General

My Analysis of SpaceX's S-1 (IPO)

Alright, I'm going to try to go into this with an open mind.

But I have to say one thing up front. The fact that they are trying to go public at a $2 trillion valuation is reprehensible to the highest degree.

Apple went public at an $1.8B valuation in 1980. Amazon went public at an $440M valuation in 1997. Hell, even Tesla went public at an $1.7B valuation.

SpaceX is asking you to buy the stock for 100x revenue. 100x revenue. ONE HUNDRED TIMES REVENUE.

Venture capitalists and private investors have gotten all of the juice out of this company, and they're throwing over the nasty, rotten rind to us.

At least in the near term. I absolutely recognize the value of the total addressable market that SpaceX is going after. If they are successful in making life multi-planetary, then the upside could be in the hundreds of trillions of dollars.

But I don't think that's the case.

If you're unfamiliar with S-1's they are [explain S-1]s

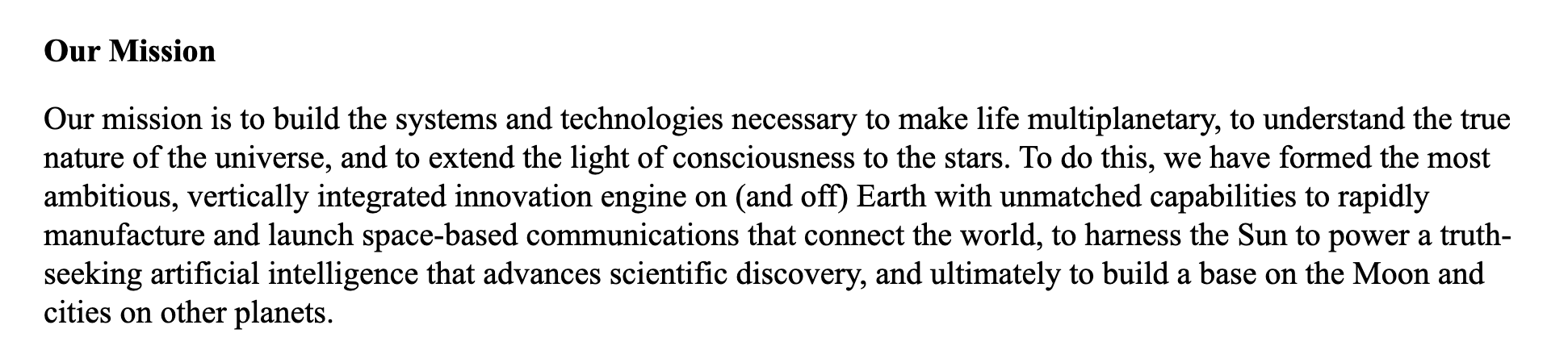

SpaceX's mission

I love this mission statement. If they would have gone public at a $100 million valuation years ago, I would have been an investor.

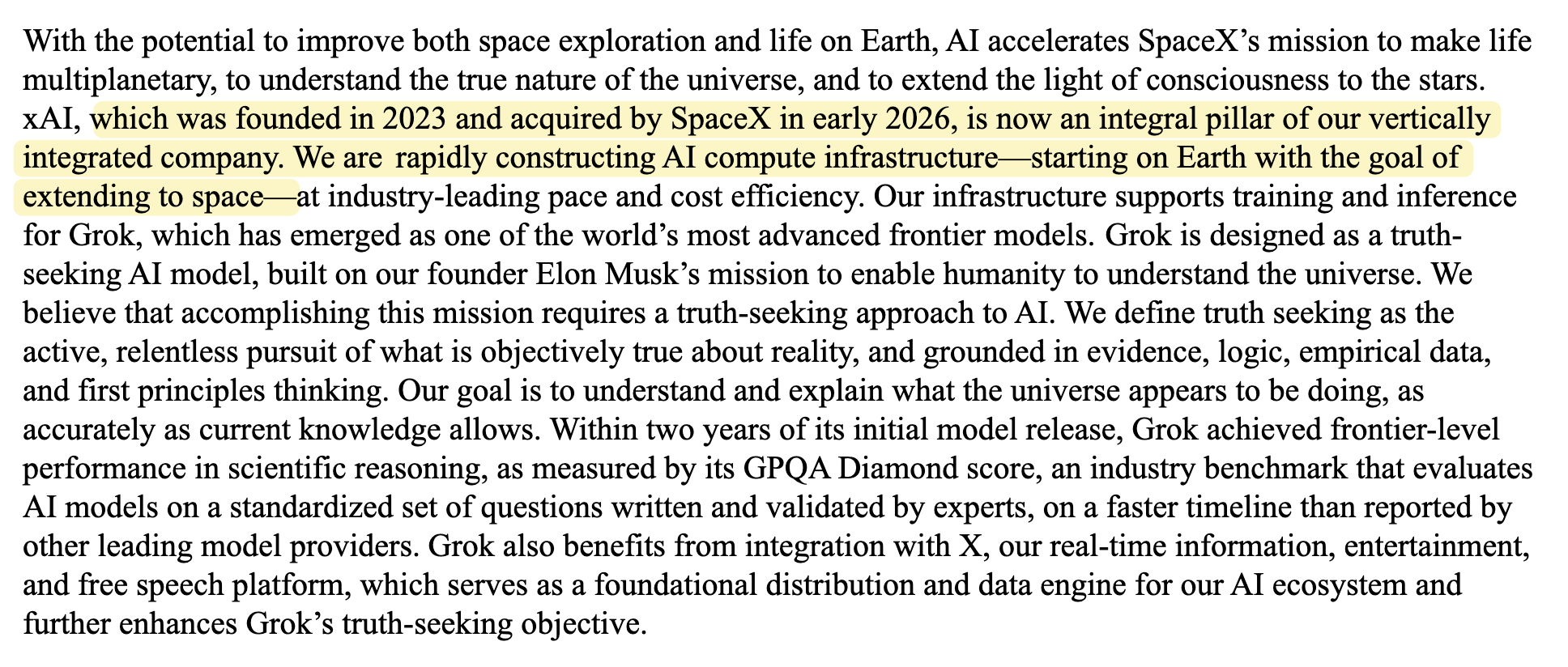

And of course, in the Overview, they had to talk about throwing the dirty (money-losing) diaper that is xAI into it somehow:

Data centers in space are a great idea, in my opinion, but it also seems like it is decades away and not a near-term goal. This is a common thing we see in Musk's companies (overpromise and underdeliver on ambitious timelines)... It's important to note, they believe they will have orbital AI compute satellites as early as 2028 (suuuuuuure, Elon)

