DUOL

Duolingo Inc

Duolingo has a moat, but I'm not sure how durable it is

Is There A Qualitative Moat?Below is my structured breakdown of the moats that matter for Duolingo, and which of them rise above a “competitive advantage” into a durable Buffett-style moat.

Brand Moat

Duolingo has one of the strongest consumer education brands on the planet.

Over 130M monthly users see the Duo Owl, and its meme-driven marketing has become a cultural force — to the point where Duolingo was named AdAge’s “Marketer of the Year” in 2024.

The brand is tied to the idea of gamified learning. It's a combo of a core habit (learning), reinforced daily by streaks, notifications, characters, achievements, and social identity.

More people learn languages on Duolingo than in all U.S. public schools combined, making the brand synonymous with “learning a language online.”

Few competitors have ever created a consumer ed brand with this level of emotional stickiness, global reach, humor, and trust.

The biggest problem I see to their brand moat is the efficacy. I've heard a lot of longtime Duolingo users who say, "yeah, I had a 500-day streak, but I feel like I can't speak French".

I think this is a legitimate concern, but given how strong the company is at technology, I believe the efficacy of the app will improve drastically over time.

Their brand-strength is also improving with their certifications. The Duolingo English Test (DET) is accepted by more than 6,000 programs across colleges and universities.

Sentiment: Bullish

Switching Moat

While Duolingo doesn’t have switching costs like enterprise software, it does have behavioral switching costs, which can be just as powerful in consumer apps.

Users build long streaks, unlock characters, earn XP, climb leaderboards, and accumulate personalized progress tracked by Duolingo’s AI models (Birdbrain).

But yeah, you can quit anytime.

Sentiment: Neutral

Toll Moat

Duolingo does not have a pure toll moat in its core app (it isn’t the only way to learn a language).

But it does have an emerging toll moat in one business line: the Duolingo English Test (DET).

Once institutions bake DET into admissions workflows, it effectively functions like a toll: students must take it, and only Duolingo can provide it. This moat is early but growing.

But a competitor could snatch this up relatively easily.

Sentiment: Neutral

Network Effect

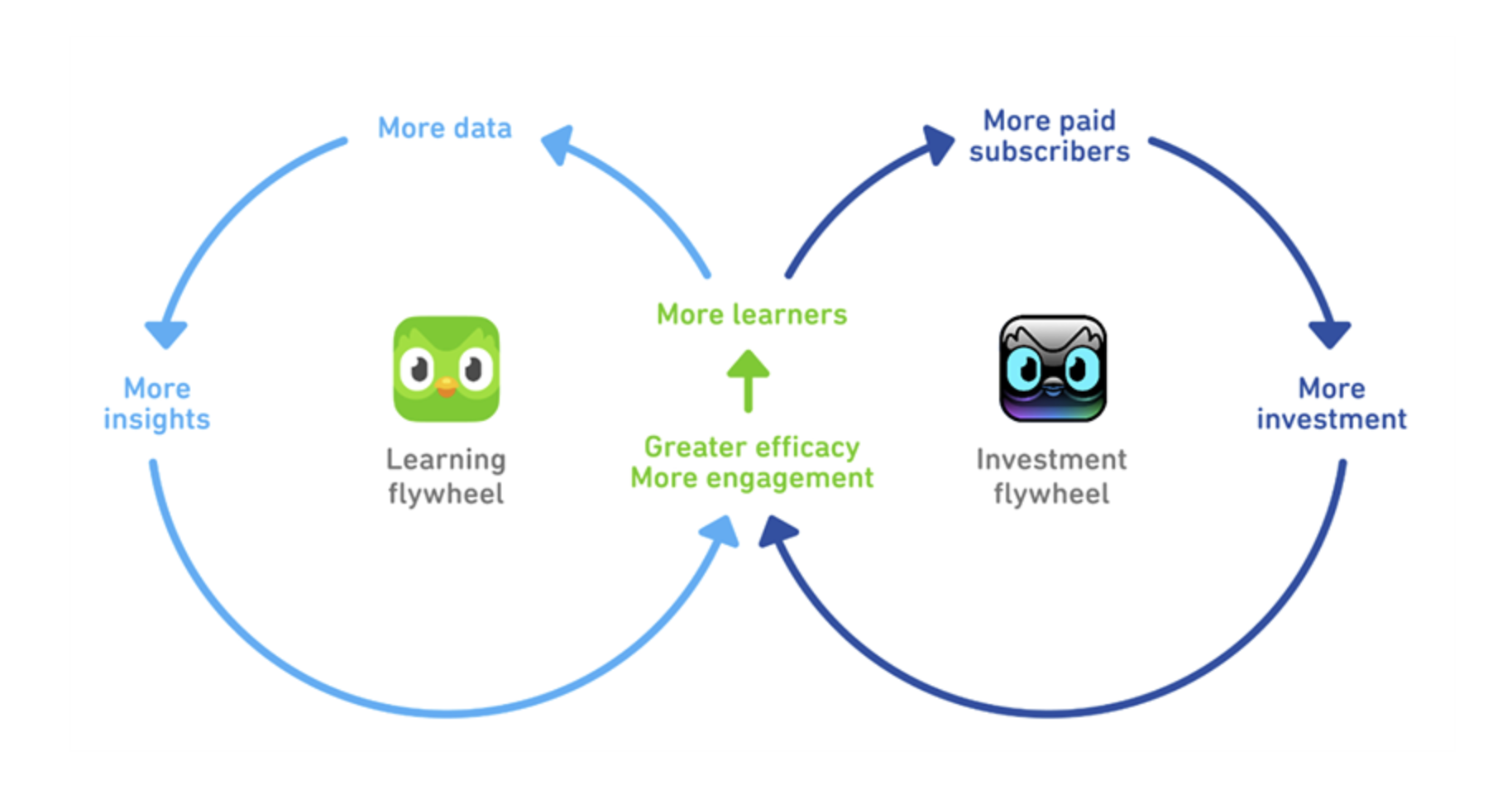

Duolingo has data network effects, and some social network effects.

