DUOL

Duolingo Inc

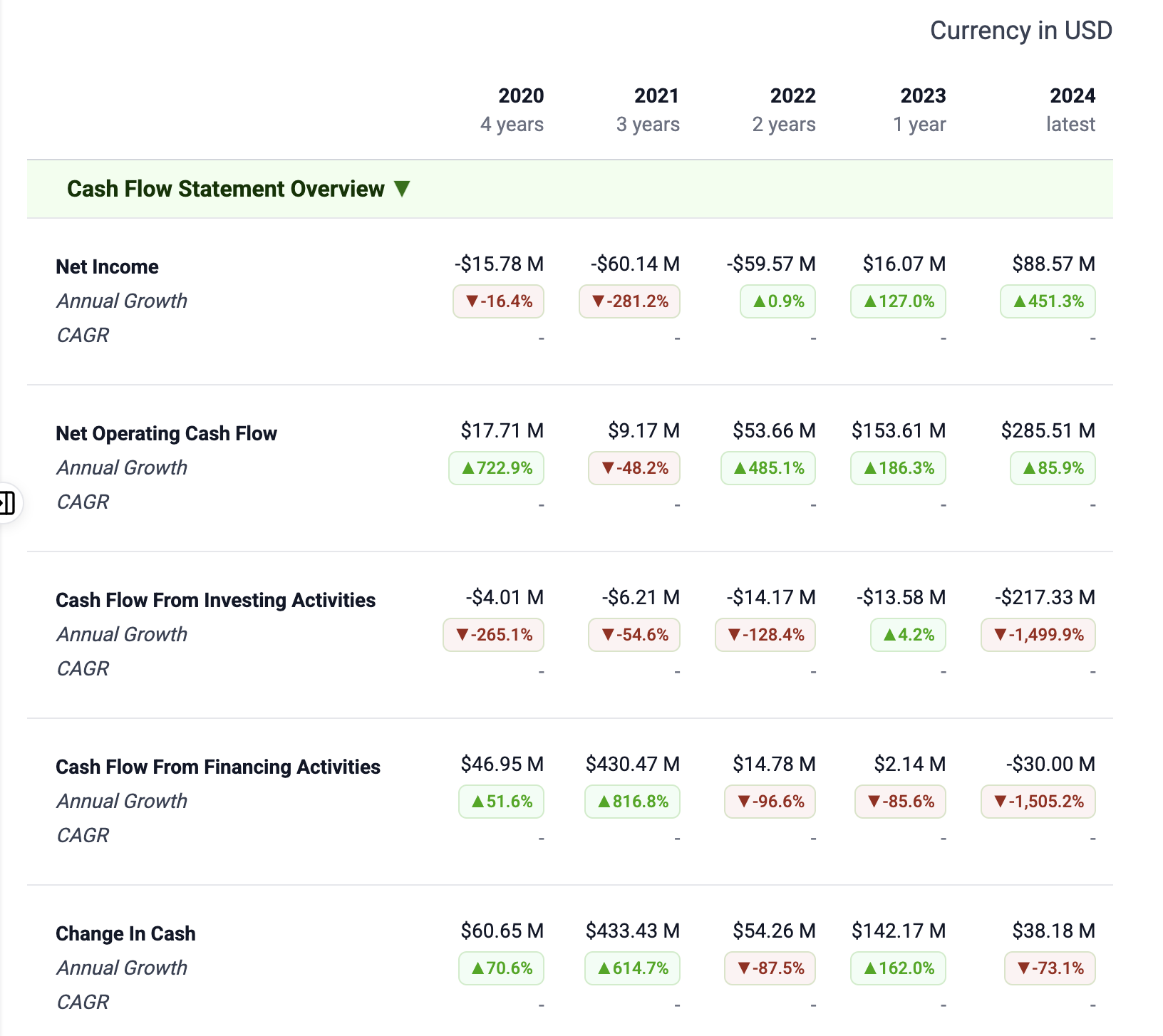

Duolingo Cash Flow Statement

Understand The Cash Flow StatementFrom their 2024 annual report...

Five year trend is, again, fantastic. Duolingo’s cash flow profile is very strong and improving.

Operating cash flow has been consistently positive and climbing... from $9.2 million in 2021 to $53.7M in 2022, $153.6M in 2023, and reaching $285.5M in 2024

This indicates that even during years of net loss, the company’s operations were generating cash (thanks to upfront subscription payments and non-cash expenses like depreciation/stock comp).

Capital expenditures have remained low, generally in the single-digit millions each, which means the majority of OCF translates into free cash flow.

Free cash flow (OCF minus capex) hit roughly $273M in 2024, a very robust figure that has grown each year.