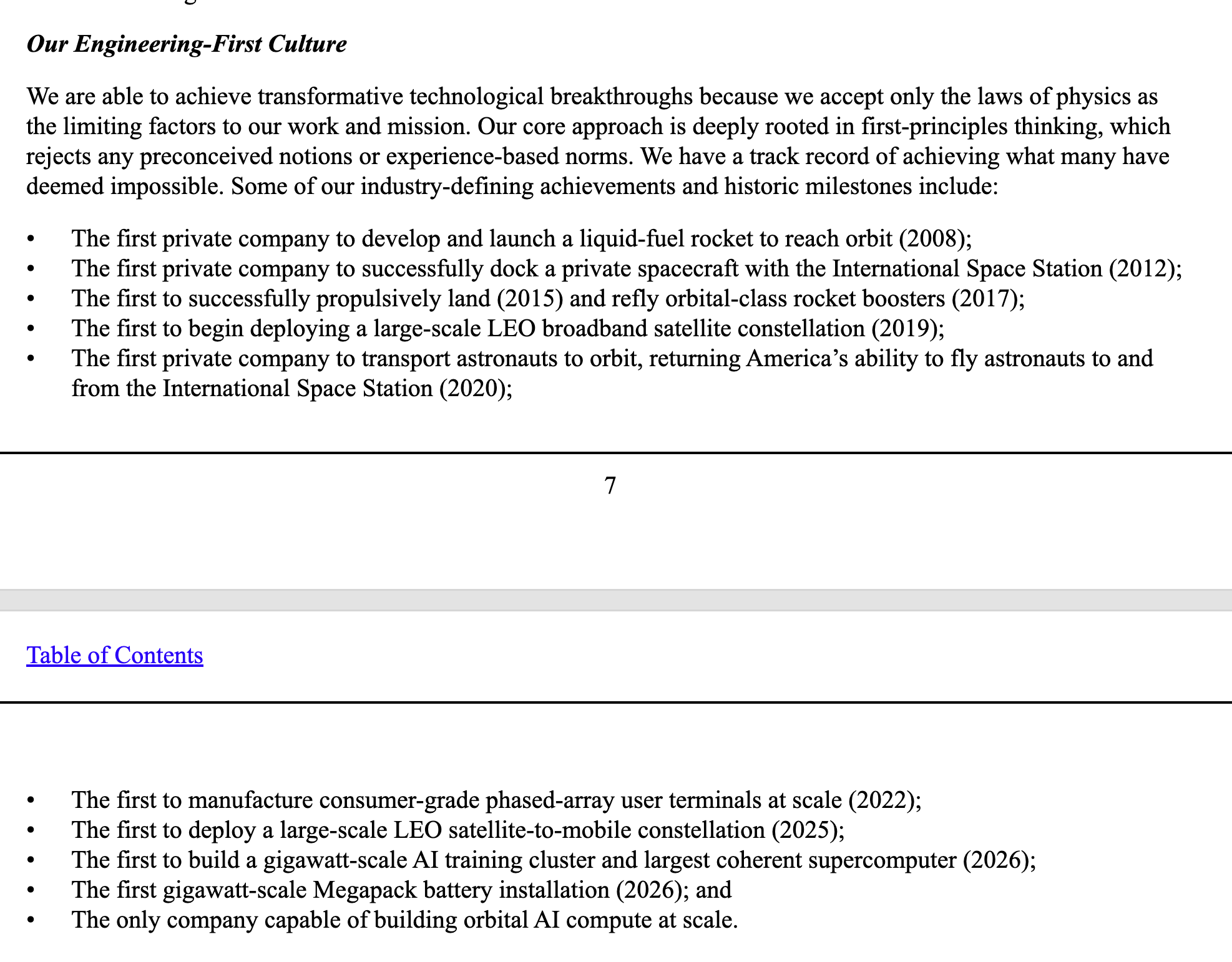

Later in the S-1, they talk about their Engineering First culture. I love this. They've done amazing things so far - that is undeniable.

SpaceX's segments

They are breaking SpaceX into 3 BU's:

