BRK.A

Berkshire Hathaway Inc

Berkshire's Cash Flow Statement

Understand The Cash Flow StatementFrom the 2024 Annual Report,

Before we go into the Grove discussion, let's look at the Cash Flow Statement as a Forest.

The cash flow statement answers one simple question:

Where did the cash actually come from, and where did it go?

It tells us a story. In Berkshire’s case, it's a story of how capital is being allocated across the five groves.

From the Forest-level:

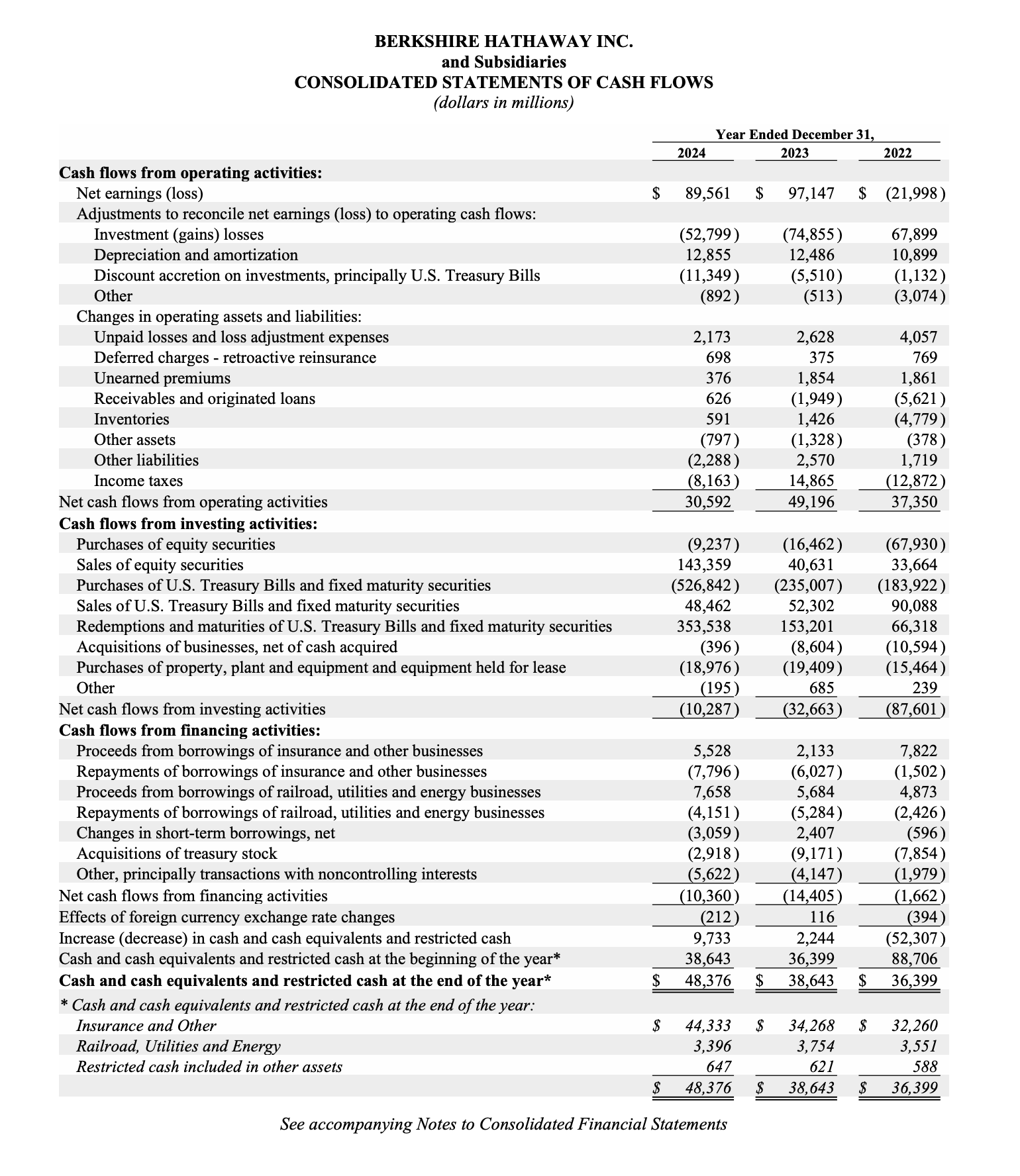

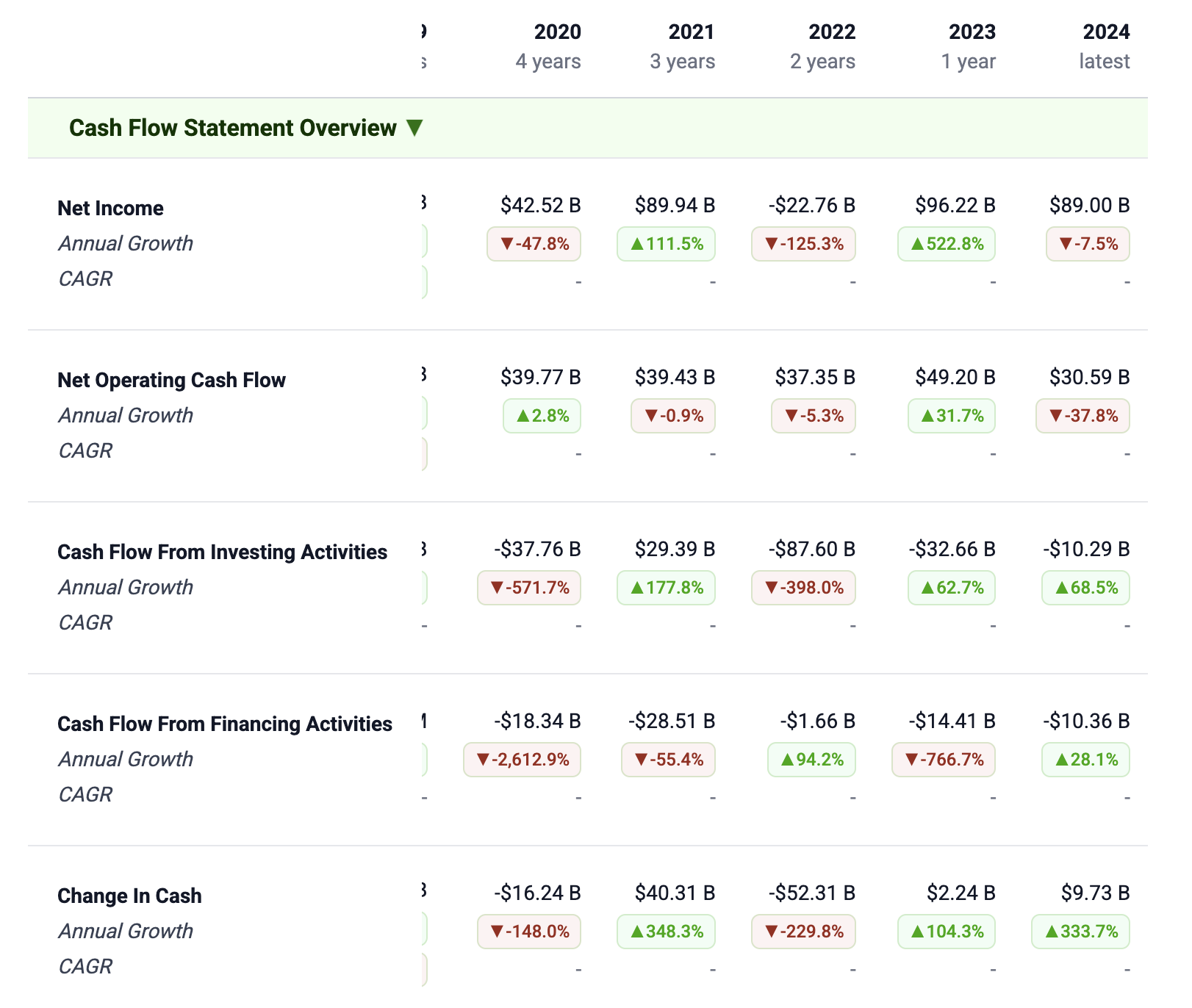

Cash from operating activities: ~$30.6B

Cash used in investing activities: ~($10.3B)

Cash used in financing activities: ~($10.4B)

At first glance, that looks underwhelming relative to $89B of GAAP net income.