Every lesson completed (billions per week) trains their personalization engine (Birdbrain) and their generative-AI course creation system, making the product better for the next user.

As Duolingo rolls out AI conversation partners and AI-generated lessons, the data advantage compounds — leading to faster improvement, better accuracy, and superior learning outcomes compared to smaller apps.

A competitor cannot “buy” this data; they would need years of global usage at Duolingo-scale.

Sentiment: Bullish

Economies of Scale

This is the beauty of software businesses.

Duolingo converts scale directly into margin expansion. Once you build the app, the incremental cost to teach one more student is close to zero.

With MAUs above 130M, DAUs above 50M, and 70%+ gross margins, Duolingo has reached a scale where each additional user improves profitability.

AI-generated content amplifies this advantage by dramatically lowering the cost and speed of developing new courses.

In 2025, Duolingo doubled its course catalog using generative AI, something a smaller competitor could never afford.

Sentiment: Bullish

Innovation Moat

This is one of Duolingo’s most powerful moats... possibly the moat.

Under CEO Luis von Ahn, Duolingo operates like a perpetual innovation engine: thousands of A/B tests running at any time, rapid iteration, constant gamification improvements, and a deep integration of AI across the product.

Duolingo Max’s AI conversations, the new Real-Time Feedback tutor, AI storytelling, and AI-generated Adventures are proof of an innovation pace previously unmatched in ed-tech or language learning.

It's a bit old, but here's a 2022 blog post from CEO Luis Von Ahn on Duolingo's culture of innovation

Sentiment: bullish

Secrets Moat

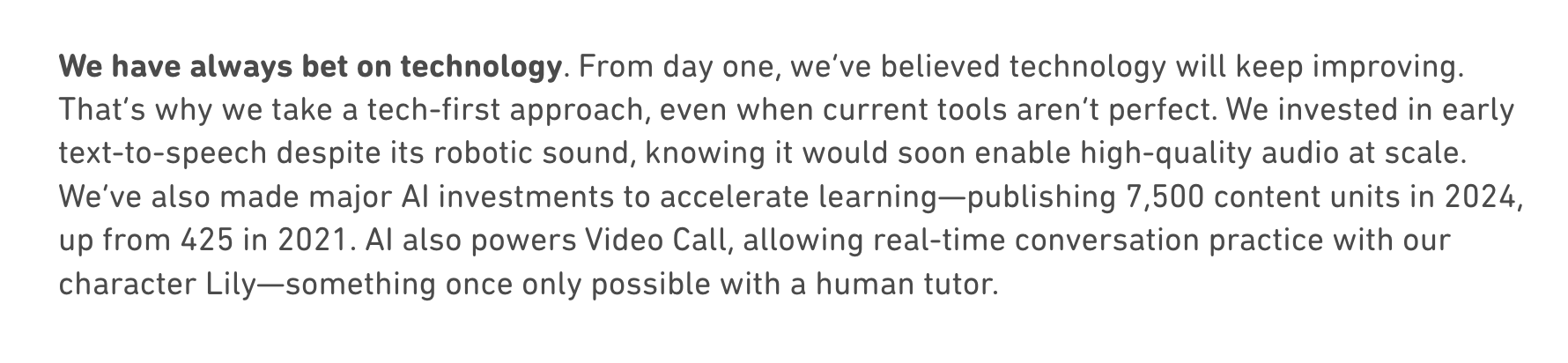

Duolingo doesn’t rely on patents, but it does have proprietary secrets:

Birdbrain, the adaptive learning AI model trained on years of user data

AI content generation tooling that cut course creation time from years to weeks

A massive proprietary dataset on how people learn languages, errors, pacing, difficulty curves

These secrets can’t be easily replicated because they require both the data flywheel and the learning science expertise that Duolingo accumulated over a decade.Competitors like Babbel or Memrise simply don’t have this multi-year advantage in data density or model refinement.

Which is why Duolingo being primarily a technology company has its advantages. From their company strategy document:

Sentiment: bullish

Barrier to Entry Moat

Building a global, gamified, AI-first learning platform at Duolingo’s level is extremely difficult. You need:

Tens of millions of daily users

Thousands of A/B tests per year

AI infrastructure, training data, machine learning expertise

Gamification design at scale

A brand people actually want to engage with

A free tier that monetizes 8% of users profitably

The biggest barrier: The willingness to offer the core product free, which requires enormous scale to make the freemium model work. New entrants cannot realistically catch up without burning billions. Even Big Tech hasn’t been able to replicate the engagement or identity-based loyalty.

Sentiment: Neutral

Monopoly Moat

Duolingo isn’t a monopoly in the antitrust sense... but it is the monopoly of consumer mindshare in language learning.

It has become a verb ("I’m Duolingo-ing Spanish"), and its social presence makes it feel unavoidable. In app stores, it is ranked far above every competitor.

In schools, students consider Duolingo the default app for language practice. Cultural memes reinforce this dominance.

Sentiment: Neutral