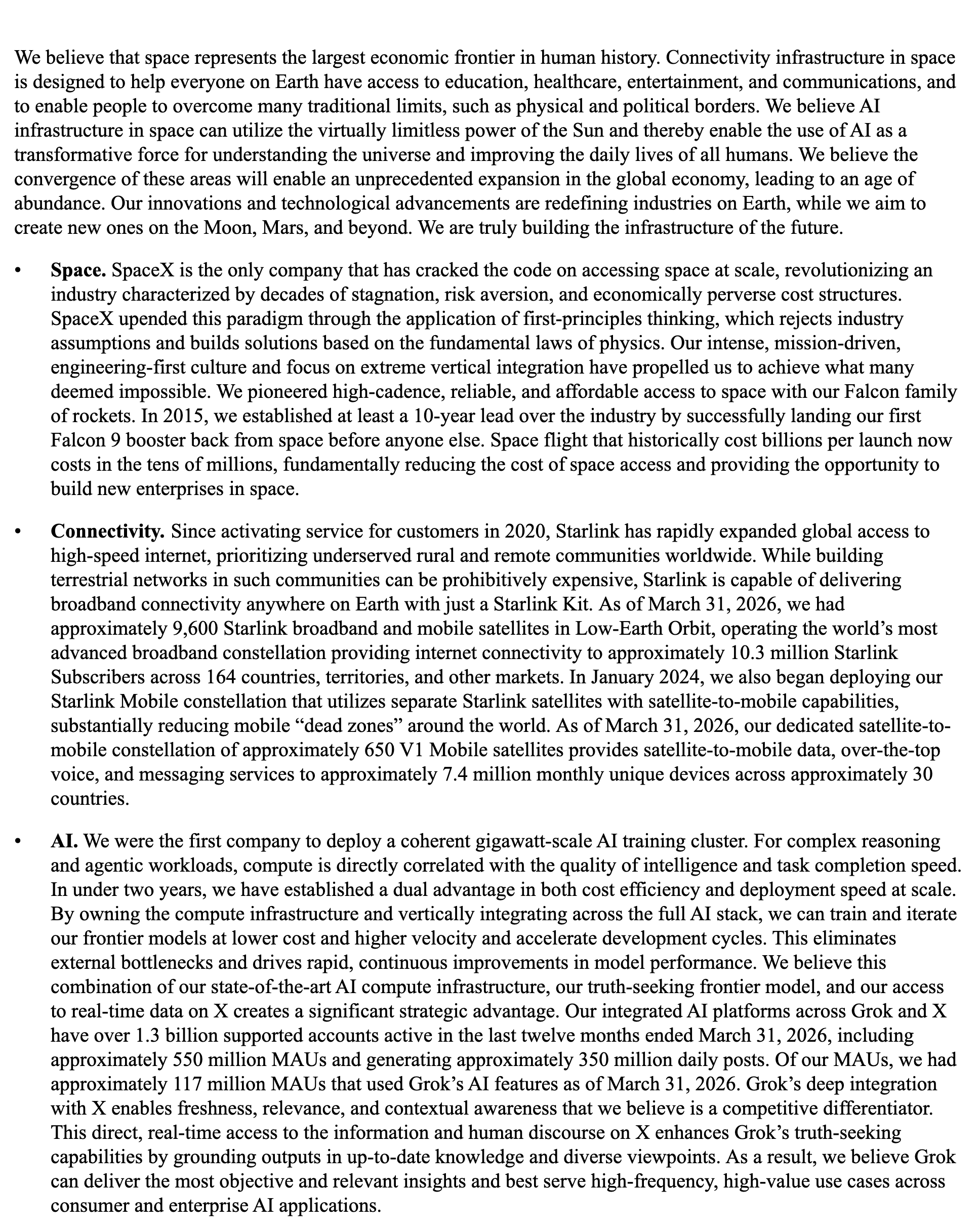

Space

Connectivity

AI

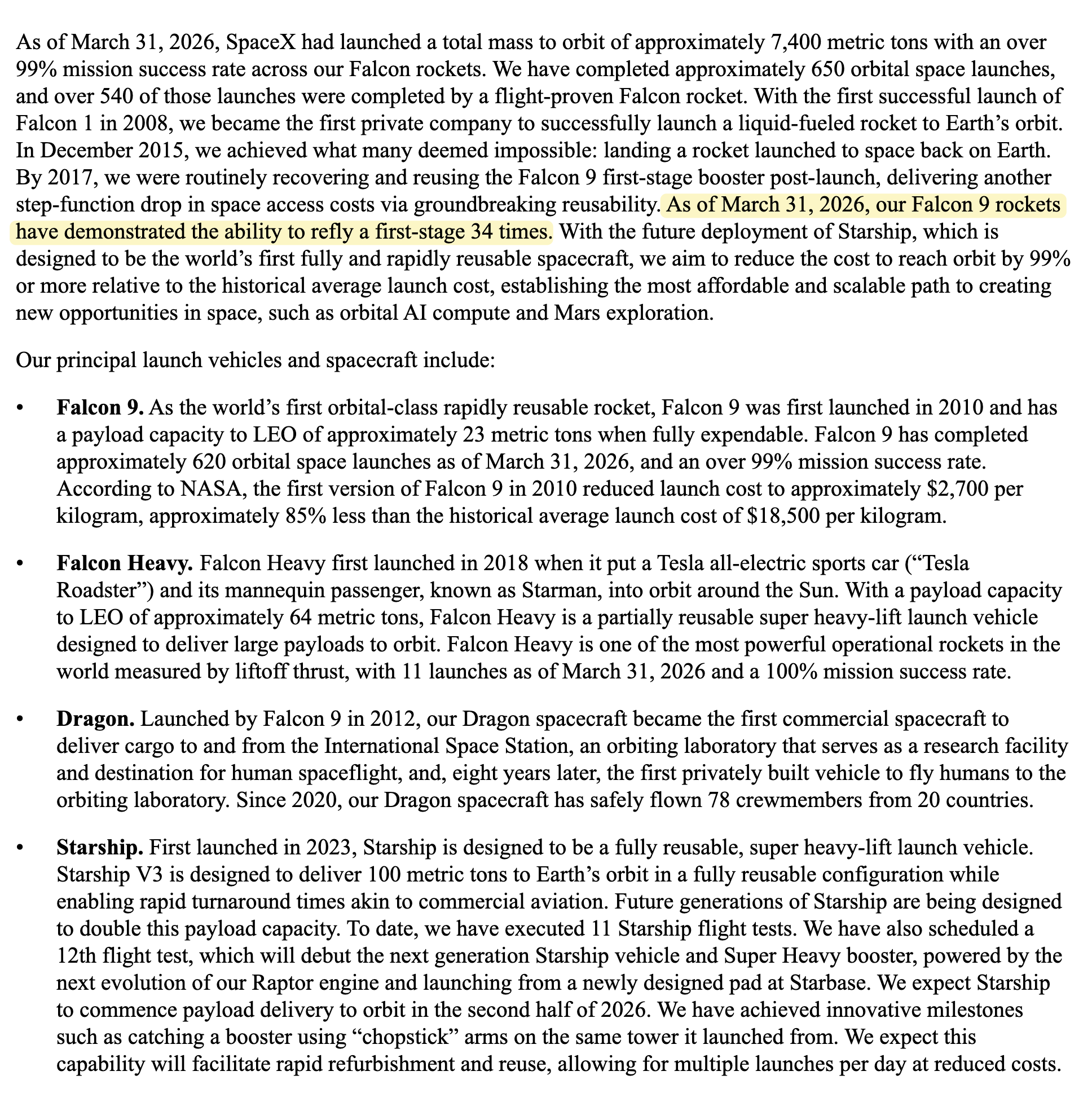

Amazingly, they say that their Falcon 9 rockets are capable of reflying up to 34 times. That is truly a modern marvel of engineering. If only they went public sooner...

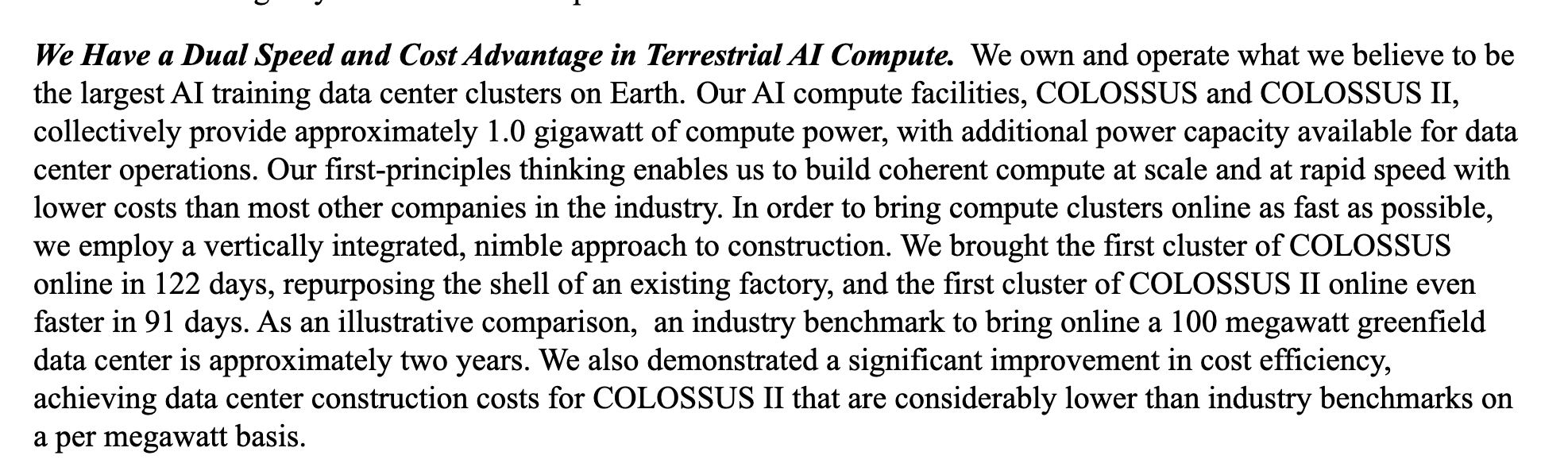

Their speed of AI training data centers is also absolutely incredible... they built COLOSSUS I and II at 122 and 91 days respectively. COLOSSUS are the first 1.0 gigawatt compute data centers in existence. Damn.

They reallllly try to hammer into potential investors that Space data centers is the next big thing for SpaceX... which I do agree with. But there's a lot of things that need to happen between then and now.