On the financing side, Duolingo received a major cash inflow from its 2021 IPO (~$438M) and since then has not needed new debt financing, even initiating modest share buybacks in 2023.

As Buffett-style investors, our focus is on cash generation, low capital requirements, and wise use of cash – Duolingo’s cash flow statement mostly earns high marks, with a few points to monitor.

Green Flags

Strong and Rising Operating Cash Flow

Duolingo converts its growing revenues into cash effectively.

Operating cash flow jumped from only ~$9M in 2021 to $154M in 2023, then $286M in 2024. Each year’s OCF was higher than the last, outpacing even net income due to non-cash charges and upfront payments. This consistent cash generation is great to see– it shows the company’s earnings are not just accounting figures but backed by real cash.

Notably, even when Duolingo had GAAP losses, its OCF was positive (e.g. 2021–2022) because customers paid upfront (deferred revenue grew) and expenses like stock comp didn’t drain cash. Such a trajectory suggests a business that funds itself and can reinvest for growth without external help.

High Free Cash Flow & Low CapEx Needs:

Duolingo’s free cash flow (FCF = OCF minus capital expenditures) has grown dramatically, indicating an ability to produce surplus cash.

In 2024, FCF was roughly $273M (=$285.5M – $12.1M) Crucially, this is achieved with minimal capital expenditure – capex was only $3–12 million per year over 2020.

Such a capital-light model means Duolingo can support growth and innovation (mostly through R&D, which is expensed on the income statement) without requiring heavy investments in fixed assets.

We love businesses that throw off lots of cash relative to what they must plow back in – Duolingo fits that mold by turning a large portion of its revenue into free cash. This FCF can be used to build cash reserves, acquire complementary businesses, or eventually return capital to shareholders.

Self-Funded Growth (Prudent Capital Allocation)

Since going public, Duolingo has not relied on debt or frequent equity raises to finance its operations – its growth is essentially self-funded by operating cash flow.

In fact, the company has started returning some cash to shareholders: it repurchased about $11.5M of stock in 2023 and ~$49M in 2024.

These buybacks were relatively small (likely to offset dilution from employee stock programs), but they signal that Duolingo generates enough cash to cover its expansion and still have excess.

I view this positively since management isn’t overextending with leverage or diluting shareholders for cash; instead, they appear to be conservative capital allocators – raising a big war chest in the IPO and then operating within their means.

Recurring Revenue Model Boosts Cash Flows

As noted, Duolingo’s subscription model means customers often pay upfront for annual plans, which bolsters operating cash flow. The growing deferred revenue (customer prepayments) has been a significant contributor to OCF each year.

This is effectively interest-free financing provided by users.

Yellow Flags

High Non-Cash Adjustments (Stock Comp)

A large portion of operating cash flow is coming from adding back stock-based compensation.

In 2024, Duolingo added back ~$110M of stock comp expense to arrive at its $285M operating cash flow. While this accounting treatment is correct (stock comp doesn’t use cash), you could argue it’s not “free” cash – it’s essentially paid via dilution.

The yellow flag here is that a significant share of OCF is due to non-cash expenses; if we adjust for ongoing stock grants, the underlying cash earnings attributable to shareholders are a bit lower. In other words, Duolingo’s cash flow is strong, but part of it is achieved by issuing equity to employees instead of paying them fully in cash – a practice that should be watched.

Ideally, as Duolingo matures, we’d want to see stock comp growing slower than revenue, so that more of OCF comes from core operations (subscriptions and services) rather than from this add-back.

Use of Cash for Acquisitions

The investing cash flows show Duolingo has begun deploying cash for strategic acquisitions and internal investments. For instance, it spent about $6.6M in 2024 on acquisitions, and even more (~$33.6M) in the first three quarters of 2025.

So far, Duolingo’s cash acquisitions have been small bolt-ons, which is prudent. This is a yellow flag only in the sense of “keep an eye on it” – ensure that as cash builds up, it isn’t squandered on ill-advised acquisitions or excessive projects.

