General

Kaspi.kz - Kazakh Super app at a floor valuation (10%+ CAGR)

A quick pitch on Kaspi.kz

My thesis on Kaspi.kz is that the stock now trades at a level where if their main growth strategy failed, you can still make a comfortable 10% return on investment. This gives you a nice floor valuation to work off of, which I detail below. Secondly, I also believe that it is quite probable that company succeeds in their mission to expand over the long term, if not initially.

This makes it an asymmetric bet.

I’ll skip a long business description (others have done that well) and link to a few articles down below.

Kaspi.kz is Kazakhstan’s super app. Payments network, Marketplace, e-grocery, even a get your driver’s license service. Think of it as a blend of PayPal, Shopify, and a digital bank, but built for an emerging market where financial infrastructure was still wide open. Its ecosystem connects consumers, merchants, and lenders in one integrated app with the first mover advantage, making it extremely difficult to compete with.

It trades at a ridiculously low valuation because of location, geopolitics, and most importantly low confidence in the company’s plan to expand operations beyond Kazakhstan to the unpenetrated market of Türkiye. This would massively expand the total addressable market from Kazakh’s already saturated population of 20 million to Türkiye’s 85 million.

Kaspi began this expansion by purchasing a controlling interest in Hepsiburada, a e-commerce marketplace in Türkiye.

(All figures in USD)

Valuation today:

P/E is 7.3

EV/EBIT is 3.58

Kaspi.kz is the 18th cheapest stock on the NASDAQ (by EV/EBIT)

Kaspi has put roughly $1.5bn into the Türkiye expansion so far. About $1.2bn of which is for the Hepsiburada purchase plus roughly $0.3bn in cash use, interest and other spending. If Türkiye truly flops, you’re looking at an outright write-off in the $1.1–$1.8bn neighborhood for deployed capital. Once you add goodwill impairments, working-capital burn and FX you can estimate $2bn. Management could still try to sell Hepsiburada and recover some value, but their current stake is marked to market at 520 million, an over 50% haircut (NASDAQGS:HEPS).

Why the downside looks tolerable:

Türkiye is a current drag on the income statement. Strip that drag out, and Kaspi’s Kazakhstan core still looks very good: management forecasts income growing ~15%/yr, and the company today trades at compressed multiples (P/E 6.99, EV/EBIT 3.58). Use the Kazakhstan operating run-rate (add back Turkey losses) as your downside income, apply a conservative haircut, and you get a sensible valuation floor that still leaves upside optionality from Türkiye.

Target market cap $23.5 B in 5 years (10% CAGR). Without multiple expansion (P/E 7.3), net income would need to grow from $2.019 bn today to $3.36 bn. The Kazakhstan core alone can achieve this, making the Turkey expansion optional upside rather than necessary for achieving your target returns.

Over the long term, if Türkiye does not work, they will direct the efforts towards another nation, which can balance out the growth as the Kazakh growth stalls.

Qualitative factors driving growth at Kaspi

Operating leverage. Software development costs are the same whether they have 1 million users or 100 million. Margins scale with the business.

Super-app network effects. Payments, marketplace, lending and banking feed each other: more shoppers → more payment volume → better underwriting data → more lending → more loyalty. That loop compounds growth without equal incremental marketing spend.

Data & underwriting advantage. Decades of transaction-level behavior in a single ecosystem gives Kaspi a superior risk model for consumer credit and merchant economics. That reduces loss rates and improves unit economics.

Customer obsession. Customer experience (speed, returns, checkout) is core to retention. Once users rely on Kaspi for daily finance + commerce needs, switching costs rise.

Owner-operator alignment. Mikheil Lomtadze’s meaningful ownership and mission focus produce long-term decision-makings.

Embedded payments & merchant distribution. Payment acceptance and merchant tools make Kaspi the default for merchants, which grows take-rate and distribution without proportional sales spend.

Cross-sell economics. Low customer acquisition cost for additional products (credit, insurance, savings) drives higher revenue per active user and margin expansion.

Localized market know-how & regulatory navigation. Deep experience in Kazakhstan means they move faster than competitors and can shape product/regulatory outcomes.

Optionality from international expansion. Other markets are upside optionality. If they succeed, it multiplies all the above advantages; if it fails, core Kazakhstan economics remain intact.

You can’t price in AWS. No investors can price in the segments Kaspi hasn’t entered into yet. Low CAC + plus a track record of success are factors in favor of this trend.

And most importantly, what do you think happens when 2 or 3 or all of these act in accordance with each other? It’s what Charlie Munger calls “Lollapalooza” where multiple factors work together.

Don’t count Kaspi out:

Insiders own 43.8% of the company and only a small about of the market cap is available to the public.