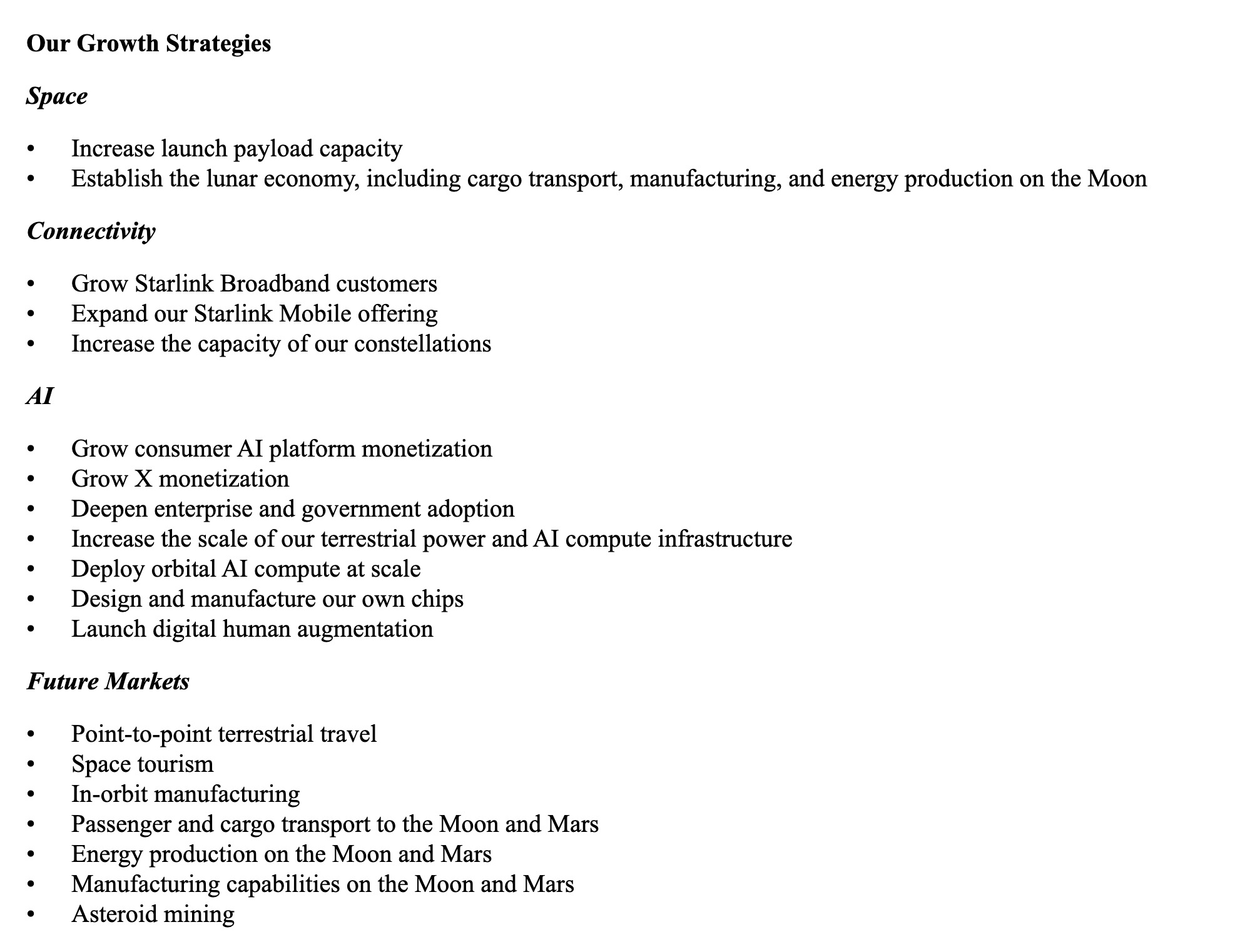

SpaceX Growth Strategies

Always love to see when they lay this out clearly. Here's what SpaceX is planning:

These strategies sit on a steep gradient from shipping-today to physics-class science project, and the prospectus quietly buries the most speculative items at the bottom of the list.

Connectivity is the only bucket actually executing right now: Starlink broadband and direct-to-cell (Starlink Mobile) are live and throwing off real cash, and "increase constellation capacity" just means launching more satellites, which they do better than anyone alive.

The middle tier is real but expensive and unproven at scale. "Increase launch payload capacity" rests entirely on Starship, which still hasn't put a payload in orbit and only just got a V3 debut date. Terrestrial AI compute plus X/consumer/enterprise monetization are genuine businesses, but that's the exact segment bleeding $6.4B at the operating line. And "design and manufacture our own chips" (Terafab) is, by the filing's own admission, only a "general framework" with Tesla and Intel, with no committed projects, timelines, or capex attached yet.

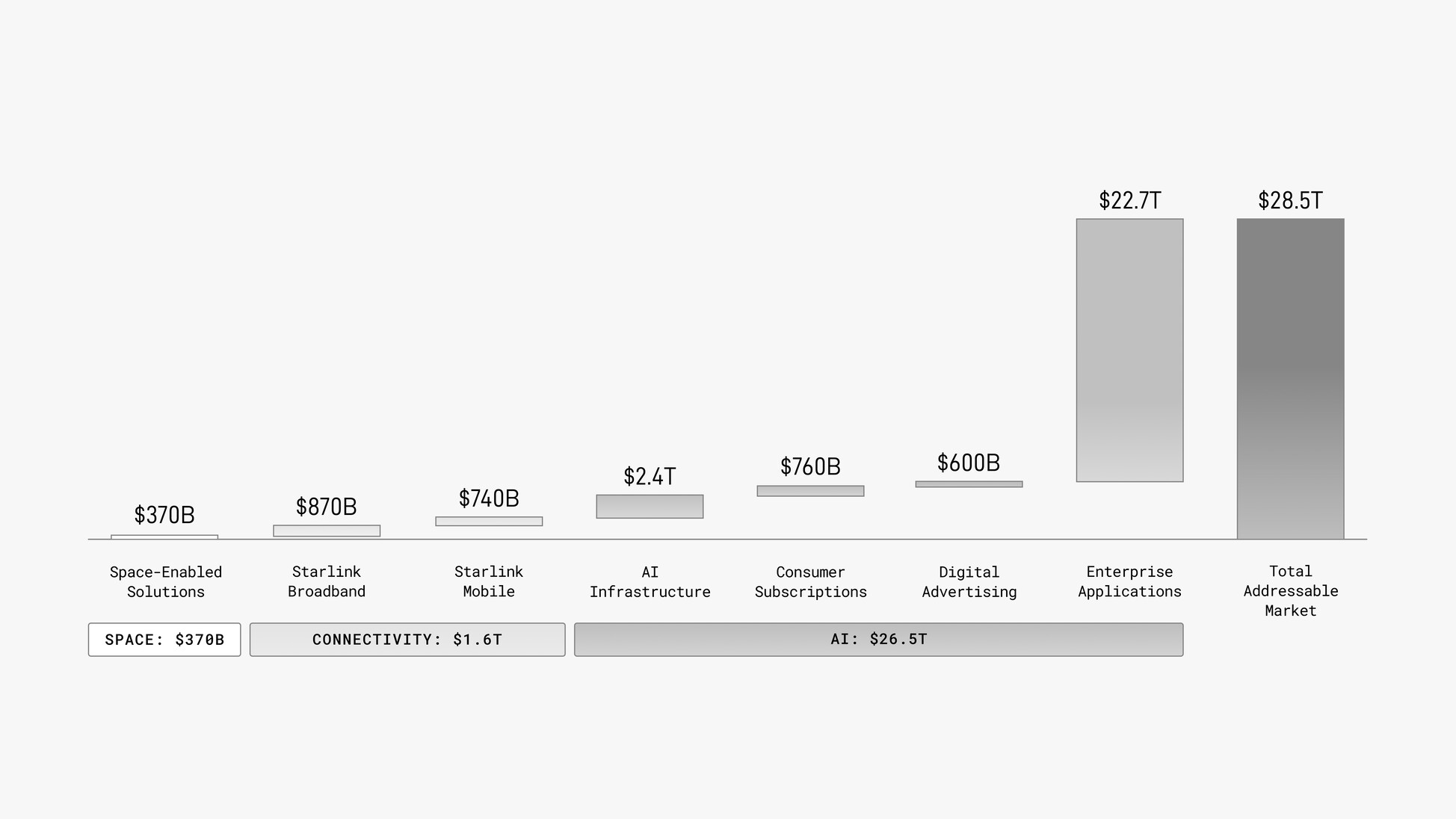

They call our that the total addressable market is $28.5T (typical Musk inflation):

VERY important to note what they are calling out as the opportunity here: almost 80% of this TAM is in "Enterprise Applications"... what?

