BRK.A

Berkshire Hathaway Inc

BEHOLD! The Glorious Balance Sheet of Berkshire Hathaway

Understand The Balance SheetFrom their 2024 annual report... (2025 will be released later this month, I will update my analysis then)

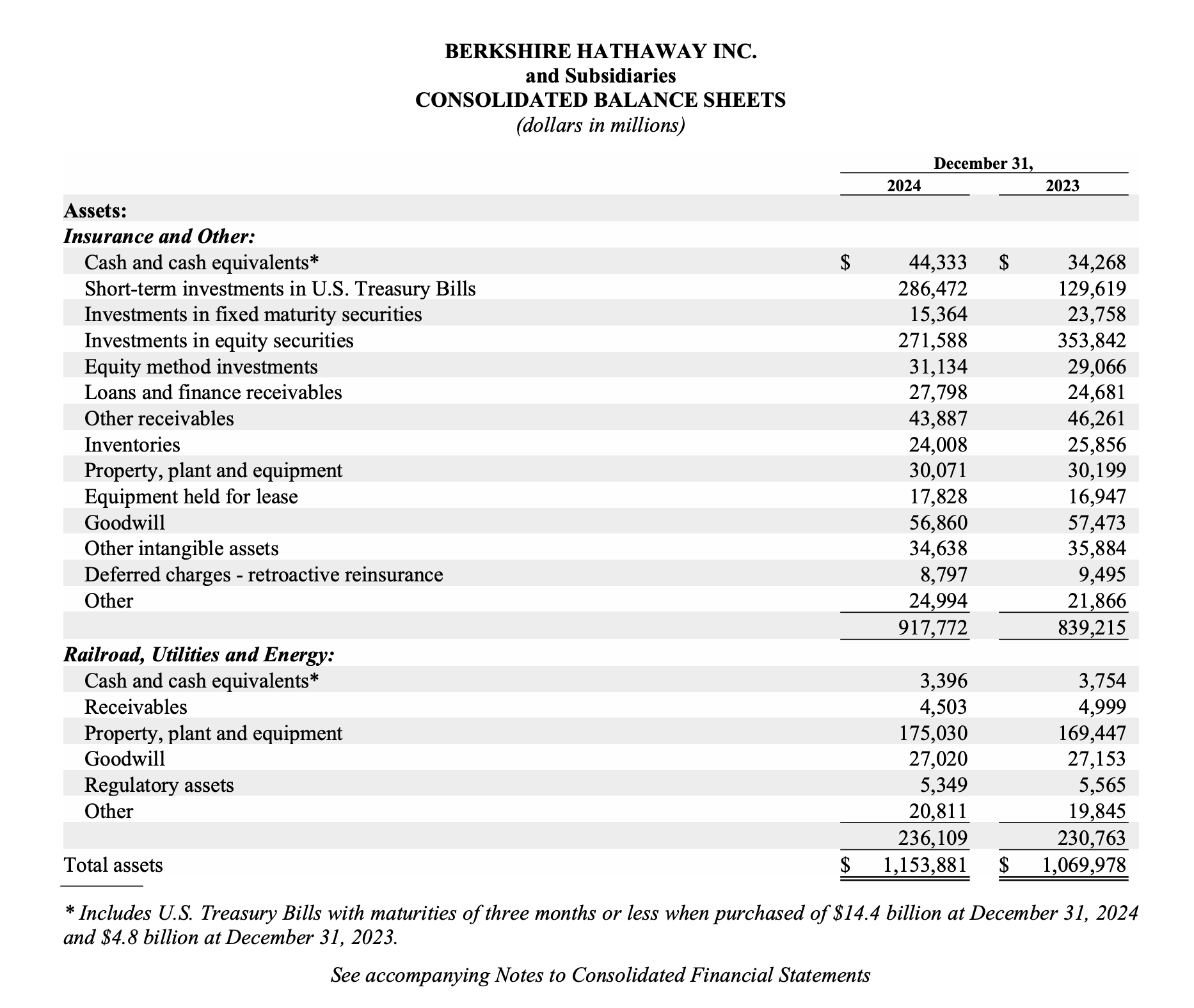

Let's start off with Assets by grove:

Grove 1 (controlled non-insurance businesses): accounting understates them.

