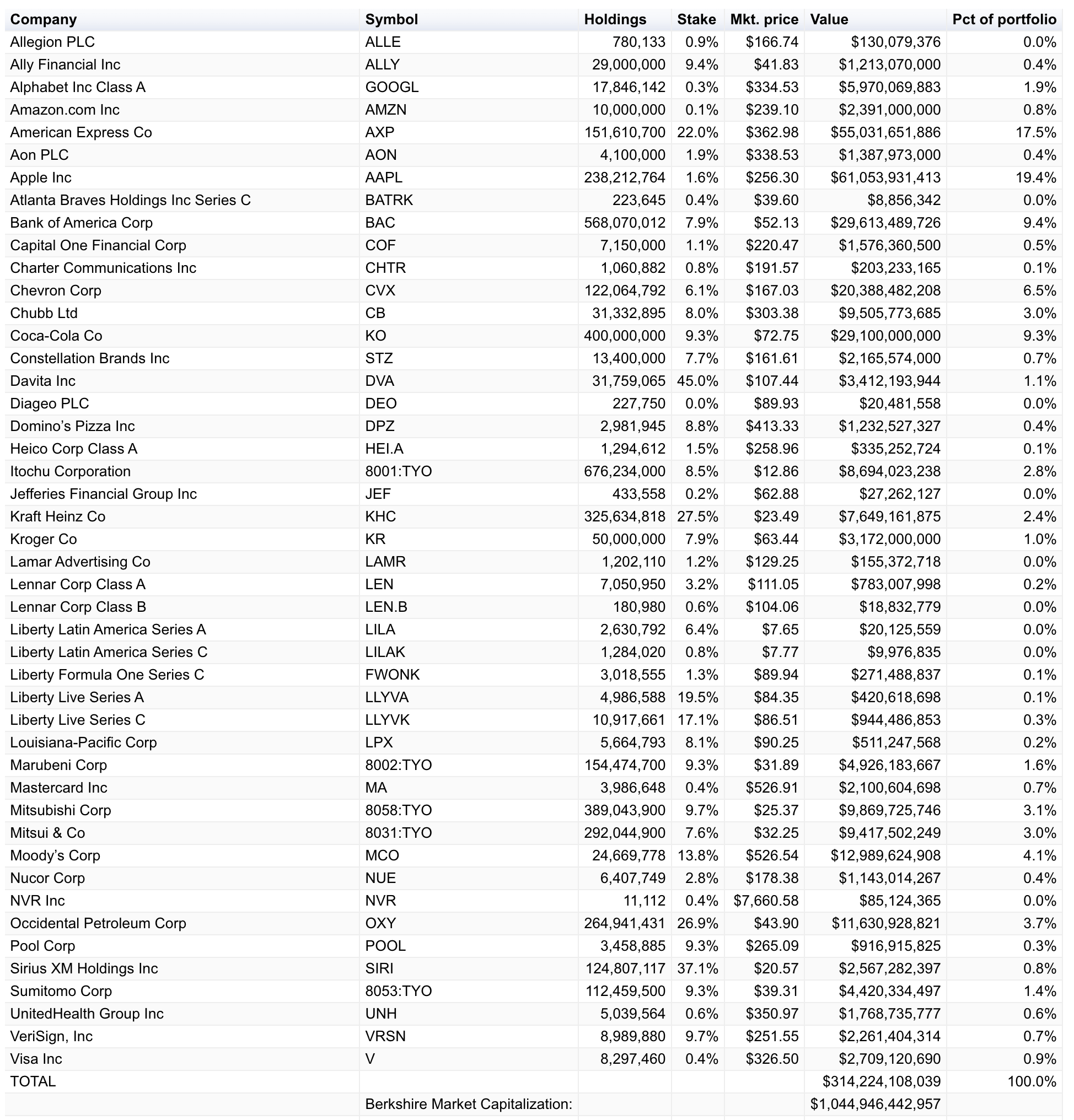

Equity Investment Portfolio

This is Berkshire's current equity portfolio:

It would be insane to study all of these businesses and assume a growth rate. Instead, I'm going to assume they'll grow at 10%/yr. My reason for this: stocks have historically grown at 8%/yr, and with dividends, buybacks, and just good ole fashion Buffett-premium, I'm going to assume they generate a little bit of alpha.

It's important to note, Buffett has repeatedly said that he has built Berkshire to perform decently in bull markets, and fantastically in bear markets. This portfolio is an all-weather portfolio. If the next 10-years are tough, I expect Berkshire to do even better.