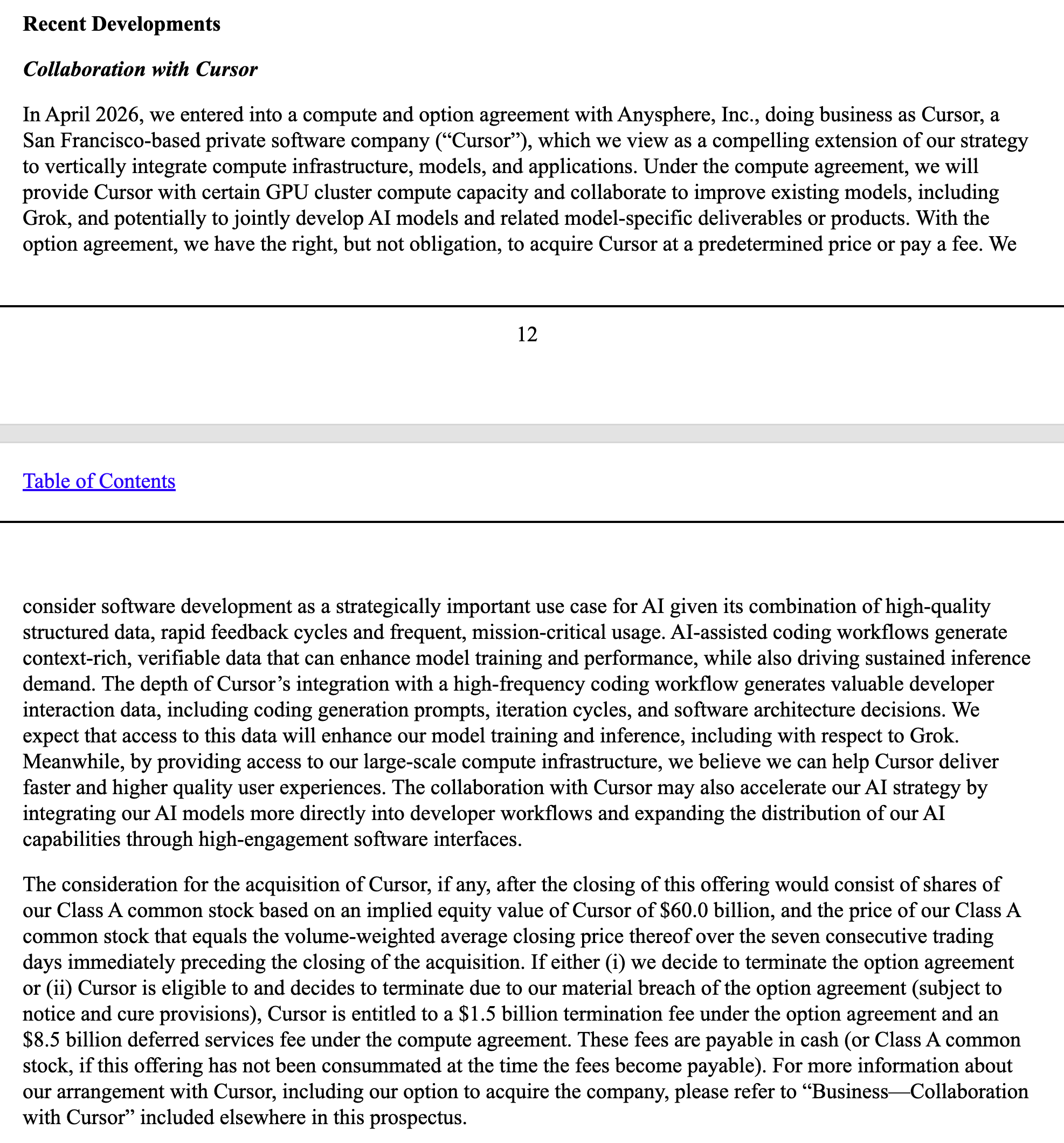

And to make this come true... they have to do... M&A?! What happened to the amazing team that can do anything better than everyone on and off Earth?? If the Enterprise Applications is 80% of their growth strategy... shouldn't that be homegrown? Why would they need to acquire a company for $60B? Yeah, that's $60B with a B.

The numbers

One of the big reasons investors love S-1's is because it's our first look into a Company's financials.

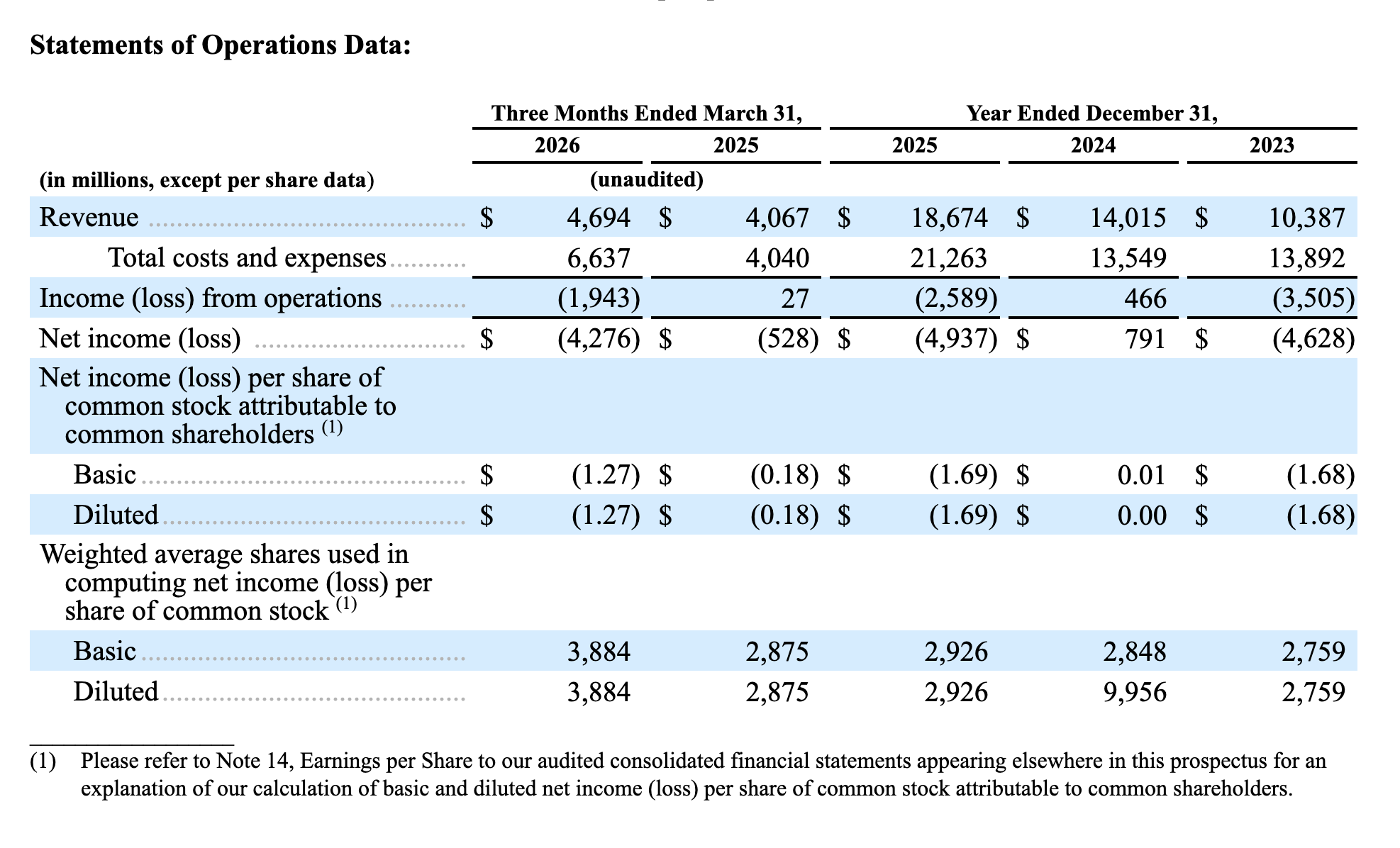

Given that SpaceX is planning the largest IPO in human history, surely they are printing cash.

Wrong.

The company lost almost $4B in net income.