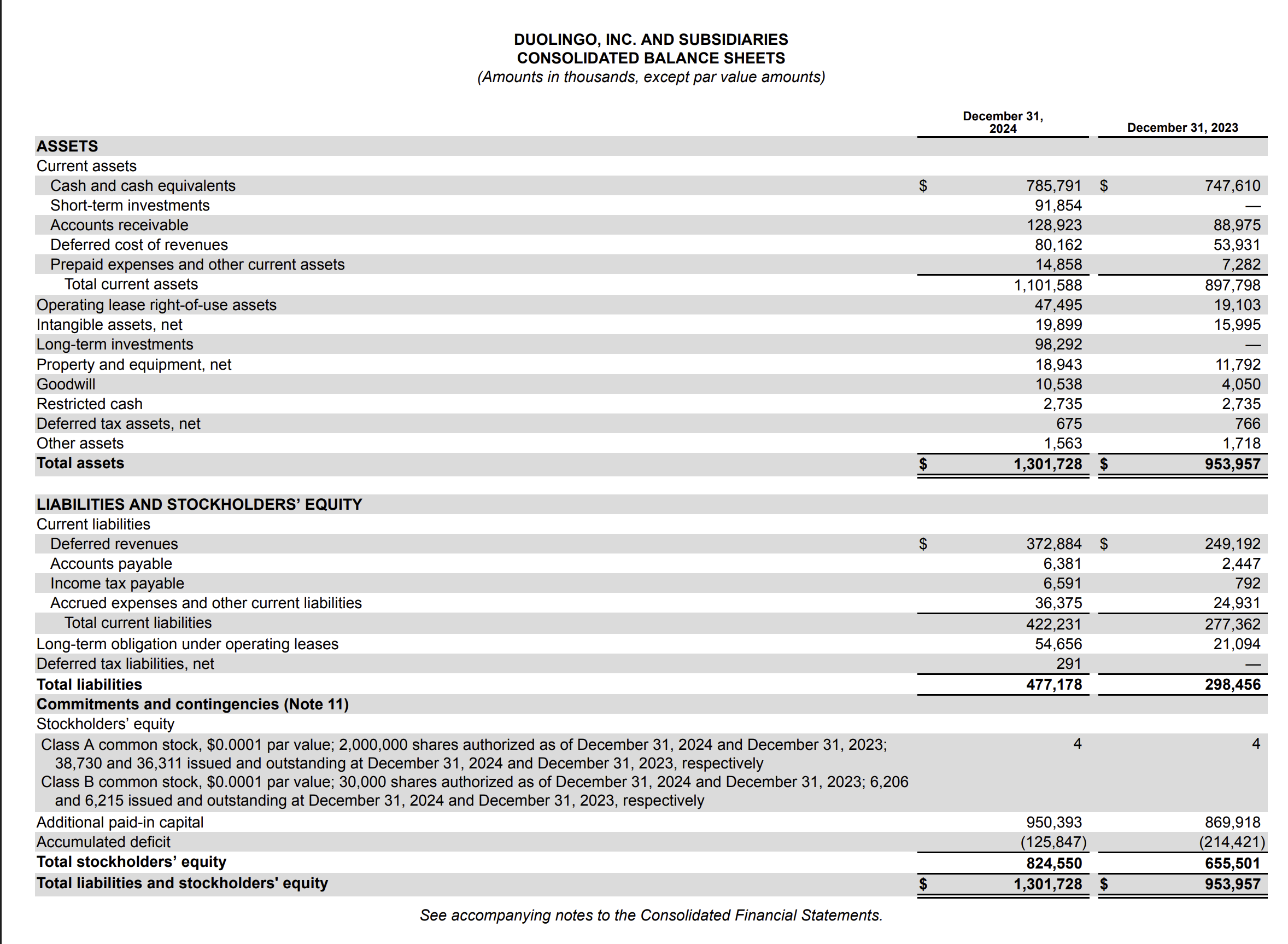

Growing Cash Pile – Deployment Challenges

By 2024 Duolingo had nearly $786M in cash and short-term, and this is likely higher now given continued positive cash flow.

Having a large cash reserve is certainly a strength, but it also raises the question of capital allocation going forward.

When cash piles up in the treasury earns low returns and pressures management to either reinvest or return it.

Duolingo’s management must decide how to best use this cash: continue aggressive R&D hiring, possibly initiate larger share buybacks, or simply retain it as a cushion.

This is a “high-class” problem, but a potential flag if cash continues accumulating without a clear plan. Excessive idle cash can drag down returns on equity.

I would like to see Duolingo only deploy cash for high-growth opportunities, otherwise, they should pay it back to shareholders-- which would be a bit odd for a early growth stage company.

Red Flags

NONE

No Major Red Flags in Cash Generation: Duolingo’s cash flow statement is largely positive. The company is not burning cash; on the contrary, it’s throwing off cash. It isn’t burdened with debt service or aggressive financial engineering that might mask issues.

The only caution that borders on red is to be mindful of how much of the cash flow is tied to continuous user growth (as discussed) and equity-based compensation.

If, hypothetically, user interest waned or the company had to start paying more expenses in cash (instead of stock), cash flow could weaken. But presently, Duolingo’s cash flow health is robust. There are no glaring signs of poor fundamentals in the cash flow statement – no dependence on external financing, no irregular swings, and no unsustainable uses of cash.

The key will be maintaining this trajectory and using the cash wisely – a challenge many young companies fumble, but one that Duolingo is positioned to handle given its strong financial footing.

Overall Sentiment: Bullish+