BRK.A

Berkshire Hathaway Inc

Berkshire's ...bad...? Past Growth

Is The Business Growing?THIS IS WHY DOING THE STEPS ARE IMPORTANT

I'm honestly shocked by what I'm seeing on Berkshire's recent growth. Obviously you adjust the scope of time >9 years, Berkshire has grown at an amazing rate.

In fact, if Berkshire's stock price dropped by 99%, it would STILL have beaten the SP500 since 1965... this speaks more to the power of compound interest than anything else.

But the near-term does not share Berkshire's long-term glory.

Let's do the numbers...

9-yr/5-yr/1-yr CAGRs: (checkout the Course if this doesn't make sense)

Revenue: 6.7 / 7.8 / 1.9%

Net Income: 16(!) / 1.8 / -7.5.

Total Equity: 10.5/8.9/15.7 (!!)

FCF: -3.6%/-12.5/-61(!!)

That revenue slowdown is scary. Buffett has long warned about the "law of big numbers".

I found this Great bearish article (need to recruit this guy as a Flanker), and he shared my concern.

And he made a great possible explanation, it's bleak, but cogent:

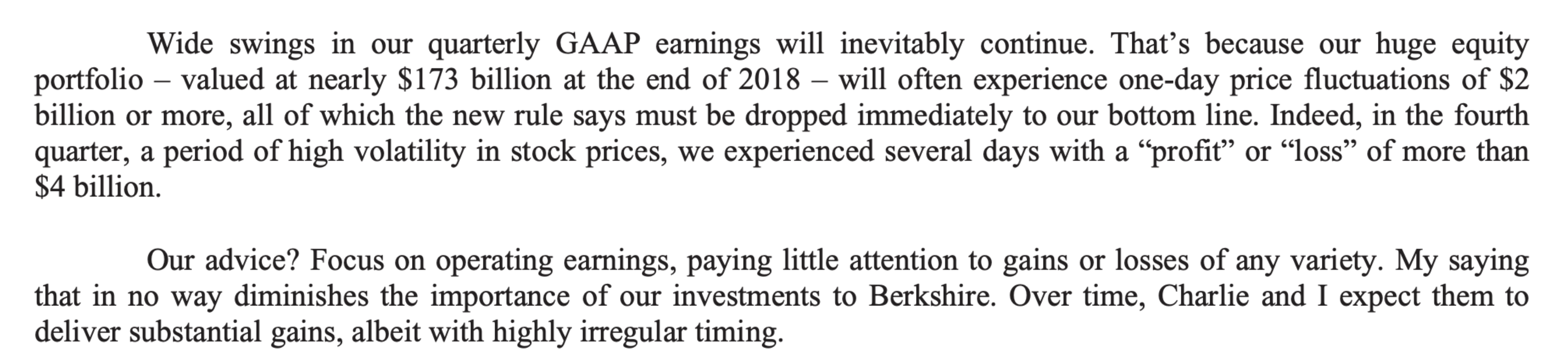

Net Income is not super important when analyzing Berkshire, Buffett has long written about what to look for in a Holding company like Berkshire..

From the 2018 Chairman's letter (thanks, Logan, for reminding me):

Ugh, as I'm writing this article, I'm literally remembering all of the various things that make our usual steps of analyzing businesses not work here... I'm going to need to spend more time on this, I will update this post later

(and when I update, a lot of users said version control is annoying on Flank rn. i'll also be on the lookout for that for improvements we can make)

Hope everyone is doing well! GIVE A FLUX AND TAKE THE CHALLENGE (if you want)

Update 1/26/25:

Here's why our traditional past growth metrics don't work for Berkshire:

Revenue:

Berkshire is a conglomerate that keeps acquiring businesses

Revenue jumps when a business is acquired even if no value was created (this is what makes M&A such a Siren's Song

Net Income:

Berkshire owns huge equity stakes (Apple, Coke, AmEx, etc.)

Accounting rules force unrealized market gains and losses through net income

This creates massive volatility that has nothing to do with operating performance

Total Equity

Absolute size says nothing about owner enrichment

FCF

Insurance float distorts cash generation

Cash inflow/outflow represent float growth (for insurance), not true owner earnings

Buffett has instead said to focus on value creation per share, not how the top line looks.

So where should we look instead?