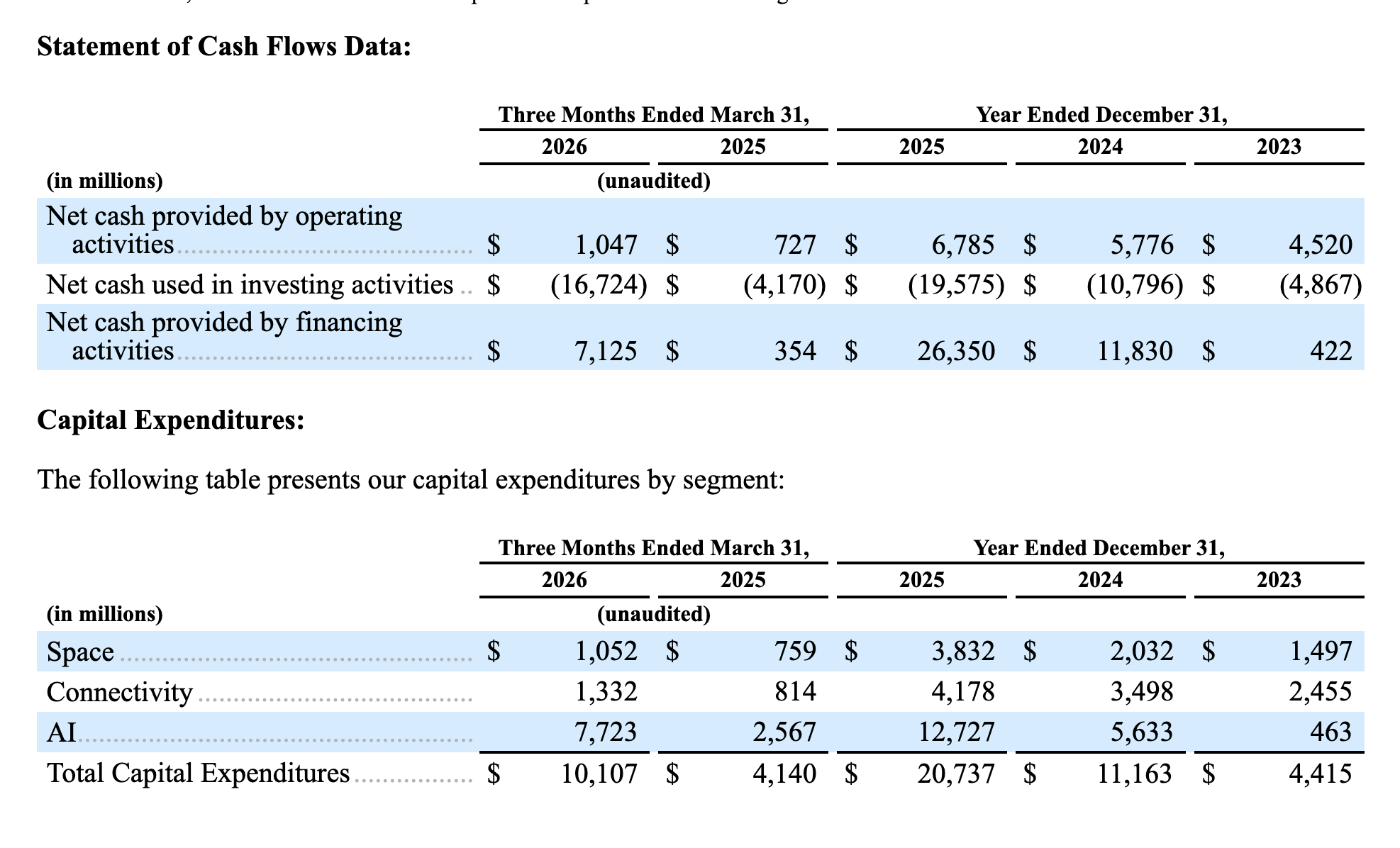

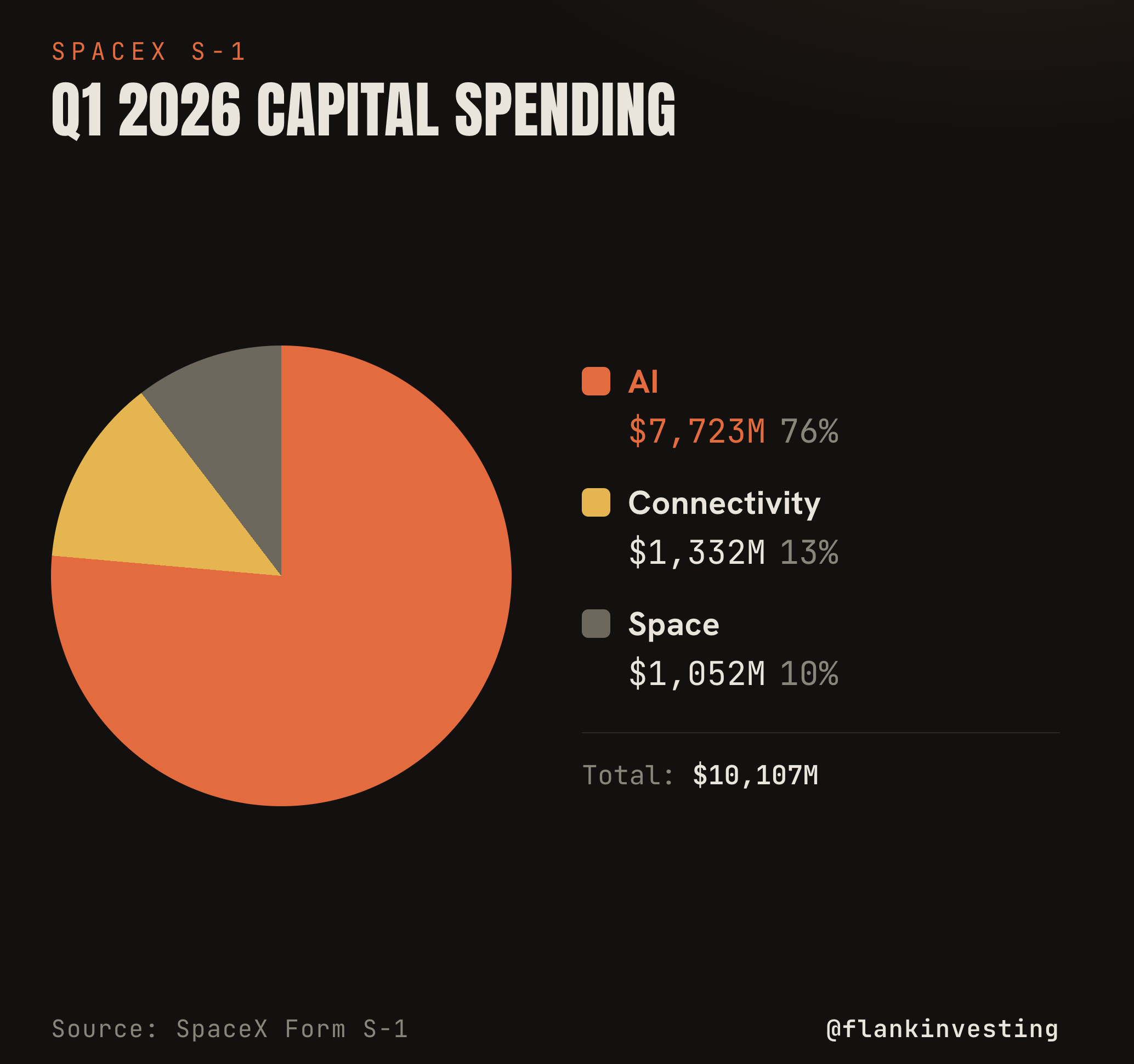

And a vast majority of the Capital expenditures (>70%) are from... AI

So it seems like Musk is trying to sell us an AI company with the SpaceX logo.

