General

Buffett Indicator is over 200%

We're currently at 217%. There is certainly opportunity out there, but we need to wary of valuations.

https://www.currentmarketvaluation.com/models/buffett-indicator.php

Here's what Buffett said about the Buffett Indicator (in 2001, right in the midst of the dot com bust):

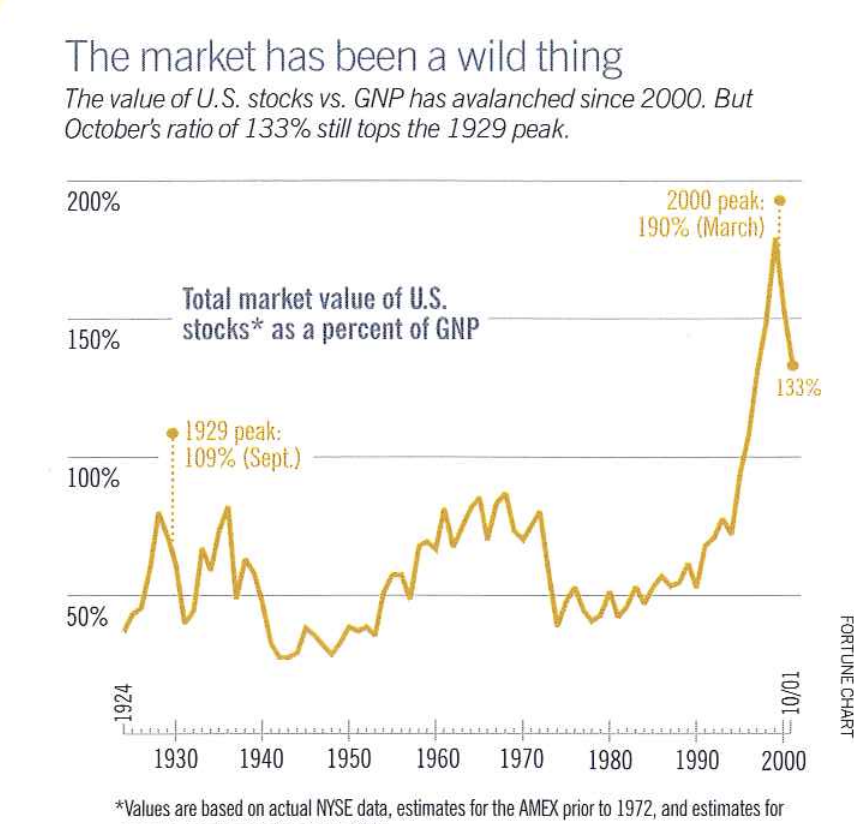

"The tour we've taken through the last century proves that market irrationality of an extreme kind periodically eruptsand compellingly suggests that investors wanting to do well had better learn how to deal with the next outbreak. What's needed is an antidote, and in my opinion that's quantification. If you quantify, you won't necessarily rise to brilliance, but neither will you sink into craziness. On a macro basis, quantification doesn't have to be complicated at all. Below is a chart, starting almost 80 years ago and really quite fundamental in what it says.

The chart shows the market value of all publicly traded securities as limitations in telling you what you need to know. Still, it is probably the best single measure of where valuations stand at any given moment. And as you you can can see, nearly two years ago the ratio rose to an unprecedented level. That should have been a very strong warning signal. For investors to gain wealth at a rate that exceeds the growth of U.S. business, the percentage relationship line on the chart must keep going up and up. If GNP is going to grow 5% a year and you want market values to go up 10%, then you need to have the line go straight off the top of the chart. That won't happen.

For me, the message of this chart is this: If the percentage relationship falls to the 70% or 80% area, buying stocks is likely to work very well for you. If the ratio approaches 200%- as it did in 1999 and a part of 2000-you are playing with fire. As you can see, the ratio was recently 133%.

Even so, that is a good-sized drop from when I was talking about the market in 1999. I ventured then that the American public should expect equity returns over the next decade or two (with dividends included and 2% inflation assumed) of perhaps 7%. That was a gross figure, not counting frictional costs, such as commissions and fees. Net, I thought returns might be 6%. Today stock market "hamburgers," so to speak, are cheaper. The country's economy has grown and stocks are lower, which means that investors are getting more for their money. I would expect now to see long-term returns run somewhat higher, in the neighborhood of 7% after costs. Not bad at all-that is, unless you're still deriving your expectations from the 1990s"

Oh boy was he right. The post-dot bomb era has seen unprecedented growth.

If you've never read the original article, I cannot recommend it enough. https://www.berkshirehathaway.com/2001ar/FortuneMagazine%20DEC%2010%202001.pdf

My key takeaway: keep studying businesses, keep valuing businesses I like. If their price is above what I believe the intrinsic value to be, I'll wait. Patience is key to intelligent investing.