FIG

Figma Inc

Rapid Revenue Growth, Driven By Adobe’s Surrender?

In the light of Figma’s languishing stock price, I’ve decided to take a swing at the numbers we do have for it, few as they may be…

The short answer is yes, they are growing!

From what I gather, they are one of the most pervasive enterprise-grade, design-oriented, software-as-a-service companies of the decade. Their main competitors still being Adobe’s new Firefly AI features, and the Australian software firm Canva.

Onto the numbers; Figma grew revenues 48.36% between 2023-2024, and is projected to grow 39.54% (with just Q4 2025 left, reporting on February 18th). These are impressive numbers, and their heightened price multiples reflect this.

They have over 1,250 customers paying $100K+ in subscription revenue and are seeing rapid growth (+13% Q3 2025) in that cohort. They’ve also got nearly 13,000 customers paying more than $10K ARR. Finally, along all their customers, they have over 540,000 paying teams as of Q2.

While the sales growth story is compelling, and their customer base is a great strength, they remain unprofitable, though this could be due to their stock-based compensation and IPO fees they’ve had to get past. An unprofitable business like this is not necessarily a bad business after all.

As a side note, in December 2023, Adobe was blocked by the FTC from acquiring them. An interesting caveat that may have been a temporary tailwind, is that Adobe XD, the product that once competed with Figma, has since been deprecated by Adobe, to instead focus on Firefly AI features in other software.

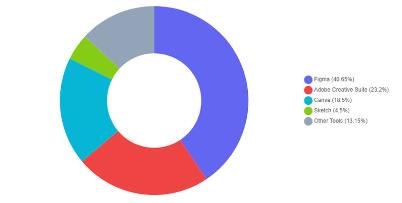

This winding down of Adobe XD was mostly caused by Figma’s competition. As a result, Figma surely captured some of Adobe XD’s ~13.5% market share, Figma still steadily adding to their almost 40%.

https://www.figma.com/blog/figma-adobe-abandon-proposed-merger/