Oh but don't worry, there's always Adjusted EBITDA (*cough* bullshit earnings) to come and try to pull the wool over our eyes:

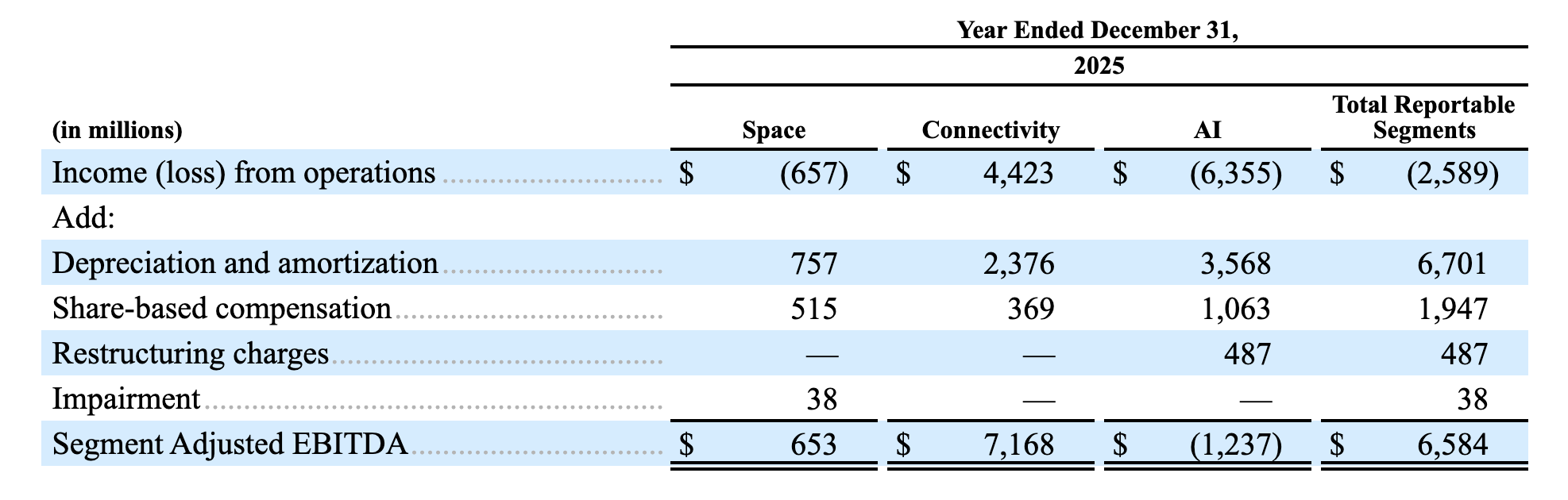

If you need more examples of the bullshit that Adjusted EBITDA gives, look no further than page 120 of the S-1:

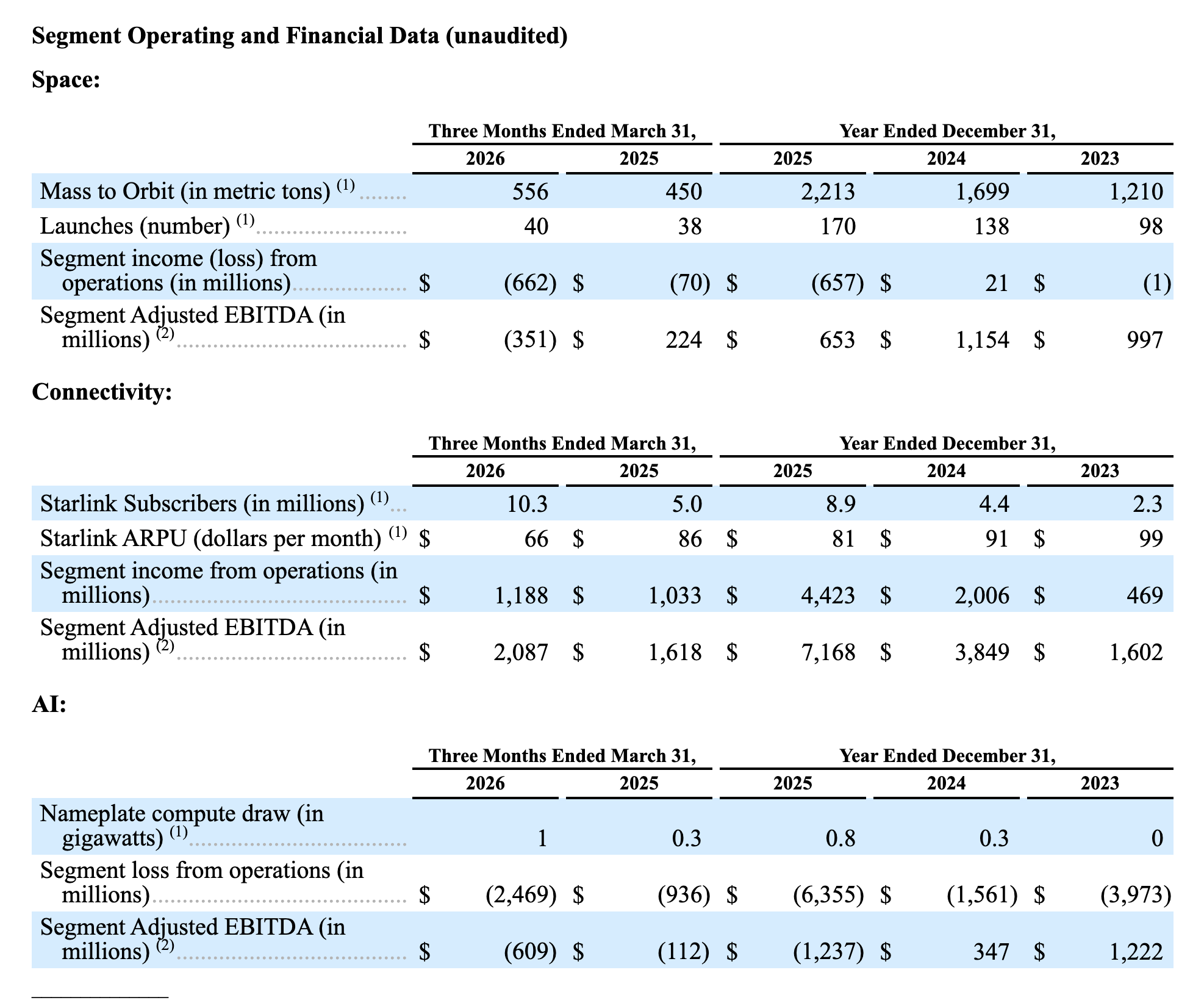

the space segment went from negative $657 million to $653 million in EBITA. Connectivity went from $4.4 billion in operating income to almost double it at $7 billion. AI went from negative $6 billion to only negative $1.2 billion