PP&E is $175.0B in railroad/utilities/energy alone. These are serious capital structures (railroads... power generation plants...).This is the private operating empire you cannot buy in the public market every day. Very strong indication of a moat.

Why? You can’t wake up and decide to build a second BNSF or a parallel utility grid. Even if you had the money, you don’t have the permits, right-of-way, regulatory approvals, or the decade it would take. That kind of “can’t be replicated” asset base is a moat you can literally touch.

Important accounting note: PP&E is carried at accounting values (cost minus depreciation), not at “what it would sell for” and definitely not at “what it’s worth as a cash-producing franchise.” A regulated utility base and a dominant rail franchise can have earning power far above what the balance sheet suggests. That’s why Buffett pushes you away from GAAP and toward “what the groves are worth.”. This is great, because it means my valuation will be conservative.

Grove 2 (public equities): huge, but smaller than last year.

Equity securities ended 2024 at $271.6B, down from $353.8B.

This is the grove that makes GAAP earnings look insane.

Because these are marked to market, changes here flow through “investment gains/losses” and can overwhelm everything else on the income statement. That’s why a normal P/E on reported net income is basically meaningless for Berkshire, as we saw in the income statement analysis.

Important nuance: I'll still haircut this grove for deferred taxes. A big chunk of Berkshire’s deferred tax liability exists because of unrealized gains here. Since I'm doing a sum-of-the-groves valuation, I don’t get to count the equities at full market value without acknowledging the embedded tax claim.

The key takeaway: this grove is huge, liquid, and volatile. Don’t treat its mark-to-market as ‘earnings.’ Treat it as a pile of businesses with a daily quote.

Grove 3 (equity-method): the quiet pile.

Equity-method investments are $31.1B. This is real value, but it lives in a weird middle ground: not fully controlled (so not consolidated), not freely traded like the public portfolio (so not marked the same way).

This is where “look-through” thinking matters.

Equity-method stakes often represent ownership in businesses that are throwing off earnings and compounding retained capital, but they don’t show up cleanly in Berkshire’s reported operating earnings the way wholly owned subs do.

It belongs in its own valuation bucket, just like Buffett told us :)

I can't slap Berkshire’s overall multiple on this. I'll value these holdings on their own economics: earning power, growth, and what a rational buyer would pay.

Grove 4 (cash): Berkshire is a fortress.

Berkshire had $44.3B of cash in Insurance/Other, $3.4B in the railroad/utilities bucket, and $286.5B in short-term U.S. Treasury Bills. That is $334.2B of cash + T-bills. There’s also a $12.8B T-bill purchase payable, so net is about $321B.

This is strategic, not lazy. Berkshire carries liquidity like a survivalist with a bunker. Buffett wants a balance sheet that can endure a financial crisis, a mega-cat event, and a broken credit market simultaneously, without selling anything important at the wrong time.

This cash pile increases Berkshire’s “optionality.” When valuations get stupid (either too high or too low), optionality is worth a lot. Cash gives Berkshire the ability to do deals when others can’t, and to be patient when deals are unattractive.

In today’s world, cash is no longer dead weight. With higher rates, this grove is also producing meaningful investment income. Berkshire’s cash is both a shock absorber and a contributor.

Grove 5 (insurance): float gives structural advantage.

Berkshire defines float as net liabilities from insurance contracts that fund investments. Float was about $171B at year-end 2024 (up from $169B).

Buffett notes float has grown from $46B to $171B over two decades and can be costless with intelligent underwriting (and luck). That's insane.

Float is funding that behaves unlike normal debt. Float is money Berkshire holds that technically belongs to policyholders over time. But as long as underwriting is disciplined, Berkshire can invest it, and the “cost” of that money can be very low, sometimes even negative (when underwriting is profitable).

It supercharges the other four groves. This is the hidden engine of Berkshire: the ability to invest not only shareholder equity but also a massive pool of float. That’s why Buffett calls Berkshire “more than the sum of its parts.” The groves don’t just coexist, they finance each other.

The risk is always reserve accuracy and catastrophe exposure. Insurance looks easy when it’s working. The real test is whether reserves are adequate and whether rare events are survivable. Berkshire’s whole setup (fortress cash + conservative culture + scale) is built around passing that test. The California Wildfires show the strength of Berkshire's underwriting capabilities.