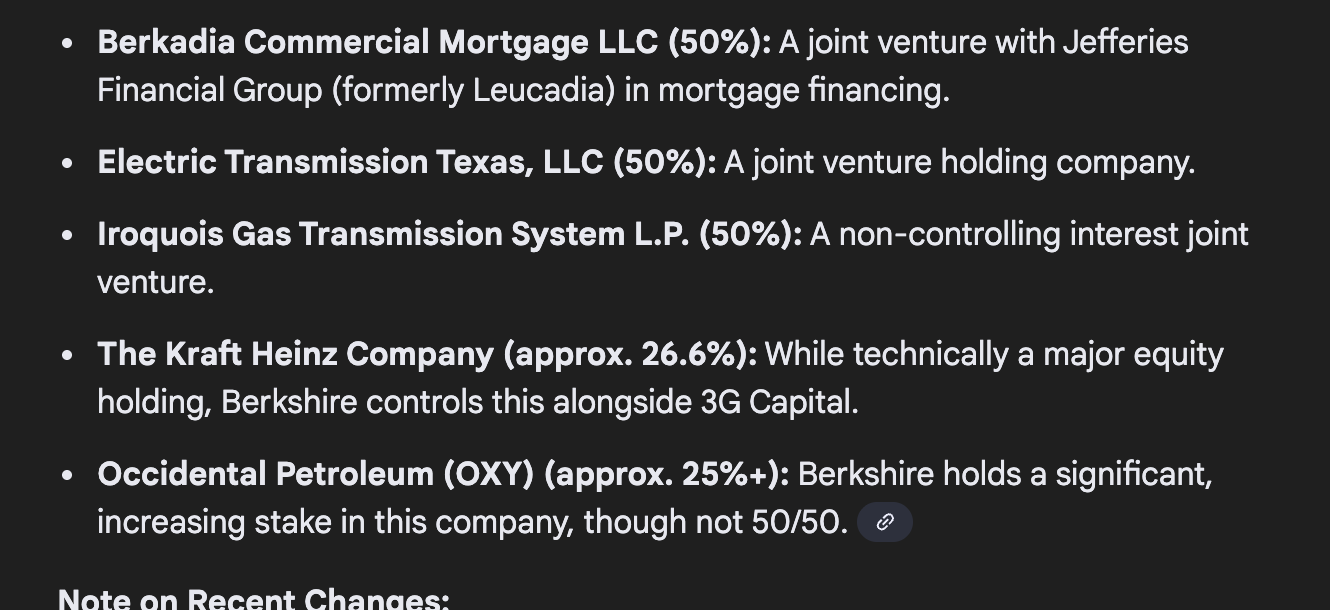

Shared-Control Businesses

This is the smallest "grove". The holdings include:

These seem even more defensive than their equity portfolio, so I'm going to assume a 4% growth rate for the next 10 years on this grove.

Cash, T-bills and Cash Equivalents

This is the segment that doesn't grow. It's Berkshire's dry-powder to make a new investment! I'm going to assume a 3% growth rate for this grove.

Insurance Operations

This includes all of Berkshire’s insurance and reinsurance companies, whose primary value comes in two ways:

ongoing underwriting profits (if any) from selling policies, and

the enormous float those policies generate. Berkshire’s insurance group – led by units like GEICO (auto insurance), General Re, Berkshire Hathaway Reinsurance, National Indemnity, and Alleghany (acquired in 2022)

Berkshire's insurance is unique for its scale and underwriting discipline.

Buffett’s approach to insurance is profitable growth, not growth at any cost. He famously said “all insurers give the message of disciplined underwriting lip service; at Berkshire it is a religion, Old Testament style”

Indeed, float has compounded over decades (for example, from ~$65B in 2007 to $122.7B in 2018, and now $170B+). However, Buffett has cautioned that as the float base gets larger, its growth rate will likely slow. He wrote in 2020 that substantial growth in float might be harder to achieve, but importantly he expects Berkshire’s existing float to be “very sticky”.. it won’t run off quickly, even if the insurance business isn’t growing fast, because Berkshire’s policies (like auto insurance renewals or long-dated reinsurance liabilities) keep the float in place.

The strategy can be summed up as: grow the float steadily if profitable, and use the float to invest in higher-yield assets (stocks, bonds, businesses) for Berkshire’s benefit.

I'll assume a 2% growth for Insurance. Berkshire’s “secret sauce” has been exactly that: using low-cost float to fuel outsized investment returns

WOO THAT WAS TOUGH I'M GOING FOR A RUN