Wow! Amazing! groans

They Need Your Money

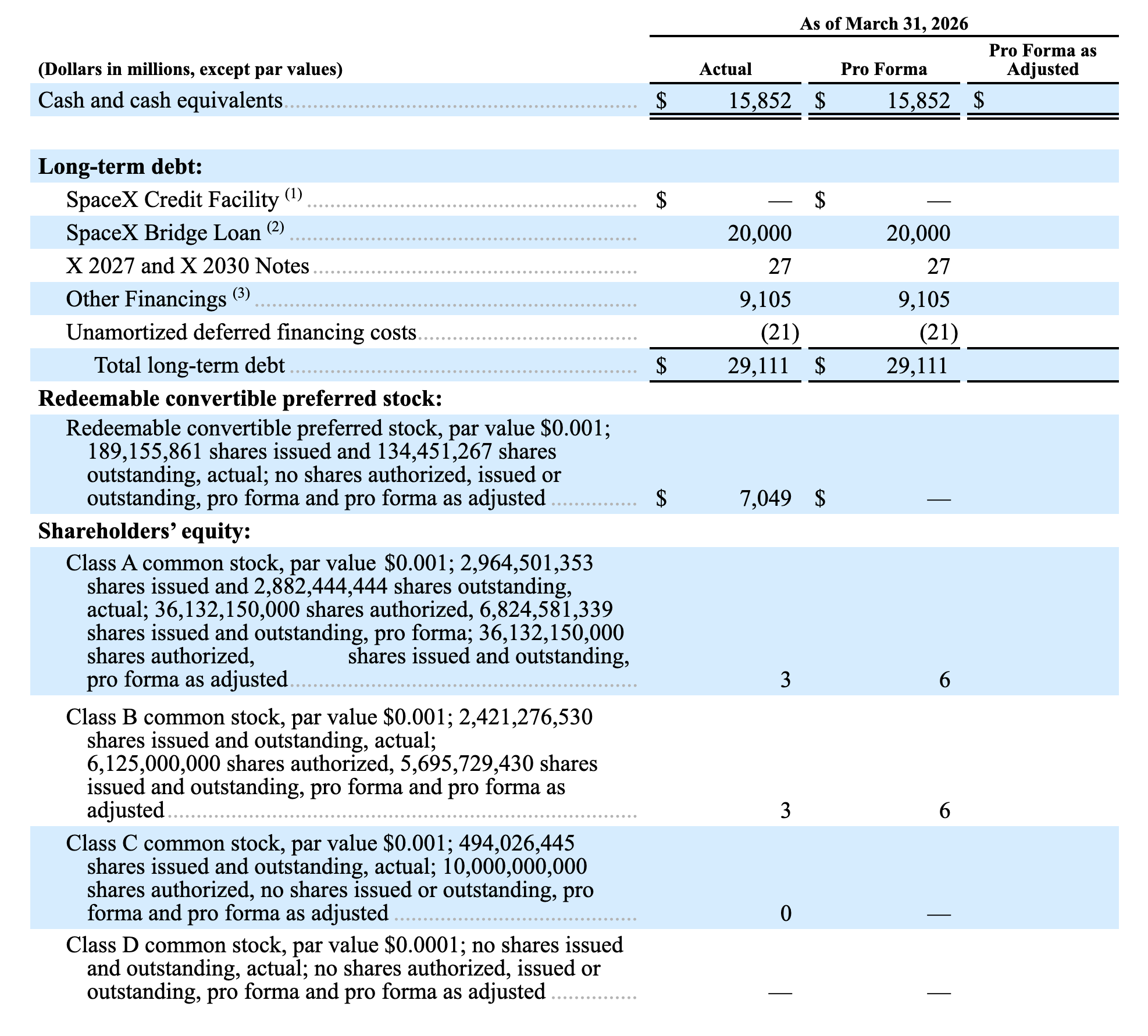

In the Capitalization section of the S-1, there's a $20 billion bridge loan sitting in the long-term debt stack, from Goldman, dated March 2, 2026, maturing September 2, 2027. A bridge loan is by definition temporary money you take out expecting to refinance it with something permanent, and the obvious "something permanent" is this IPO. The timing tells the story: the xAI merger closed February 2, 2026, and they drew the $20B bridge a month later.

So they borrowed twenty billion dollars to fund the AI pivot, and now they are bringing the company public with a roughly 16-month clock ticking on that loan. What's notable is that the stated use of proceeds never actually says "repay the bridge." It's all generic "expansion of our AI compute infrastructure" and "general corporate purposes."

But a $20B balloon coming due in 2027 does not just evaporate. Retail is, in effect, refinancing Goldman.

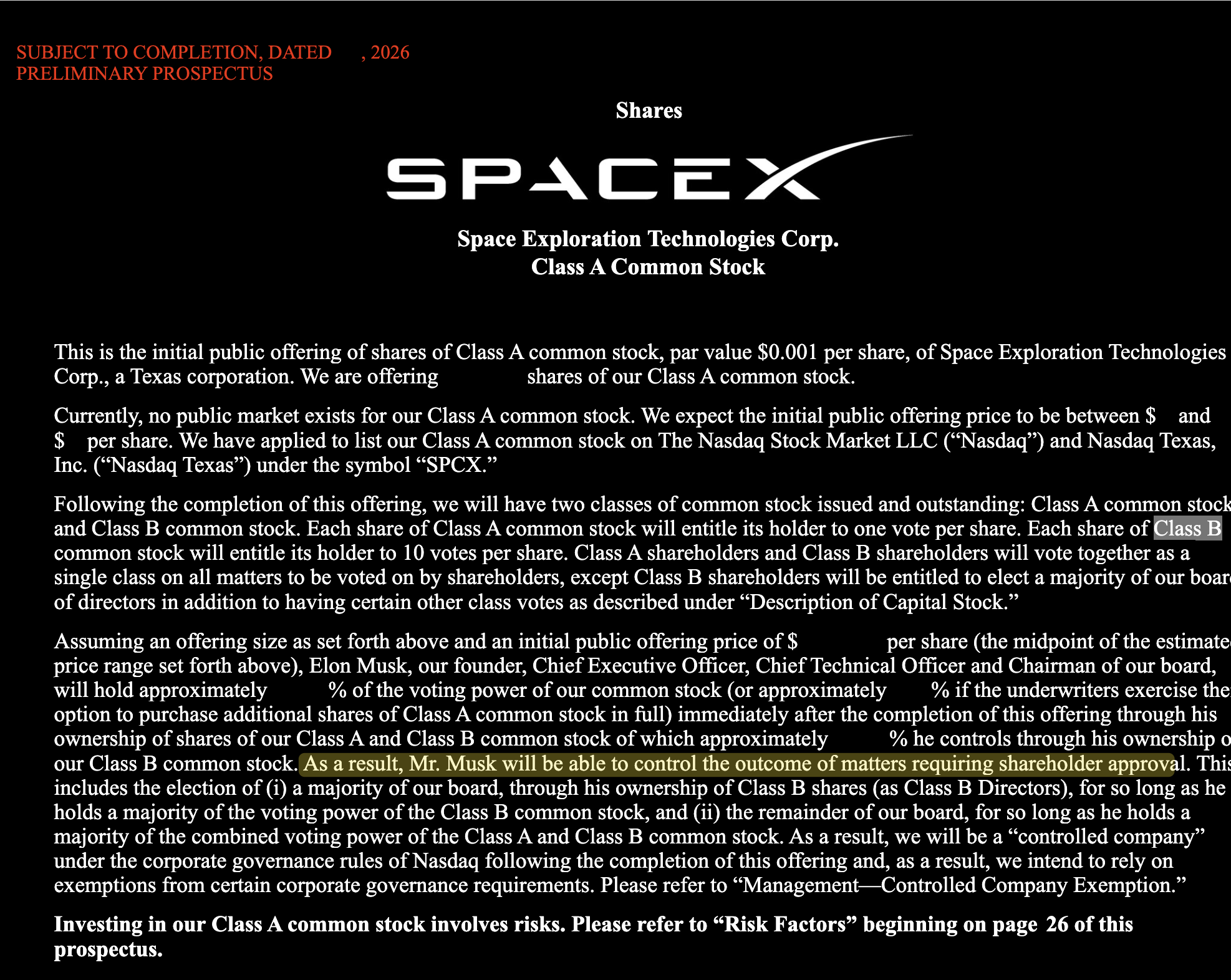

NO VOTE FOR YOU!

If you do decide to join the IPO, and Musk continues down his insane (alleged) drug fueled rampage and destroys the brand of SpaceX, don't worry... you'll never be able to vote him out!

The Class A stock you'd buy gets one vote per share; Musk's Class B gets ten. The Class B holders elect a majority of the board no matter what, the company lists as a "controlled company" so it opts out of the independent-board and independent-compensation-committee rules, and the bylaws force shareholder disputes into Texas Business Court and then mandatory arbitration, waive your right to a jury trial, and bar you from bringing claims as a class action.

Conclusion

This IPO is hot garbage, just as we expected.

I wouldn't touch this thing with a hundred-foot pole.

While I don't give stock advice, I will strongly recommend that you take a long walk on the beach or touch some grass before even thinking about participating in this IPO.

This seems like a desperate attempt to make a bridge loan so Musk can continue his AI fever dream that has not yet delivered real value and is vastly far behind other frontier models. Buyer beware.

Now, if it crashes, I could see this being a buy, but certainly not at the proposed $2 trillion valuation. Maybe like, idk, something more earnest like $100B... which would be a 95% crash. Here's to hoping.

Sentiment: Bearish