That gap is why Buffett tells us not to value Berkshire off reported earnings. Cash flow strips out equity mark-to-market noise and shows you what actually changed economically.

Let's go by Grove:

Grove 1: Controlled non-insurance businesses (cash engines with heavy reinvestment)

This grove shows up primarily in operating cash flow and capex.

Berkshire’s operating businesses generate enormous cash, but they are also capital-intensive:

Railroads, utilities, and energy systems require constant reinvestment

Capex in 2024 was roughly $19B.

My take:

These businesses are not optimized for “free cash flow margins”

They are optimized for durability, scale, and long-term earning power

Grove 1 throws off real cash, but it demands real reinvestment. That’s the price of owning irreplaceable infrastructure.

Grove 2: Public equities

The cash flow statement is where you see what Berkshire actually did in equities.

In 2024:

Equity purchases: ~$9B

Equity sales: ~$143B

That’s ~$134B of net equity selling.

This is one of the most important takeaways from the entire statement... I'm honestly surprised, but then again, at this time Berkshire was offloading a lot of its Apple stock.

It tells us:

Berkshire was not finding enough opportunities at prices it liked

Capital was intentionally pulled out of Grove 2

And redeployed primarily into Grove 4 (cash and T-bills)

Grove 3: Equity-method holdings

Grove 3 doesn’t move the consolidated cash flow statement much.

That’s not because it’s unimportant. It’s because:

Equity-method earnings are largely non-cash

Distributions are irregular

And value compounds internally at the investee level

Buffett would never judge these holdings by near-term cash flow. He judges them by look-through earnings and long-term economics. This is the least important of the moats.

Grove 4: Cash and Treasury Bills

The largest numbers on the investing section are not acquisitions. They’re Treasury bills.

In 2024:

Berkshire purchased hundreds of billions of U.S. Treasury Bills

And rolled or redeemed hundreds of billions as they matured

This is not trading. It’s industrial-scale liquidity management.

Buffett doesn’t “hold cash.”

He runs a massive, constantly rolling T-bill ladder that:

stays liquid

earns real yield

preserves optionality - its the elephant

We can see the strength of their earnings/cash flows in Grove 4. Buffett purchased $526B (!!) in T-bills/bonds in 2024. Holy cow.

Grove 5: Insurance (float shows up as quiet cash dynamics)

Insurance doesn’t scream at us on the cash flow statement.

Float doesn’t appear as a single line. Instead, it shows up through:

Changes in unpaid losses and loss adjustment expenses

Changes in unearned premiums

Retroactive reinsurance balances

In 2024, those items continued to support Berkshire’s investable capital base.

This is classic Buffett:

Insurance cash flows often look like “working capital noise”

In reality, they represent the funding engine that allows Berkshire to invest far more capital than shareholders alone provide

Insurance is not just a business. It’s the financing system for the rest of the forest.

Buffett said this on pg 10 in the Annual report:

Grove 4 is quietly producing real investable capital, even before the cash hits the account.

My takeaway

The 2024 cash flow statement tells a clear story:

Grove 1 continues to generate durable operating cash, with heavy reinvestment (only downside- but also these moats are wide)

Grove 5 continues to finance the system through float

Grove 2 was deliberately shrunk

Grove 4 absorbed massive capital, strengthening the fortress

Grove 3 compounds quietly in the background

This is not a company maximizing short-term cash flow.

This is a company optimizing for flexibility and long-term compounding.

Sentiment: Very bullish