Mikheil Lomtadze (CEO, 24.9% owner) is an incredible owner operator. If anyone can make the expansion into Türkiye work its him and the team. Even in the US, you’d be hard-pressed to find someone with skin in the game, as mission-driven, and prioritizing customer satisfaction over short-term financial optics.

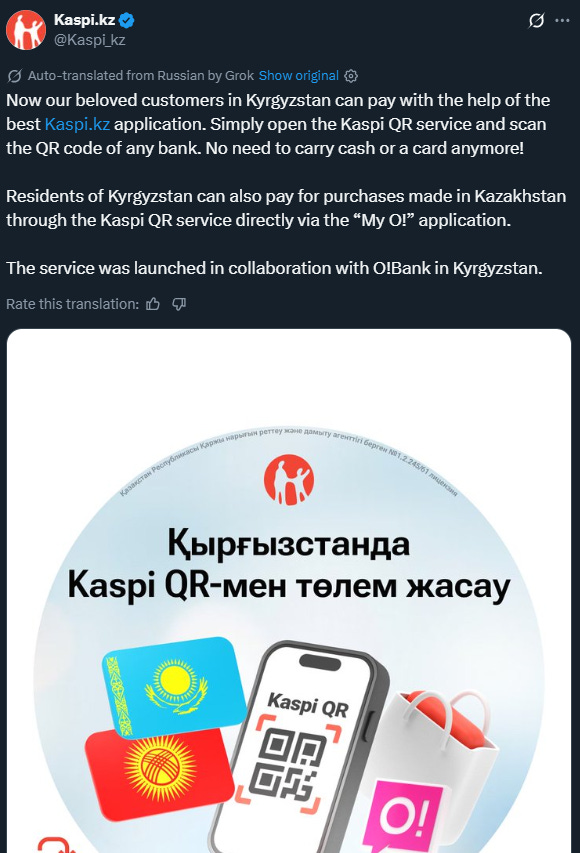

A recent post on X shows that Kaspi has integrated support for payments in Kyrgyzstan. Again it is difficult to price in what you don’t see coming.

Additionally, Goldman Sachs recently upgraded Kaspi from Neutral to Buy.

Risks / Downside

In 5 years time if multiples collapse below ~6×, required growth jumps materially (~14%+). This can happen for many reasons unrelated to the performance of the business.

There is also risks that the Kazakh government could take steps to break up Kaspi’s payments monopoly. One such rumor is that they have considered creating their own payment system, similar to India’s UPI (Unified Payments Interface). However, I discount this risk as this is a massive undertaking that is more likely in a more developed nation like India rather than Kazakhstan. Read here.

OBS! This is a repost of the original article below.

I found it interesting, and I wanted to share it with all Flankers!

Source:

https://substack.com/app-link/post?publication_id=2495981&post_id=175879717&utm_source=substack&utm_medium=email&utm_content=share&utm_campaign=email-share&action=share&triggerShare=true&isFreemail=true&r=23eft9&token=eyJ1c2VyX2lkIjoxMjY2NDQ4NzcsInBvc3RfaWQiOjE3NTg3OTcxNywiaWF0IjoxNzYwMjc4MzM0LCJleHAiOjE3NjI4NzAzMzQsImlzcyI6InB1Yi0yNDk1OTgxIiwic3ViIjoicG9zdC1yZWFjdGlvbiJ9.MtSp86FFqsETdz-JVouXx3qx_tU0kE9LqLY5zyhckhE

https://substack.com/@firsthill

Key Points (AI Generated):

Kaspi.kz is a dominant Kazakh “super app” (payments, marketplace, fintech, e-gov) with very strong network effects and high switching costs.

The stock trades extremely cheap (≈7x P/E, ≈3.6x EV/EBIT), giving a valuation “floor” where the Kazakh core alone can likely deliver ~10%+ annual returns.

Around $1.5B has been deployed into Türkiye via Hepsiburada; even if this is largely written off, the core business still looks attractive.

If Türkiye and other international expansions work, they provide large upside optionality on top of the already solid Kazakhstan base.

Moat-y economics (data/underwriting advantage, operating leverage, merchant lock-in) plus high insider ownership (≈44%, CEO ≈25%) support a long-term, owner-operator story, with key risks being multiple compression and potential regulatory moves against its payments dominance.

Summary (AI Generated):

Kaspi is a highly profitable, entrenched super app in Kazakhstan that currently trades at a very low multiple relative to its quality and growth. Even assuming its Turkish expansion fails and much of that investment is written off, the core business appears capable of delivering roughly 10%+ annual returns from today’s price, creating an attractive downside-protected “floor.” If its international expansion (Türkiye and beyond) succeeds, investors could get substantial upside on top of that base case.