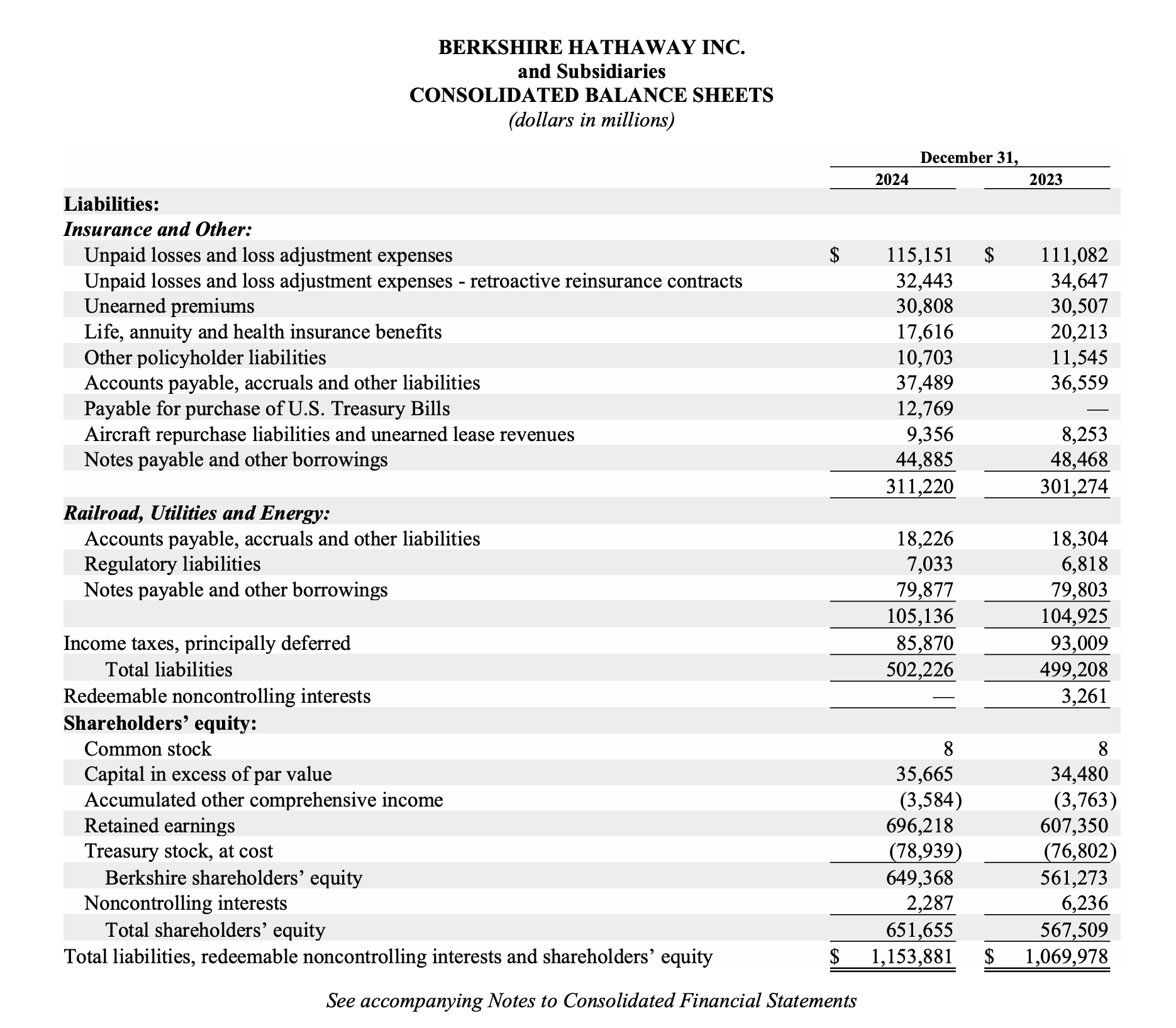

Turning to liabilities, there are seriously no red flags for me. It's beautiful.

When you look at Berkshire through the five groves, the balance sheet stops being a list of line items and becomes a map of how Buffett compounds capital:

a private operating empire (understated by accounting),

a massive public portfolio (priced daily),

a quiet pile of “in-between” ownership stakes,

a fortress cash position that creates optionality,

and an insurance engine that finances the whole machine.

That’s the forest.

Sentiment: Super Bullish