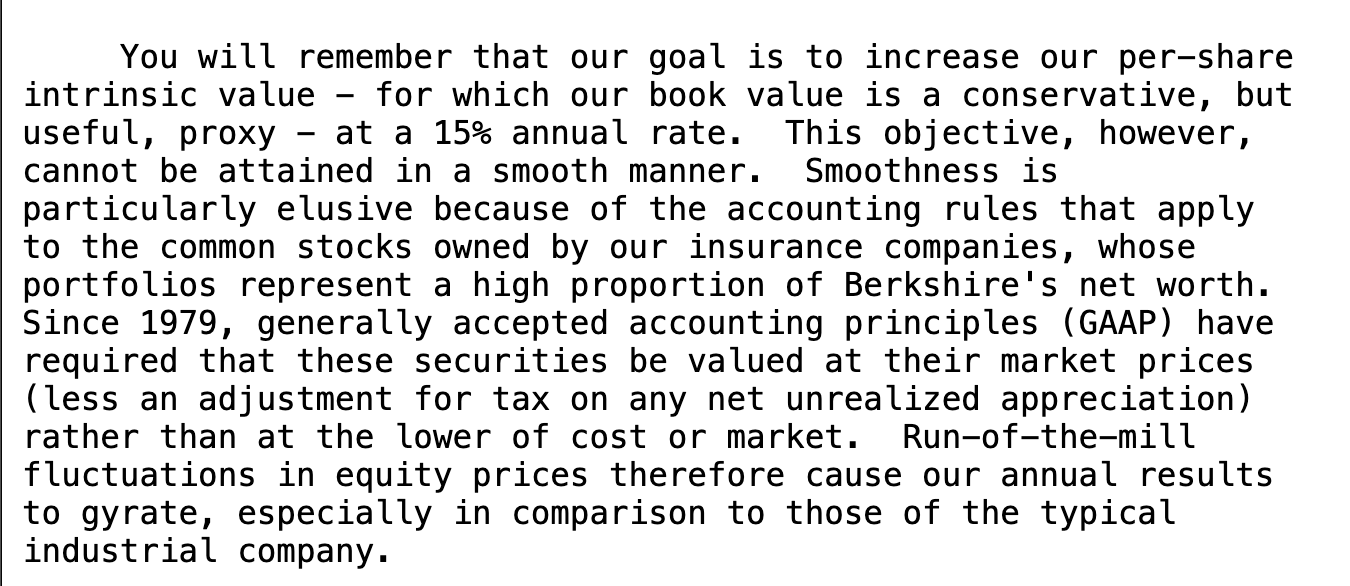

Book Value Per Share

This is the metric Buffett used as his yardstick for decades.

He likes it for a few reasons:

Smooths out accounting noise

Captures retained earnings

Reflects growth in intrinsic value reasonably well

"But Dave, isn't Total Equity === Book Value?" YUP! It is. But the per share part matters here tremendously.

Here's the 1992 Letter:

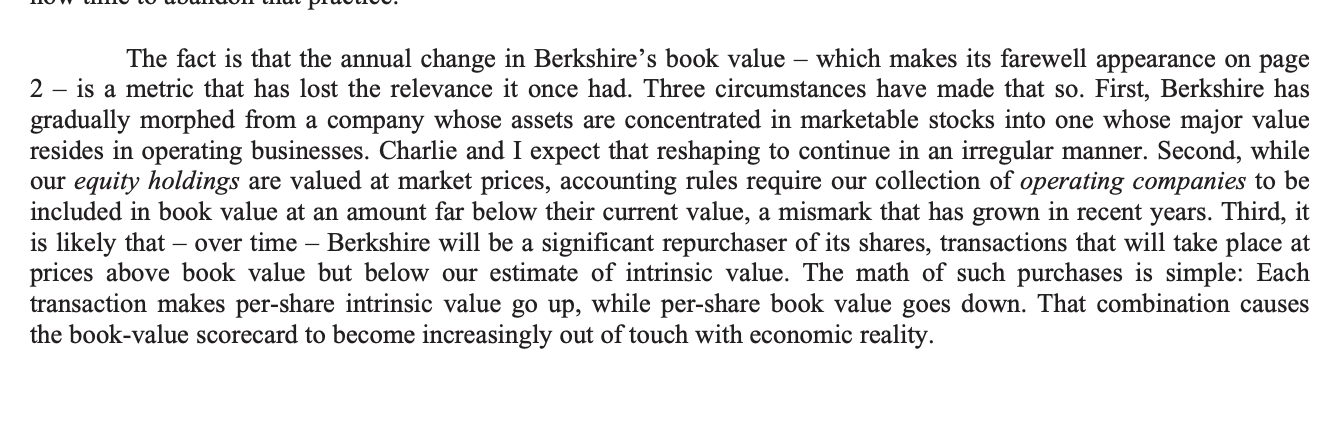

But then in 2018, Buffett wrote that BVPS lost it's value for valuing Berkshire (DOH!)

And, thank goodness, Buffett tells us what to focus on post-2018. It's a great paragraph, read it.

"I believe Berkshire’s intrinsic value can be approximated by summing the values of our four asset-laden groves and then subtracting an appropriate amount for taxes eventually payable on the sale of marketable securities."

So the "groves" I'll be focusing on are:

Berkshire's many non-insurance businesses that Berkshire controls

Berkshire's collection of equities (5-10% ownership-- like $KO, $AMEX, $AAPL)

Berkshire's 'quartet of companies in which we share control with other parties' (like 26% of Kraft, 38% of Pilot Flying J (as of 2018))

US Treasury Bills holdings and cash equivalents

Insurance Operations

So that's what I'll be focusing on in my analysis moving forward! PYAHH!!